If you’re running a conveyancing practice in Australia, AML/CTF compliance isn’t optional, it’s a legal obligation that carries serious penalties when it’s not done properly. Having a solid conveyancing AML program checklist in place is the difference between a practice that’s audit-ready and one that’s scrambling to plug gaps when AUSTRAC comes knocking.

The challenge most practitioners face isn’t a lack of awareness, it’s knowing exactly what needs to be in the program, how to document it, and how to keep it current. Identity verification, risk assessments, ongoing monitoring, and record-keeping all need to work together as a cohesive compliance framework, not a collection of disconnected spreadsheets. That’s where tools like StackGo’s IdentityCheck come in, letting you run KYC verification directly from your existing software rather than juggling yet another platform.

This guide walks you through every component your AML program needs, step by step. You’ll get a practical, actionable checklist you can start implementing today, covering everything from your initial risk assessment through to staff training and reporting obligations. Whether you’re building a program from scratch or tightening up an existing one, this is your starting point.

What changes on 1 July 2026 for conveyancers

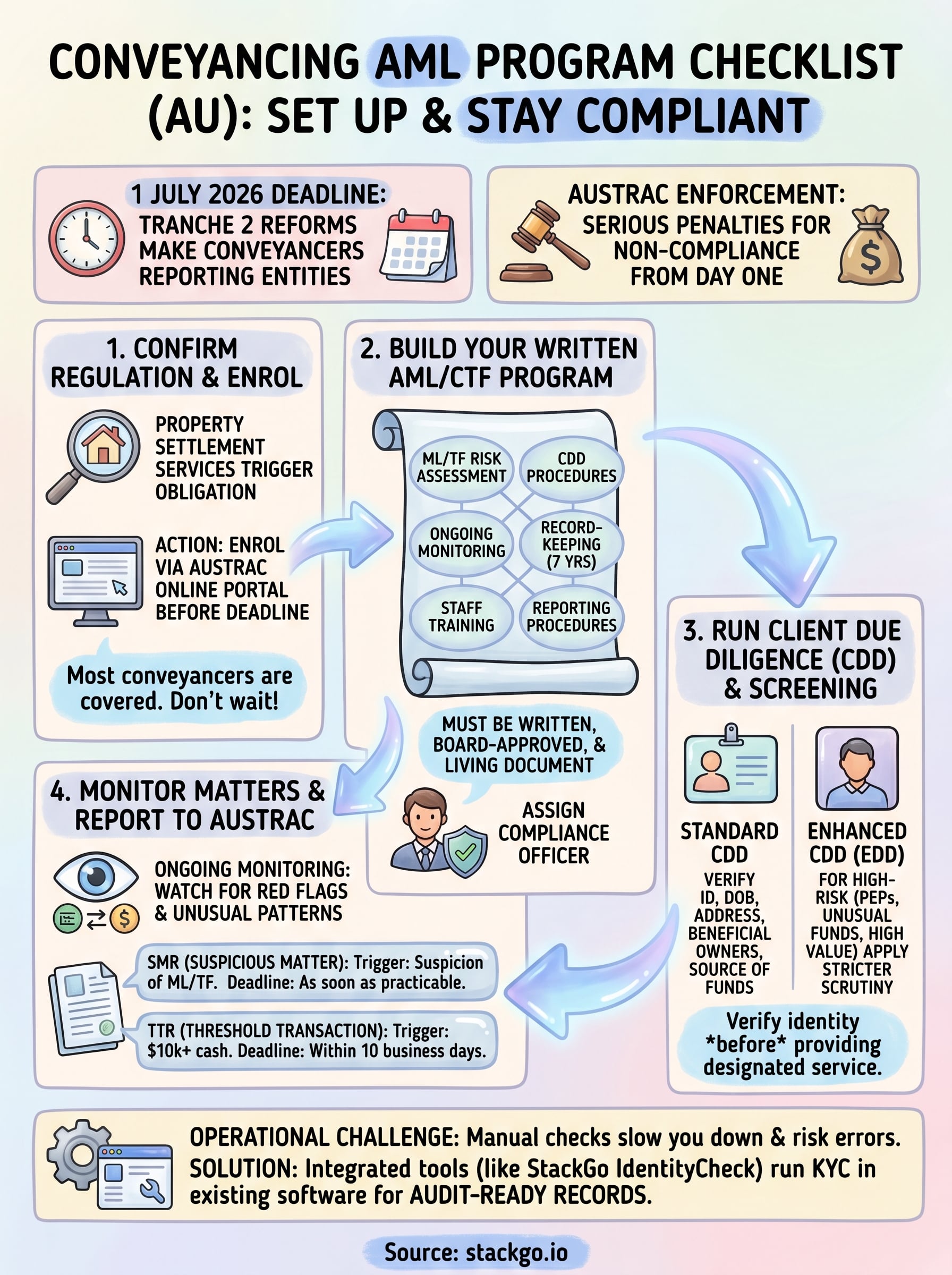

From 1 July 2026, conveyancers in Australia become reporting entities under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act). This is the result of the Tranche 2 reforms, which extend Australia’s AML/CTF regime to professional services that were previously outside its scope. If you provide conveyancing services, the date matters, and you need to act well before it arrives.

What the Tranche 2 reforms actually cover

The reforms bring designated non-financial businesses and professions (DNFBPs) into the regime for the first time. Conveyancers fall under this category because property transactions are a well-documented pathway for money laundering in Australia. AUSTRAC has identified real estate as a high-risk sector, with property regularly used to layer and integrate illicit funds through otherwise legitimate transactions.

AUSTRAC’s 2024 risk assessment identifies real estate as one of Australia’s highest-risk sectors for money laundering activity.

Your obligations under the new rules include enrolling with AUSTRAC, establishing a written AML/CTF program, conducting customer due diligence (CDD), reporting suspicious matters and threshold transactions, and keeping records for seven years. These are not optional extras you can phase in gradually, they are mandatory requirements from day one of the new regime.

What happens if you miss the deadline

Failing to comply by 1 July 2026 exposes your practice to significant civil and criminal penalties. AUSTRAC has enforcement powers that include infringement notices, enforceable undertakings, and court-ordered penalties running into the millions of dollars. Every conveyancing AML program checklist should treat the deadline as a hard cutoff, not a soft target, because AUSTRAC has a clear track record of pursuing non-compliant entities without hesitation.

Step 1. Confirm you are regulated and enrol

Before you build anything else on your conveyancing AML program checklist, confirm your practice falls within the regulated scope and then enrol with AUSTRAC. Most conveyancers providing property settlement services in Australia will be caught by the new rules, but it pays to verify this before proceeding.

What services trigger the obligation

Your practice becomes a reporting entity if you provide conveyancing services that involve transferring real property on behalf of a client. This includes residential and commercial settlements, preparation of transfer documents, and acting as a settlement agent. If you are unsure whether your specific services qualify, AUSTRAC’s published guidance is the definitive reference.

Once you provide a designated service, the obligation to enrol applies immediately, regardless of transaction volume or business size.

How to enrol with AUSTRAC

Enrolment happens through the AUSTRAC Online portal. You will need your ABN, business contact details, and a clear description of your designated services. Work through these steps before 1 July 2026:

- Log in to or create your AUSTRAC Online account

- Select "Enrol as a reporting entity"

- Confirm your designated service type as conveyancing

- Submit your enrolment and save the confirmation for your records

Step 2. Build your AML and CTF program

Your AML/CTF program is the central document that proves your practice takes compliance seriously. It must be written, formally approved by senior management, and updated regularly as your business and the regulatory environment evolve. Without a documented program in place by 1 July 2026, your practice is non-compliant from day one.

What your written program must include

Every conveyancing AML program checklist should confirm these six elements are documented:

- ML/TF risk assessment covering your clients, services, and delivery channels

- Customer due diligence (CDD) procedures for new and existing clients

- Ongoing monitoring processes to detect unusual transaction patterns

- Record-keeping policies that meet the seven-year retention requirement

- Staff training schedule with dated completion records

- Reporting procedures for suspicious matter reports (SMRs) and threshold transaction reports (TTRs)

AUSTRAC requires your program to be a living document, reviewed and updated regularly, not filed away after the initial sign-off.

Assign a compliance officer

Your program needs a named compliance officer responsible for day-to-day implementation and oversight. This person must understand your obligations under the AML/CTF Act and hold the authority to enforce procedures consistently across the whole practice.

Step 3. Run client due diligence and screening

Customer due diligence is one of the most operationally intensive parts of your conveyancing AML program checklist. Every time you onboard a new client, you need to verify their identity before providing a designated service, and the level of scrutiny depends on the risk profile of that client.

Standard CDD requirements

For most clients, standard CDD means collecting and verifying the full legal name, date of birth, and residential address. You must also identify the beneficial owners of any company or trust instructing you and document the source of funds where it is not immediately clear. Use this checklist for each new matter:

- Full legal name verified against a government-issued document

- Date of birth

- Residential address

- ABN or ACN for businesses

- Beneficial ownership confirmed for companies and trusts

- Source of funds documented

When to apply enhanced due diligence

Some clients carry a higher risk profile and require enhanced due diligence (EDD). Trigger EDD when your client is a politically exposed person (PEP), the transaction involves a high-value property, or the source of funds cannot be readily explained.

Failing to apply EDD to high-risk clients is one of the most common compliance gaps AUSTRAC identifies during reviews.

Step 4. Monitor matters and report to AUSTRAC

Your compliance obligations don’t end once you complete CDD at onboarding. Ongoing monitoring is a core requirement of your conveyancing AML program checklist, and it means actively reviewing client transactions and behaviour throughout the full life of each matter.

Ongoing transaction monitoring

You need to watch for transaction patterns that don’t match the client’s stated purpose or financial profile. Common red flags include last-minute changes to purchaser names, third-party fund contributions without clear explanation, and unusual urgency around settlement timelines. Document every concern in writing, even when you decide no further action is warranted.

A documented decision not to file a report is far safer than no record at all if AUSTRAC ever reviews your files.

Reporting to AUSTRAC

Two mandatory report types sit at the core of your obligations. Suspicious matter reports (SMRs) must be lodged with AUSTRAC as soon as practicable after you form a suspicion, and threshold transaction reports (TTRs) are required for any cash transaction of $10,000 or more. Use this quick reference for each matter:

| Report type | Trigger | Deadline |

|---|---|---|

| SMR | Suspicion of ML/TF activity | As soon as practicable |

| TTR | Cash transaction of $10,000+ | Within 10 business days |

Next steps for your practice

Working through this conveyancing AML program checklist gives you a clear picture of what your practice needs to have in place before 1 July 2026. The deadline is close, so the right move is to start with enrolment and your written AML/CTF program this week, then build your CDD and monitoring workflows around them in the weeks that follow. Waiting until June puts you under unnecessary pressure.

The operational side is where most practices run into friction. Manual identity checks across multiple platforms slow down onboarding, introduce errors, and make it harder to maintain audit-ready records. StackGo’s IdentityCheck runs KYC verification directly inside your existing software, so your team verifies clients without switching tabs or managing a separate compliance tool.

If you want to see how it fits your practice, explore IdentityCheck for AUSTRAC Tranche 2 compliance or create a free account and run a test check today.