Australian businesses operating under AML/CTF regulations face a fundamental question: when is standard verification enough, and when do you need to dig deeper? Understanding enhanced due diligence vs customer due diligence is essential for staying compliant without over-engineering every client interaction.

Customer due diligence (CDD) forms the baseline, the standard identity checks you run on most clients. Enhanced due diligence (EDD) kicks in when risk factors demand closer scrutiny: politically exposed persons, high-risk jurisdictions, or unusual transaction patterns. Getting this distinction wrong means either wasting resources on unnecessary checks or, worse, failing to meet your regulatory obligations.

For accountants preparing for AUSTRAC’s expanded AML/CTF requirements, and professionals across financial services, legal, and real estate, this isn’t theoretical. These are the decisions you’ll make daily. At StackGo, we build identity verification tools like IdentityCheck that integrate directly into your existing CRM, so you can apply the right level of due diligence without switching between systems or drowning in manual processes.

This article breaks down when CDD applies, what triggers EDD, and how to structure your verification processes to meet Australian compliance standards efficiently.

Why the difference between CDD and EDD matters

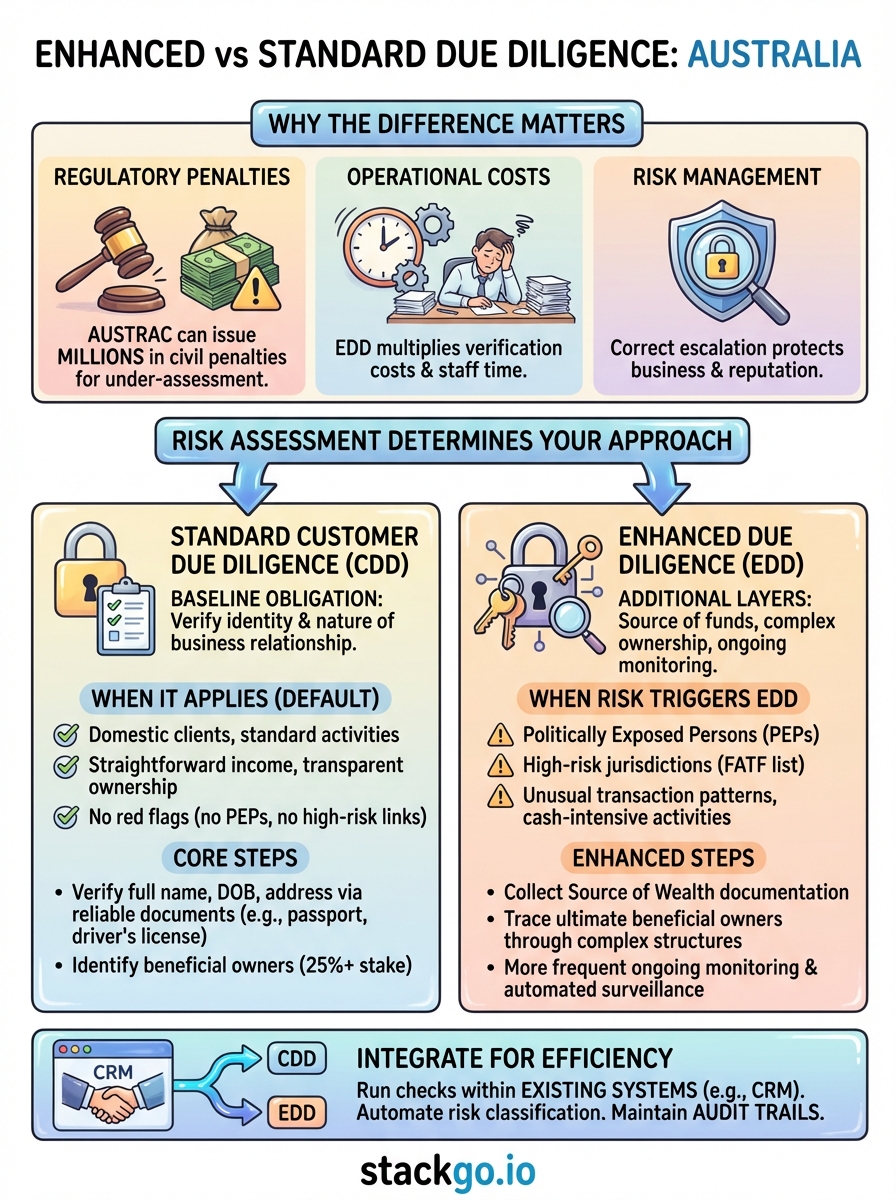

The distinction between enhanced due diligence vs customer due diligence directly impacts your compliance obligations, operational costs, and legal exposure. AUSTRAC doesn’t give you flexibility on when to apply each level. Your risk assessment determines the requirement, and applying the wrong level creates two equally problematic outcomes: regulatory breaches that invite enforcement action, or unnecessary friction that drives clients away.

Regulatory consequences you can’t ignore

When you apply only CDD to a high-risk client, you’ve failed to meet your AML/CTF obligations under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006. AUSTRAC can issue civil penalties reaching millions of dollars for reporting entities that systematically under-assess risk. For accountants preparing for expanded AML/CTF coverage, this means every client relationship needs proper classification from day one.

Conversely, treating every client as high-risk wastes resources and creates unnecessary delays in onboarding. Your low-risk clients don’t need source of wealth documentation or ongoing monitoring at EDD levels. The compliance framework expects you to calibrate your response to actual risk indicators.

The risk-based approach means you allocate verification resources where they genuinely protect against money laundering and terrorism financing threats, not uniformly across your entire client base.

Cost and efficiency implications

Running EDD on every client multiplies your verification costs. Each enhanced check requires additional documentation, deeper source of funds analysis, and ongoing monitoring that standard CDD doesn’t demand. For a practice with hundreds of clients, this difference translates to substantial operational expenses and staff time.

Your team spends more hours collecting documents, verifying information across multiple sources, and maintaining enhanced monitoring systems. This matters particularly for accountants and financial advisors who compete on service delivery speed. Getting clients through verification quickly, while meeting compliance standards, affects your competitive position.

Risk management you control

The difference between CDD and EDD determines how effectively you identify suspicious activity before it becomes your liability. Standard CDD catches basic identity fraud and ensures you know who you’re dealing with. Enhanced procedures dig into beneficial ownership structures, source of wealth, and transaction patterns that reveal money laundering or terrorism financing risks.

When you correctly escalate to EDD based on risk triggers, you protect your business from being used as a conduit for illicit funds. This isn’t just about avoiding penalties. It’s about maintaining the integrity of your client relationships and preserving your reputation in the market. Proper application means you can demonstrate to regulators that you understand your obligations and implement them appropriately.

What customer due diligence means in Australia

Customer due diligence represents your baseline obligation under AUSTRAC’s AML/CTF framework. You verify who your clients are, confirm their identity through reliable documentation, and understand the nature of their business relationship with your firm. This forms the foundation of your compliance program before you consider whether enhanced due diligence vs customer due diligence applies in specific cases.

The core verification steps

CDD requires you to collect and verify specific identity information for every client. You need their full name, date of birth, and residential address verified through documents like passports, driver’s licenses, or government-issued identification. For companies, you verify registration details through ASIC records and identify beneficial owners who control 25% or more of the entity.

Your verification process must use reliable and independent sources. This means checking documents against issuing authorities where possible, or using third-party verification services that meet AUSTRAC standards. You also need to understand the purpose and intended nature of the business relationship, which helps you establish a baseline for detecting unusual activity later.

Standard CDD applies to the majority of your client relationships, providing adequate protection for routine business activities without the additional scrutiny that high-risk situations demand.

When CDD applies by default

You apply CDD when onboarding clients who present no elevated risk factors. This includes domestic clients operating in standard business activities, individuals with straightforward income sources, and entities with transparent ownership structures. Australian residents conducting routine transactions within your normal service offering fall into this category.

CDD remains appropriate when you see no red flags during initial assessment: no links to high-risk jurisdictions, no unusual transaction patterns relative to the client’s stated business purpose, and no connections to politically exposed persons. Standard verification gives you sufficient information to meet your regulatory obligations while maintaining efficient onboarding processes.

What enhanced due diligence adds

Enhanced due diligence requires you to look beyond basic identity verification and examine the source of funds, beneficial ownership structures, and ongoing transaction patterns that standard CDD doesn’t demand. When comparing enhanced due diligence vs customer due diligence, the critical difference lies in the depth and frequency of scrutiny you apply to client relationships that present elevated money laundering or terrorism financing risks.

The additional verification layers

EDD mandates source of wealth documentation that traces where your client’s assets originated. You verify employment history, business revenue sources, inheritance documentation, or investment returns that explain their financial position. Standard CDD doesn’t require this level of financial background investigation.

You also examine beneficial ownership chains more thoroughly, particularly for complex corporate structures. While CDD identifies owners with 25% stakes, EDD requires you to trace control through multiple layers, identify ultimate beneficial owners regardless of direct shareholding, and verify the business purpose behind layered structures. This deeper investigation reveals whether legitimate commercial reasons exist for complex arrangements.

Enhanced procedures include ongoing monitoring at higher frequencies, with automated transaction surveillance that flags unusual patterns relative to the client’s established profile and risk classification.

When risk indicators trigger EDD

Politically exposed persons automatically require enhanced scrutiny under AUSTRAC requirements. You apply EDD when clients hold prominent public positions, have close associates in government roles, or maintain family connections to political figures. This extends to foreign PEPs operating in Australia.

Clients from high-risk jurisdictions identified by FATF trigger EDD obligations. Your verification intensifies when dealing with countries that have strategic AML/CTF deficiencies or face sanctions. Unusual transaction patterns relative to stated business purpose, such as cash-intensive activities inconsistent with industry norms, also escalate your due diligence requirements beyond standard CDD protocols.

How to choose between CDD and EDD in Australia

Your decision between enhanced due diligence vs customer due diligence starts with a systematic risk assessment of each client relationship. AUSTRAC requires you to classify clients based on objective risk indicators, not subjective feelings or business convenience. This assessment happens at onboarding and whenever circumstances change materially during the relationship.

Risk assessment determines your approach

You evaluate specific risk factors that AUSTRAC identifies in its guidance. Start by checking whether your client is a politically exposed person or holds family connections to PEPs. Review their geographic connections to high-risk jurisdictions on FATF’s list. Examine their business model for cash-intensive operations or complex ownership structures that obscure beneficial owners.

Client behaviour during onboarding provides additional signals. Reluctance to provide standard documentation, vague explanations about business purpose, or transactions that don’t match stated activities all indicate elevated risk requiring EDD. You document each assessment decision with clear reasoning that demonstrates your compliance approach to AUSTRAC auditors.

Your risk classification isn’t permanent, so you reassess whenever clients change business activities, enter new jurisdictions, or demonstrate transaction patterns inconsistent with their original profile.

Common risk triggers you’ll encounter

Accountants preparing for expanded AML/CTF obligations will frequently see these escalation triggers:

- Clients operating in high-risk sectors like money services, precious metals dealing, or gambling

- Trusts and companies with nominee directors or shareholders in tax haven jurisdictions

- New clients requesting services outside your normal business scope

- Transactions involving large cash components relative to industry standards

- Beneficial owners who cannot be verified through standard documentation

You apply EDD immediately when any combination of these factors appears. Standard CDD remains appropriate only when none of these indicators exist and the client presents transparent, verifiable business operations within Australia.

How to run CDD and EDD in your existing systems

Running both verification levels without disrupting your current operations requires integration into the systems you already use. You don’t need new software for identity checks if your verification tools operate directly within your CRM or practice management platform. This eliminates tab switching, duplicate data entry, and the manual errors that come from moving client information between disconnected systems.

Integration into your CRM workflow

Your verification process should read client details from your existing contact records, run the appropriate checks based on risk classification, and write results back automatically. When you onboard a new client in HubSpot, Salesforce, or similar platforms, your verification tool triggers standard CDD by default for low-risk profiles.

You configure your system to escalate automatically when risk triggers appear during initial assessment. Politically exposed person flags, high-risk jurisdiction connections, or unusual business structures automatically route to EDD workflows without manual intervention. This means your team sees clear next steps within the same interface they use for client management, not in a separate verification portal.

Integrated verification eliminates the need to export data, log into standalone compliance platforms, or manually transcribe verification outcomes back into your client records.

Automating risk classification decisions

You set up rule-based triggers that determine when enhanced due diligence vs customer due diligence applies. Your system checks client data against PEP databases, jurisdiction risk lists, and industry classification codes to assign risk levels automatically. Complex cases that require manual assessment get flagged for review rather than blocking the entire workflow.

At StackGo, we built IdentityCheck to handle this classification within your CRM, running global verification checks across 200+ countries without storing PII in your primary systems. Your team maintains complete audit trails of every verification decision, accessible when AUSTRAC requests compliance documentation.

Final checks

Getting enhanced due diligence vs customer due diligence right protects your business from regulatory penalties while keeping your onboarding process efficient. You apply standard CDD to your low-risk clients, escalate to EDD when specific risk indicators appear, and document every classification decision for AUSTRAC audits. This risk-based approach means you allocate verification resources where they actually protect against money laundering threats.

Your verification tools should work within your existing systems, not force you to adopt new software that sits outside your normal workflow. Integration eliminates manual errors, reduces onboarding time, and maintains complete audit trails accessible when regulators request compliance documentation.

For Australian accountants preparing for expanded AML/CTF obligations, IdentityCheck handles both verification levels directly inside your CRM, automatically classifying risk and running the appropriate checks without storing PII in your primary systems. You maintain compliance while your team focuses on client service, not compliance administration.