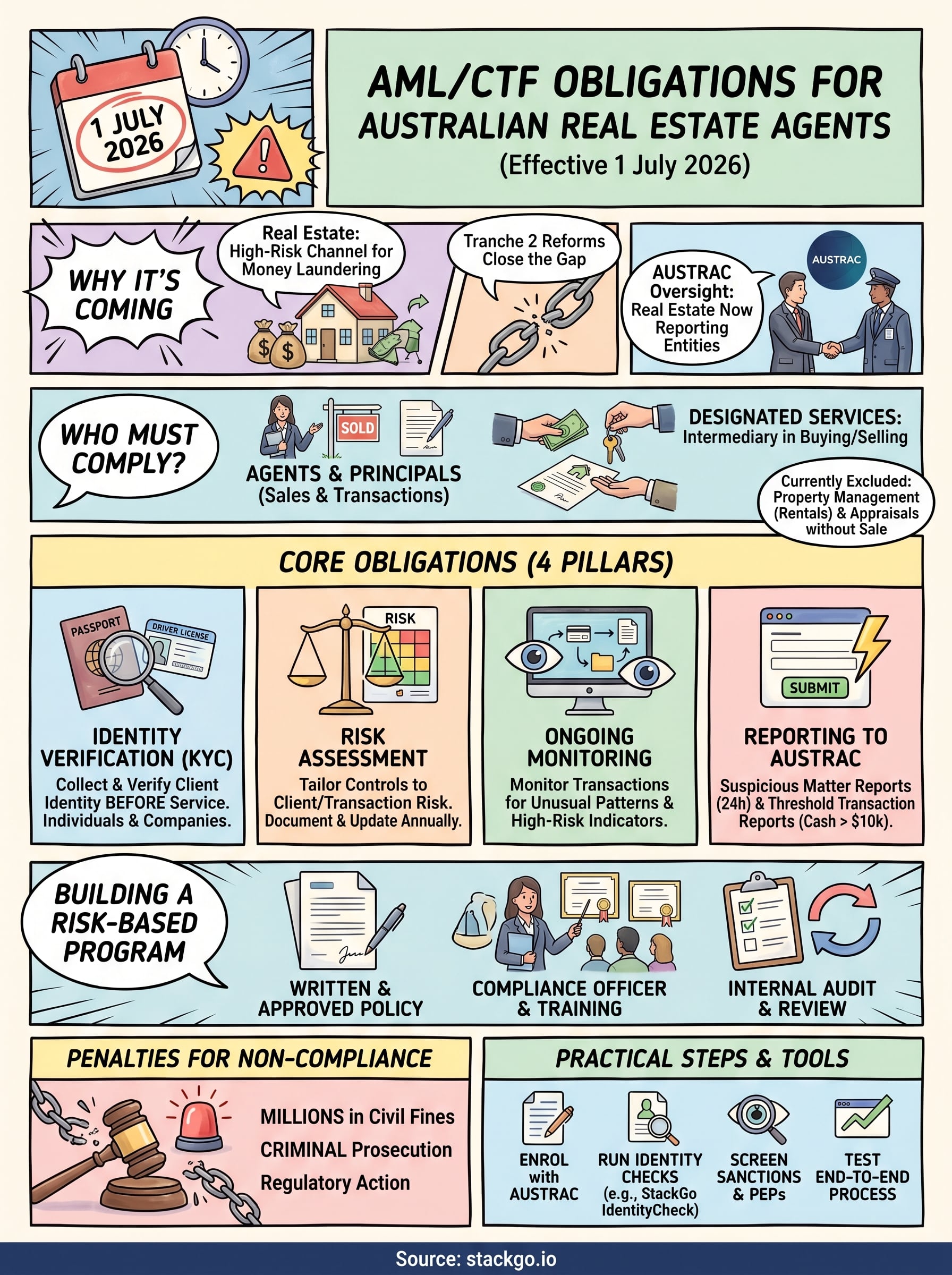

Australia’s Tranche 2 reforms bring AML/CTF obligations for real estate agents Australia-wide into effect from July 2026, and the deadline is now less than three months away. For the first time, real estate professionals will fall under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006, placing them alongside financial institutions and gambling operators as regulated reporting entities under AUSTRAC.

This isn’t a box-ticking exercise. Real estate has long been identified as a high-risk channel for money laundering in Australia, and the new regime requires agents to implement customer due diligence, ongoing transaction monitoring, and suspicious matter reporting as part of their day-to-day operations.

This article breaks down exactly what’s required: the specific obligations you’ll need to meet, the penalties for non-compliance, and the practical steps to build a compliant program before the deadline hits. We’ve also covered how tools like StackGo’s IdentityCheck can help you run KYC/AML identity verification directly from your existing CRM, so compliance fits into your current workflow rather than adding another disconnected system to manage. If you’re in real estate and haven’t started preparing, now is the time to act.

Why AML/CTF is coming to Australian real estate

Australia has known for years that its property market carries serious money laundering risk. The same features that make real estate attractive to legitimate investors – large transaction values, stable returns, and tangible assets – also make it attractive to people moving criminal proceeds through the economy.

The gap in Australia’s financial crime framework

The Financial Action Task Force (FATF) reviewed Australia’s AML/CTF regime and identified a critical weakness: professional service providers, including real estate agents, lawyers, and accountants, faced no obligation to report suspicious activity or verify client identities. Australia was one of the few developed nations with this gap still open. International partners, including the United States and the United Kingdom, had brought real estate professionals into their frameworks years earlier.

AUSTRAC has linked billions of dollars in Australian property transactions to suspected money laundering activity, making real estate one of the highest-risk sectors in the country.

Australian law enforcement has documented cases where high-value property purchases converted proceeds from drug trafficking, foreign bribery, and organised crime into seemingly legitimate wealth. Without mandatory checks, agents had no requirement to ask who their client was or where the funds originated.

What the Tranche 2 reforms change

The Tranche 2 amendments to the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 close that gap directly. They extend regulated reporting entity status to real estate professionals for the first time, placing the same customer due diligence requirements on agents that banks and financial institutions have carried for years.

For you, this shift is concrete. The AML/CTF obligations for real estate agents Australia-wide mean you now carry formal legal responsibilities to identify your clients, assess transaction risk, and report certain activity to AUSTRAC. These are not optional guidelines – they are statutory requirements with real financial and criminal penalties attached to non-compliance.

Who must comply and what counts as a designated service

Not every person involved in real estate falls under the new regime. The legislation targets specific roles and transaction types, so understanding exactly where you sit in that framework is the first step toward knowing what you need to do.

Real estate agents and agency principals

If you sell, purchase, or facilitate the transfer of real property on behalf of another person for payment, you are a reporting entity under the amended Act. This covers licensed agents and agency principals across residential, commercial, and rural property. Property managers who only handle rental arrangements are currently excluded, but any agent who also conducts sales falls within scope.

What qualifies as a designated service

The AML/CTF obligations for real estate agents Australia-wide apply when you provide a designated service, which the legislation defines as acting as an intermediary in the buying or selling of real property. This includes off-the-plan sales, auction transactions, and any arrangement where you receive or handle purchase funds on a client’s behalf.

If you are unsure whether a specific service you offer triggers designation, AUSTRAC’s published guidance is the authoritative reference point.

Leasing, property management, and appraisals without a sale component sit outside this definition for now, though AUSTRAC has indicated it will monitor how the regime operates before considering further extensions.

Key obligations and deadlines for 2026

The 1 July 2026 commencement date is fixed, and AUSTRAC expects reporting entities to be fully operational on day one. For real estate agents, compliance is not something you phase in gradually – you need a functioning program in place before that date, not after it.

The 1 July 2026 compliance deadline

From 1 July 2026, every designated service provider in real estate must be enrolled with AUSTRAC and operating under a compliant AML/CTF program. AUSTRAC has confirmed that enrolment itself is a separate requirement, and failing to enrol before you provide a designated service is a distinct breach from any program-related failures. Penalties for non-compliance include civil fines in the millions and, in serious cases, criminal prosecution.

Enrolment through AUSTRAC’s online portal is the first step – without it, you cannot legally provide a designated service under the new regime.

Your core statutory obligations

The AML/CTF obligations for real estate agents Australia-wide cover four main areas once the regime starts. You must identify and verify your clients before or during each transaction, assess the risk level of each customer relationship, monitor ongoing transactions for unusual patterns, and report suspicious matters to AUSTRAC promptly. Both the buyer’s agent and the seller’s agent carry these duties independently where each party receives a fee for facilitating the transaction. Failing to meet any one of these four obligations exposes your agency to regulatory action.

How to build a risk-based AML/CTF program

A risk-based program means you tailor your compliance controls to the actual risk level of each client and each transaction, rather than applying identical procedures across every deal. AUSTRAC requires your program to be written, approved by senior management, and actively maintained. It cannot sit as a static document you produce once and forget; your program must also include an internal audit function to confirm your controls are working in practice.

Document your risk assessment

Your first task is to produce a written risk assessment that maps the types of clients you work with, the transaction values you handle, and the geographic markets you operate in. Reviewing and updating this assessment at least annually keeps your program aligned with changes in your business and AUSTRAC’s guidance. Common high-risk indicators include:

- Foreign buyers or clients with offshore funds

- Transactions involving trusts, companies, or other complex ownership structures

- Cash-heavy deals or unusually fast settlement requests

A thorough risk assessment is the foundation that every other part of your compliance program depends on.

Assign roles and train your staff

Every agency principal must nominate a compliance officer to own the program and keep it current. That person carries responsibility for day-to-day oversight and signs off on any changes to your program documentation.

The AML/CTF obligations for real estate agents Australia-wide require that training records are documented and refreshed whenever your risk profile or the rules change. Staff who handle transactions without completing that training expose your agency to direct regulatory liability.

How to handle KYC, sanctions and AUSTRAC reporting

The AML/CTF obligations for real estate agents Australia-wide require you to take concrete steps at the transaction level, not just at the policy level. Knowing how to run identity checks, screen against sanctions lists, and lodge reports with AUSTRAC correctly is what separates a functioning program from one that looks good on paper but fails in practice.

Verifying client identity

You must collect and verify each client’s identity before you provide your designated service. For individuals, this means confirming their full name, date of birth, and residential address against a government-issued document such as a passport or driver’s licence. For companies, you need to verify the entity and identify its beneficial owners.

Verification must happen before settlement, not after – AUSTRAC treats post-transaction checks as a breach of your obligations.

Checking sanctions and PEPs

You must screen every client against Australia’s consolidated sanctions list and assess whether they qualify as a politically exposed person. The Australian Government publishes the consolidated list through the Department of Foreign Affairs and Trade, and you should check it at each new transaction, not just at onboarding. A match does not automatically block a deal, but it triggers enhanced due diligence.

Submitting reports to AUSTRAC

You must lodge a Suspicious Matter Report with AUSTRAC within 24 hours if you suspect a transaction relates to crime. Threshold transaction reports apply where you handle physical cash above AUD 10,000.

Final checks before you go live

With 1 July 2026 approaching fast, use the final weeks to confirm your program is ready to operate, not just ready to present. Check that you are enrolled with AUSTRAC, your written risk assessment is signed off by senior management, your compliance officer is nominated, and every staff member handling transactions has completed documented training. Run a test of your identity verification process end-to-end to confirm it produces a clear outcome before settlement, not after.

The full scope of AML/CTF obligations for real estate agents Australia-wide requires you to keep every element of your program current, so build a review cycle into your calendar now rather than scrambling when the rules shift.

The practical sticking point for most agencies is making KYC verification fast enough to fit inside a live transaction. StackGo’s IdentityCheck runs identity checks directly inside your existing CRM, so your team works in one place. See how IdentityCheck supports Tranche 2 compliance and test it against your current workflow before the deadline.