Australia’s financial services regulatory requirements exist to protect consumers, maintain market integrity, and ensure that firms operating in the sector meet strict compliance obligations. Whether you hold an Australian Financial Services Licence (AFSL), are applying for one, or simply need to understand how the rules affect your day-to-day operations, getting across this framework isn’t optional, it’s foundational to running a compliant business.

The regulatory structure covers a lot of ground: licensing, conduct obligations, anti-money laundering and counter-terrorism financing (AML/CTF), client verification (KYC), dispute resolution, and ongoing reporting. Multiple bodies oversee enforcement, with ASIC, APRA, and AUSTRAC each responsible for different pieces of the puzzle. For firms trying to keep up, the challenge isn’t just knowing the rules, it’s operationalising them without drowning in manual processes or disconnected software.

That operational challenge is exactly where tools like StackGo’s IdentityCheck become relevant. Compliance obligations such as KYC and AML/CTF verification need to happen reliably and repeatedly for every client you onboard. StackGo enables regulated businesses to run identity verification directly from their existing CRM, platforms like HubSpot or Salesforce, so compliance tasks slot into your current workflow rather than sitting in a separate system. With support for over 200 countries and 10,000 document types, it’s built for firms that need global coverage without the headache of managing yet another standalone tool.

This article breaks down the full scope of Australian financial services regulation: the key laws, the governing bodies, specific licensing and compliance obligations, and how the framework applies in practice. By the end, you’ll have a clear, working understanding of what’s required and where the major obligations sit, whether you’re new to the sector or tightening up an existing compliance programme.

Why financial services regulation matters in Australia

Australia’s financial services sector manages trillions of dollars across superannuation, lending, insurance, and investment products, making it one of the largest contributors to the national economy. That scale creates significant exposure: when things go wrong in financial services, they affect millions of ordinary Australians, not just a handful of sophisticated investors. Regulation exists because financial products are complex, often asymmetric in their risks, and typically purchased by consumers who don’t have the technical knowledge to assess what they’re actually buying. Meeting your financial services regulatory requirements isn’t a formality you tick off once; it’s the ongoing mechanism that keeps consumer trust, market stability, and your own operating licence intact.

The Royal Commission changed the enforcement landscape

The 2018-2019 Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry fundamentally shifted how regulators and businesses approach compliance in Australia. Commissioner Hayne’s findings exposed systemic misconduct across major institutions, including charging fees for no service, selling products that were clearly unsuitable, and consistently failing to act in clients’ best interests. The Commission wasn’t simply a reputational crisis for those firms; it directly triggered legislative reform and gave regulators expanded enforcement powers that remain in force today.

When regulation fails in financial services, the consequences aren’t limited to fines: they ripple out as widespread consumer harm, market instability, and lasting damage to the trust that the entire industry depends on.

Following the Commission, ASIC adopted a formal "why not litigate?" enforcement stance, replacing the previous preference for negotiated settlements and remediation plans. That shift means non-compliance now carries a real prospect of litigation rather than a quiet conversation. Firms that previously relied on goodwill with their regulator can no longer assume that approach will protect them.

What the stakes look like for individual firms

For your business, the practical consequences of non-compliance run across several dimensions. Civil penalties under the Corporations Act can reach millions of dollars per contravention. Beyond financial penalties, regulators can suspend or revoke your AFSL, ban individuals from operating in the sector, and require costly remediation programs that consume significant operational resources. Public enforcement action also carries reputational damage that affects client retention and new business development in ways that are difficult to reverse.

Smaller firms sometimes assume that enforcement action is reserved for large institutions. In practice, ASIC regularly takes action against smaller licensees and individual advisers, particularly where misconduct is clear and consumers have experienced direct harm.

Why compliance protects your business, not just your clients

Regulatory obligations are frequently framed in terms of consumer protection, but they serve a direct protective function for your firm as well. A business that runs documented, auditable compliance processes is substantially better positioned when a client dispute arises, when a regulator requests records, or when an internal review takes place.

Take client onboarding as a concrete example. If your KYC process is manual, inconsistent, or conducted outside your core systems, it creates gaps that are difficult to defend under scrutiny. A systematic, well-documented approach to verifying client identities, running AML checks, and recording outcomes gives you a defensible record that manual spreadsheets simply cannot replicate. Embedding compliance into your operational workflow, rather than treating it as a parallel administrative task, is the practical difference between managing regulatory risk and reacting to it. The firms that treat compliance as infrastructure are the ones that scale without compounding liability at every stage of growth.

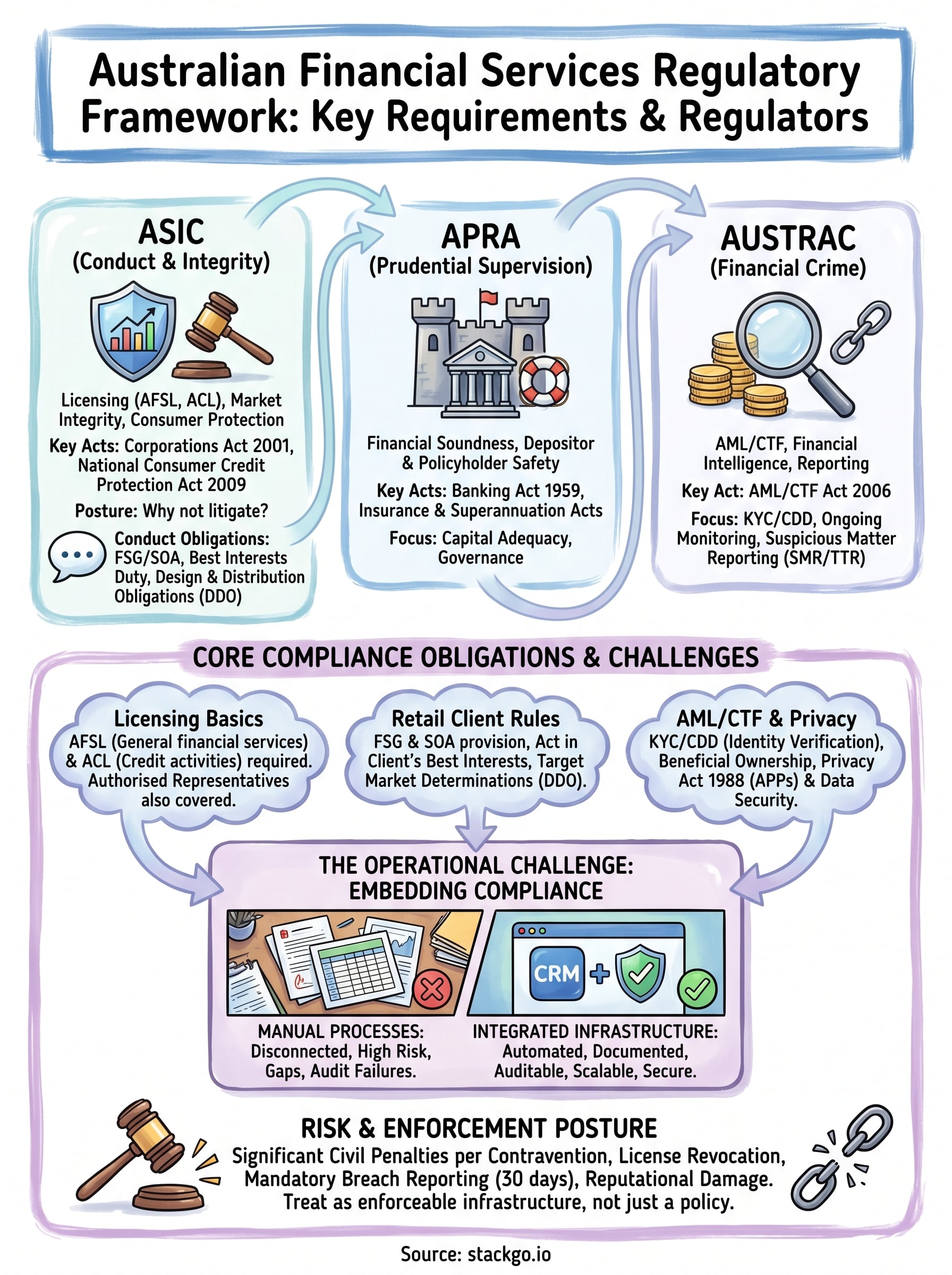

The regulators and how their roles differ

Australia’s financial services regulatory requirements are administered by three primary federal regulators, each with a distinct mandate. Understanding which regulator governs which part of your obligations is not just useful background knowledge; it directly affects how you structure your compliance programme and who you’ll be dealing with if something goes wrong.

ASIC: conduct and market integrity

The Australian Securities and Investments Commission (ASIC) is the conduct regulator for financial services and markets. ASIC administers the Corporations Act 2001, the National Consumer Credit Protection Act 2009, and a range of other legislation that governs how financial services businesses deal with their clients. If you hold an AFSL or a credit licence, ASIC is your primary licensing regulator. It also handles enforcement action for misconduct, including misleading advice, product suitability failures, and breaches of disclosure obligations.

ASIC’s current enforcement posture means that licence holders at every scale should treat regulatory obligations as legally enforceable requirements, not aspirational standards.

APRA: prudential supervision

The Australian Prudential Regulation Authority (APRA) focuses on the financial soundness of institutions rather than consumer conduct. Its mandate covers authorised deposit-taking institutions (ADIs) such as banks, credit unions, and building societies, as well as general and life insurers and superannuation funds. APRA sets and enforces capital adequacy standards, liquidity requirements, and governance frameworks designed to prevent institutional failure. If your business is an ADI or operates in the insurance or superannuation space, APRA’s prudential standards sit alongside ASIC’s conduct rules as a parallel compliance obligation.

AUSTRAC: financial crime and AML/CTF

The Australian Transaction Reports and Analysis Centre (AUSTRAC) administers the Anti-Money Laundering and Counter-Terrorism Financing Act 2006. Where ASIC focuses on conduct and APRA on institutional stability, AUSTRAC’s mandate is specifically about detecting and disrupting financial crime. Reporting entities, including a growing number of professional service firms under the incoming AML/CTF reforms, must maintain an AML/CTF programme, conduct customer due diligence, and submit suspicious matter and threshold transaction reports. AUSTRAC has demonstrated it will pursue significant civil penalty action against firms that fail to maintain adequate controls, with several landmark cases resulting in penalties running into the hundreds of millions of dollars.

The legal framework: key Acts and ASIC guidance

Australia’s financial services regulatory requirements sit across several pieces of legislation, each targeting a different part of the sector. Understanding which Acts apply to your business is the starting point for building a compliance programme that actually holds up under scrutiny, rather than one assembled from assumptions.

The Corporations Act 2001 and the ASIC Act

The Corporations Act 2001 is the primary statute governing financial services conduct in Australia. Part 7 of the Act sets out the licensing framework, the obligations that apply to AFSL holders and their authorised representatives, the rules around financial product disclosure, and the standards for providing financial product advice. If your firm provides financial services of any kind, Part 7 of the Corporations Act is the first document your compliance team needs to understand thoroughly.

The ASIC Act 2001 operates alongside the Corporations Act: it establishes ASIC’s powers and functions, and it contains its own consumer protection provisions that apply to financial services separate from the Australian Consumer Law.

Amendments introduced following the Royal Commission strengthened adviser registration requirements, introduced the Financial Adviser Standards and Ethics Authority (FASEA) framework for education and ethics obligations, and expanded ASIC’s civil penalty powers significantly. The penalty amounts for breaches of key provisions are not nominal, and they apply per contravention, which means a systemic failure across a client base can compound quickly.

ASIC regulatory guides and legislative instruments

ASIC supplements the legislation with a large body of regulatory guides, class orders, and legislative instruments that provide detailed guidance on how specific obligations apply in practice. These aren’t optional reading; in many cases they define the exact steps regulators and courts will use to assess whether your firm met its obligations. Regulatory Guide 175, for example, covers AFS licensing and the authorisation to provide financial services, including competency standards and responsible manager requirements.

Legislative instruments issued by ASIC can modify or extend obligations under the Corporations Act, sometimes with limited public notice. Your compliance team should maintain a regular review process that catches changes to instruments and updated regulatory guides before they affect your operations, rather than discovering a change after the fact. ASIC publishes updates on its website, and subscribing to those updates is a straightforward step that smaller firms often overlook.

Licensing basics: AFSL and who needs it

The Australian Financial Services Licence (AFSL) is the primary licence that authorises businesses to provide financial services in Australia. Administered by ASIC under the Corporations Act 2001, it functions as the legal gateway between your business and the clients you serve. Understanding the scope and requirements of the AFSL is one of the most practical steps you can take when mapping your firm’s financial services regulatory requirements.

What the AFSL covers

An AFSL does not grant blanket permission to provide any financial service; it specifies the particular services and products your firm is authorised to deal in. Your licence will list the financial products you can advise on or deal in, the types of clients you can serve (retail, wholesale, or both), and any conditions that apply to your operations. Common authorisations include financial product advice, dealing in securities, operating managed investment schemes, and providing traditional trustee company services.

If you operate outside the scope of your licence authorisations, even unintentionally, you are in breach of the Corporations Act and exposed to both civil and criminal penalties.

ASIC assesses applications against several criteria, including whether your responsible managers have adequate training, competency, and experience relevant to the services your firm intends to provide. You will also need to demonstrate that you have adequate resources, both financial and human, to operate a compliant business and meet your obligations to clients.

Who needs to apply

Any business that carries on a financial services business in Australia needs an AFSL unless a specific exemption applies. This includes businesses that provide financial product advice, issue or deal in financial products, make a market for financial products, or operate a registered managed investment scheme. The obligation applies to Australian businesses and foreign entities that provide services to Australian clients.

Some businesses do not need their own AFSL because they operate as authorised representatives of an existing licence holder. Under this arrangement, the licence holder takes on responsibility for the representative’s conduct, which is a significant compliance obligation that licence holders frequently underestimate. If you operate as an authorised representative, your obligations to clients remain substantively the same as those of a direct licence holder, even if the licensing responsibility sits with another entity.

Credit, banking and other licensing regimes

The AFSL is not the only licensing regime that applies to financial services businesses in Australia. Depending on what your firm does, you may need to comply with separate licensing frameworks that sit alongside or in addition to your AFSL obligations. Mapping these regimes to your actual business activities is a core part of understanding your financial services regulatory requirements in full.

The Australian Credit Licence

If your business engages in credit activities, you need an Australian Credit Licence (ACL) issued by ASIC under the National Consumer Credit Protection Act 2009. Credit activities include providing credit, arranging credit, and providing credit assistance to consumers. This covers mortgage brokers, personal lenders, car finance providers, and any business that assists consumers to apply for credit products.

Holding an AFSL does not authorise you to engage in credit activities. The two licences are separate, and operating credit activities without an ACL is a breach of the National Consumer Credit Protection Act.

Like the AFSL, the ACL requires you to demonstrate that your responsible managers hold the relevant qualifications and experience, that your business has adequate resources to comply with its obligations, and that you maintain membership of an approved external dispute resolution scheme. ASIC assesses ACL applications against these criteria, and the standards are comparable in rigour to the AFSL process.

Banking authorisation and the ADI framework

Businesses that want to accept deposits from the public must be authorised as a deposit-taking institution under the Banking Act 1959. APRA grants this authorisation and classifies ADIs into categories including full banks, mutual banks, credit unions, and building societies. The authorisation process is demanding: APRA applies detailed prudential standards covering capital adequacy, liquidity management, and governance before granting an ADI licence.

For most financial services firms, full ADI authorisation is not relevant to day-to-day operations. However, if your business partners with, distributes products for, or acts as an agent of an ADI, you need to understand the obligations that flow downstream. APRA’s prudential standards affect the products your ADI partner can offer and the operational requirements they must impose on their distribution arrangements, which in turn affect your compliance obligations at the point of client interaction.

Retail client rules: disclosure, advice and DDO

When your firm serves retail clients, a specific and detailed layer of obligations applies on top of your general AFSL duties. Retail clients receive stronger protections than wholesale clients because they are presumed to have less financial expertise and fewer resources to absorb losses from unsuitable advice or inadequate disclosure. These retail client rules form one of the most operationally demanding parts of Australia’s financial services regulatory requirements, and getting them wrong is the area where most conduct enforcement action originates.

Financial Services Guides and Statements of Advice

You must provide retail clients with a Financial Services Guide (FSG) before or at the time you provide them with a financial service. The FSG sets out who you are, what services you provide, how you are remunerated, and how clients can lodge complaints. It is not optional, and providing it after the fact does not satisfy the obligation.

Where you provide personal financial product advice to a retail client, you must follow up with a Statement of Advice (SOA). The SOA documents the advice, the basis on which it was given, and any conflicts of interest that might affect the recommendation. ASIC requires that the SOA be written in plain language so that the client can actually understand what they are being advised to do and why.

The best interests duty

The Corporations Act 2001 requires that when you provide personal advice to retail clients, you must act in the best interests of the client and prioritise their interests over your own where a conflict exists. This obligation, introduced through the Future of Financial Advice (FOFA) reforms and strengthened following the Royal Commission, is not satisfied by simply recommending a product that falls within a technically acceptable range.

Meeting the best interests duty requires documented reasoning, not just a compliant outcome. Regulators assess the process, not only the recommendation.

Design and Distribution Obligations

The Design and Distribution Obligations (DDO) framework, which came into effect in October 2021, requires product issuers to design financial products with a specific target market in mind and to document this in a Target Market Determination (TMD). Distributors, including your firm if you sell or recommend products issued by others, must take reasonable steps to ensure products reach consumers within the intended target market. If your distribution activity takes a product outside its TMD, you must report this to the issuer and review your distribution approach.

AML/CTF: KYC, reporting and ongoing monitoring

Australia’s Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act) imposes specific obligations on reporting entities, which include banks, financial services businesses, and a growing range of professional service providers under the recently reformed framework. If your firm is a reporting entity, AUSTRAC is your regulator, and non-compliance carries some of the heaviest civil penalties in the Australian regulatory landscape. These AML/CTF obligations sit firmly within the broader scope of financial services regulatory requirements and demand a structured, documented approach rather than ad hoc checks.

Customer due diligence and KYC

Customer due diligence (CDD) requires you to identify and verify the identity of your clients before you provide a designated service. For individual clients, this means collecting and verifying name, date of birth, and residential address against reliable and independent sources. For corporate clients, you need to identify the entity itself and verify the identity of its beneficial owners, which is the layer of due diligence that firms most commonly handle poorly.

Incomplete beneficial ownership identification is one of the most common deficiencies AUSTRAC identifies during compliance assessments, and it is also one of the most straightforward to fix with a consistent verification process in place.

Where your initial assessment identifies higher risk, you are required to apply enhanced customer due diligence (ECDD), which goes further into the source of funds, the nature of the business relationship, and expected transaction activity. Politically exposed persons (PEPs) and clients from high-risk jurisdictions automatically trigger ECDD obligations under most compliance frameworks.

Ongoing monitoring and reporting

Verifying a client once at onboarding is not sufficient to meet your obligations. You must monitor the ongoing relationship to ensure that transactions remain consistent with what you know about the client and to detect activity that might indicate money laundering or terrorism financing. When you identify suspicious activity, you must lodge a Suspicious Matter Report (SMR) with AUSTRAC, regardless of whether the transaction has been completed. Cash transactions of $10,000 or more also require a Threshold Transaction Report (TTR).

Your AML/CTF programme must document how you will meet each of these obligations, and AUSTRAC expects documented evidence of staff training, escalation procedures, and control testing. Treat the programme as a living document that you update as your business, client base, and regulatory obligations change.

Privacy and security requirements for customer data

The Privacy Act 1988 and its thirteen Australian Privacy Principles (APPs) sit alongside your broader financial services regulatory requirements as a core set of obligations that apply whenever you collect, use, or disclose personal information about clients. For financial services firms, almost every client interaction involves personal information, which means the APPs are relevant to your onboarding process, your advice records, your marketing activities, and your data storage practices simultaneously.

The Privacy Act and the Australian Privacy Principles

The APPs establish binding standards for how your business handles personal information at every stage of its lifecycle, from the point of collection through to disposal. APP 3 limits what personal information you can collect to what is reasonably necessary for your functions. APP 6 restricts how you can use or disclose that information beyond the original purpose for which it was collected. APP 11 requires you to take active steps to protect personal information from misuse, interference, loss, and unauthorised access.

If your client data is stored in a CRM or third-party system, you remain responsible for ensuring that system meets your APP 11 obligations, regardless of whether the security failure originates with your vendor.

Firms that handle personal information for more than 250 individuals, or that turn over more than $3 million annually, are generally covered by the Privacy Act. Most regulated financial services businesses meet these thresholds without difficulty. The Office of the Australian Information Commissioner (OAIC) enforces the Act and has authority to investigate complaints, conduct audits, and impose civil penalty orders for serious or repeated breaches.

Handling and securing customer data in practice

Your practical obligation is to understand where client data lives across your systems and what controls you have in place at each point. Data minimisation matters here: collecting only what you need and retaining it only for as long as you have a lawful purpose reduces your exposure if a breach occurs. A documented data retention and destruction policy gives you a defensible position and reduces the volume of sensitive information you hold at any given time.

Protecting personally identifiable information in your CRM is particularly relevant for firms running KYC and AML checks. StackGo’s IdentityCheck includes a privacy layer that keeps PII out of the CRM itself, making it accessible only to MFA-authenticated administrators. That architecture directly supports your APP 11 obligations without requiring you to build custom controls on top of your existing software.

Audits, breach reporting and enforcement risk

Staying on top of your financial services regulatory requirements means treating compliance as something you test regularly, not something you document once and assume is working. Regulators expect that your internal controls are actively monitored, that breaches are identified promptly, and that your firm knows exactly what reporting obligations apply when something goes wrong.

Internal audits and compliance testing

Your AML/CTF programme, your AFSL obligations, and your privacy controls all require periodic internal review to confirm that policies are being followed in practice and not just on paper. An internal audit process does not need to be elaborate, but it does need to produce documented evidence of what was tested, what was found, and what remediation steps were taken. ASIC expects that AFSL holders can demonstrate their compliance framework is operating effectively if asked, and a record of past reviews is the most straightforward way to support that position.

Regulators assess whether your controls are genuinely operational, not simply whether a compliance policy exists in a shared drive.

Breach reporting obligations

Under the Corporations Act 2001, AFSL holders have an obligation to report significant breaches to ASIC within 30 days of becoming aware of them. A significant breach includes any conduct that results in financial loss to a client, constitutes serious misconduct, or would reasonably be regarded as relevant to ASIC’s decision to grant or maintain your licence. The definition is broad enough that under-reporting carries real risk: if ASIC later identifies a breach you did not report, the failure to report itself becomes an additional contravention.

Your internal process needs a clear escalation pathway so that staff who identify potential breaches can raise them quickly, and the assessment of whether reporting is required happens without unnecessary delay.

Enforcement risk and what it means for your firm

ASIC’s current enforcement posture means that civil penalty action is a realistic outcome for firms that accumulate compliance failures, even where individual breaches may appear minor in isolation. Penalties under the Corporations Act apply per contravention, so a systemic failure affecting multiple clients simultaneously can escalate to a figure that threatens the viability of a smaller firm. Beyond financial penalties, ASIC can impose licence conditions, suspend or revoke your AFSL, and ban individuals from the industry.

Treating enforcement risk as a planning input, rather than a worst-case scenario, is what separates firms that absorb regulatory change well from those that get caught unprepared.

Key takeaways and next steps

Australia’s financial services regulatory requirements cover licensing, conduct, AML/CTF, privacy, and breach reporting. Each layer demands active, documented compliance rather than a one-time setup. ASIC, APRA, and AUSTRAC each govern distinct parts of the framework, and your obligations depend directly on what services you provide and which clients you serve.

The firms that manage this well treat compliance as operational infrastructure, not a separate administrative burden. Building verification, monitoring, and record-keeping into your existing workflows removes the gaps that regulators look for when assessing whether your controls were genuinely operational. Embedding those processes into tools your team already uses is the most reliable way to maintain consistent, auditable evidence of compliance across every client interaction.

If you need to run AML/CTF identity verification inside your current CRM without adding standalone software, see how IdentityCheck supports AUSTRAC Tranche 2 compliance and test whether it fits your business.