When onboarding clients, knowing the difference between customer due diligence vs enhanced due diligence determines whether you meet your compliance obligations or face regulatory action. Both processes sit at the core of AML/KYC frameworks, yet they apply to different risk levels and require different verification depths.

For accounting firms and regulated businesses in Australia, this distinction carries real weight. With TPB requirements already in place and AUSTRAC’s AML/CTF regulations expanding, understanding when standard checks suffice, and when deeper investigation is mandatory, directly affects your practice’s compliance posture.

This article explains the practical differences between CDD and EDD, outlines the risk-based triggers that escalate standard verification to enhanced procedures, and explores how integrated identity verification can fit into your existing software stack without adding operational complexity.

CDD, EDD, and ECDD in plain English

The difference between customer due diligence vs enhanced due diligence comes down to risk. Your verification obligations scale based on who you’re onboarding, what transactions they’re running, and which red flags appear during checks. Australian AML/KYC regulations don’t require identical scrutiny for every client.

Standard customer due diligence explained

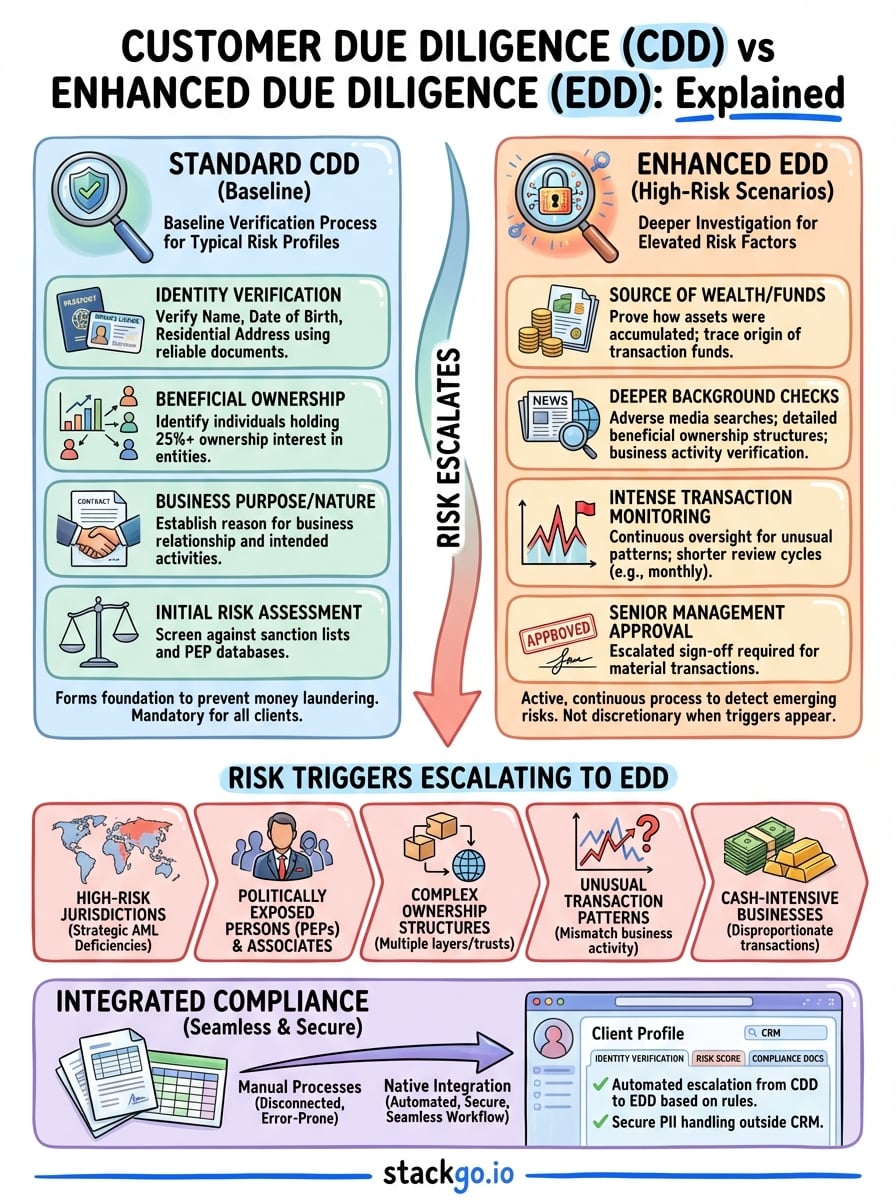

CDD represents your baseline verification process. When you onboard a typical client with a standard risk profile, CDD covers the mandatory checks that prove who they are, confirm they’re legitimate, and establish what they’re using your services for. This includes collecting identity documents, verifying those documents against authoritative sources, and screening the client against sanction lists and PEP databases.

Your CDD process captures four core elements: identity verification (name, date of birth, address), beneficial ownership for entities, business activity or purpose of the relationship, and initial risk assessment. Most accounting practices apply CDD to individual taxpayers, small businesses, and straightforward corporate structures where no elevated risk indicators appear.

Enhanced due diligence triggers

EDD kicks in when risk factors elevate a client beyond standard verification. You’re required to dig deeper, collect additional documentation, and implement ongoing monitoring that goes beyond your baseline CDD procedures. This isn’t optional when specific risk triggers appear.

Enhanced due diligence applies when client circumstances, transaction patterns, or jurisdictional factors push risk levels above your standard threshold.

Triggers include clients operating in high-risk jurisdictions, politically exposed persons and their associates, complex corporate structures involving multiple entities or trusts, unusual transaction patterns that don’t match stated business activities, and clients in industries designated as higher risk by AUSTRAC. Cash-intensive businesses, money services operations, and clients with prior adverse findings in background checks all warrant EDD treatment.

When due diligence escalates further

Some compliance frameworks reference extraordinarily complex or enhanced CDD for the highest-risk scenarios, though Australian regulations typically frame this within EDD rather than creating a separate tier. When you encounter clients presenting multiple high-risk factors simultaneously, your EDD procedures intensify further, requiring executive-level approval, continuous transaction monitoring, and source-of-funds verification for every material transaction.

The practical difference matters because each escalation adds verification depth, documentation requirements, and ongoing monitoring obligations to your compliance workload.

What standard CDD requires

Standard customer due diligence establishes your baseline verification process for clients who present typical risk profiles. Your CDD procedures must collect enough information to verify identity, understand the nature of the business relationship, and assess whether the client matches your expected risk parameters. These requirements apply universally across regulated businesses in Australia.

Core verification components

Your CDD process captures four mandatory elements. First, you verify the client’s identity using reliable and independent documentation, typically government-issued identification like passports or driver’s licences. Second, you confirm their residential address through utility bills, bank statements, or other official documents dated within the past three months.

Third, for business clients, you identify and verify beneficial owners who hold 25% or more ownership interest in the entity. Fourth, you establish the purpose and intended nature of the business relationship through declarations and supporting documentation that explain what services the client requires and why.

Standard CDD forms the foundation of your compliance framework, preventing your services from being used for money laundering or terrorist financing.

Documentation you must collect

You collect and retain specific documents for every CDD check. Identity documents include passports, driver’s licences, or national identity cards, which you verify against the original or certified copies. Proof of address requires recent utility bills, council rates notices, or bank statements showing the client’s residential address.

For entities, you obtain company registration certificates, trust deeds, partnership agreements, or other formation documents that establish the legal structure. When comparing customer due diligence vs enhanced due diligence, standard CDD stops here unless risk factors appear, whereas EDD extends verification into source of wealth, transaction monitoring, and deeper background checks that go beyond these baseline requirements.

What enhanced due diligence adds

Enhanced due diligence extends your verification process beyond the baseline CDD checks when risk indicators appear. Where standard customer due diligence confirms identity and basic legitimacy, EDD requires you to investigate source of wealth, scrutinise transaction patterns, and implement continuous monitoring that standard checks don’t demand. This additional layer protects your practice from sophisticated money laundering attempts that pass through basic verification.

Additional verification layers

You collect substantially more documentation under EDD. Source of wealth verification requires clients to demonstrate how they accumulated their assets through tax returns, investment statements, sale contracts, or inheritance documentation. Source of funds for specific transactions demands proof of where money originated, traced back through bank statements, business income records, or asset liquidation evidence.

Your background screening deepens to include adverse media searches across multiple jurisdictions, detailed beneficial ownership structures mapped through corporate registries, and verification of business activity claims against independent sources. When comparing customer due diligence vs enhanced due diligence, this documentation requirement separates the two most clearly.

Ongoing monitoring requirements

EDD mandates continuous oversight that standard CDD doesn’t require. You monitor transaction patterns for deviations from expected activity, flagging unusual volumes, frequencies, or destinations that don’t match the client’s stated business purpose. Your review cycle shortens from annual to quarterly or even monthly for highest-risk clients.

Enhanced due diligence transforms verification from a one-time onboarding check into an active, continuous process that detects emerging risks throughout the relationship.

You escalate approval requirements for material transactions, often requiring senior management or compliance officer sign-off before proceeding. This active monitoring catches changes in risk profile that static CDD processes miss entirely.

When you must step up to EDD

Your obligation to apply enhanced due diligence isn’t discretionary when specific risk factors appear. AUSTRAC’s AML/CTF regulations mandate EDD for defined circumstances, and failing to escalate verification when these triggers present exposes your practice to regulatory penalties. Understanding when customer due diligence vs enhanced due diligence applies protects both your compliance standing and your business from onboarding clients who carry unacceptable risk.

Risk triggers that mandate EDD

You must implement EDD when clients operate in high-risk industries designated by AUSTRAC, including money service businesses, precious metals dealers, gambling operations, and virtual currency exchanges. Complex ownership structures involving multiple layers of trusts, shell companies, or offshore entities trigger mandatory enhanced verification regardless of stated business purpose.

When politically exposed persons appear anywhere in your client relationship, whether as the client, beneficial owner, or close associate, enhanced due diligence becomes mandatory without exception.

Clients conducting cash-intensive transactions disproportionate to their stated business activities require EDD, as do those requesting services that don’t align with your understanding of their legitimate needs. Transaction patterns showing rapid movement of funds through multiple jurisdictions or accounts demand enhanced scrutiny.

Geographic and client-specific escalations

High-risk jurisdictions identified by FATF as having strategic AML deficiencies automatically trigger EDD for any client with operations, ownership, or significant transaction flows connected to these countries. Your client’s physical location, beneficial ownership nationality, and transaction destinations all count toward this assessment.

Clients previously flagged in adverse media searches, those with prior regulatory actions, or individuals appearing on sanctions lists require enhanced procedures before you proceed. Your risk assessment during standard CDD identifies these factors, but recognising them as EDD triggers ensures you escalate verification appropriately rather than proceeding with inadequate checks.

How to run CDD and EDD inside your systems

Running customer due diligence vs enhanced due diligence effectively requires embedding verification workflows directly into the software you already use daily. Manual processes involving spreadsheets, separate compliance portals, and disconnected verification tools create gaps where errors occur and documentation gets lost. Your compliance framework strengthens when identity checks, document collection, and risk assessments happen within your CRM or practice management system rather than forcing staff to switch between platforms.

Native integration vs manual workflows

You face a choice between native integrations that write verification outcomes directly into client records or manual processes that require copying data between systems. Manual workflows introduce transcription errors, delay onboarding, and leave incomplete audit trails that regulators flag during reviews. Staff toggle between multiple tabs, switching from your CRM to standalone verification platforms, then manually recording outcomes back into client files.

Native integrations eliminate this friction by reading contact information from your existing system, processing verification checks automatically, and writing outcomes directly into the same client record. Your team sees verification status, risk scores, and compliance documentation without leaving the software they already know.

Automation within your existing stack

You automate escalation from CDD to EDD when your integrated verification tool detects risk triggers during initial checks and immediately requests additional documentation based on predefined rules. This removes guesswork about when enhanced procedures apply.

Integrated compliance tools prevent your practice from becoming dependent on manual processes that break under volume and expose you to regulatory risk.

For Australian accounting firms, IdentityCheck integrates directly with platforms like HubSpot to verify client identities for TPB and AUSTRAC requirements without storing PII in your CRM. Your verification data remains secure in a privacy layer accessible only through multi-factor authentication while compliance outcomes appear automatically in client records.

Final takeaways

Understanding customer due diligence vs enhanced due diligence determines whether your verification processes meet regulatory obligations or leave compliance gaps. Your standard CDD procedures verify identity and establish baseline legitimacy for typical clients, while EDD escalates verification when risk factors appear. These triggers include high-risk jurisdictions, politically exposed persons, complex ownership structures, and unusual transaction patterns that your initial assessment reveals.

Running these processes manually creates operational bottlenecks and compliance risks that integrated verification eliminates. Your practice benefits when identity checks happen inside your existing CRM rather than forcing staff to manage separate platforms and manually transfer outcomes. IdentityCheck handles AUSTRAC Tranche 2 requirements directly within systems like HubSpot, automating escalation from CDD to EDD based on detected risk factors while keeping PII secure outside your primary software. This approach reduces errors, speeds onboarding, and ensures your compliance documentation stays complete without adding complexity to daily workflows.