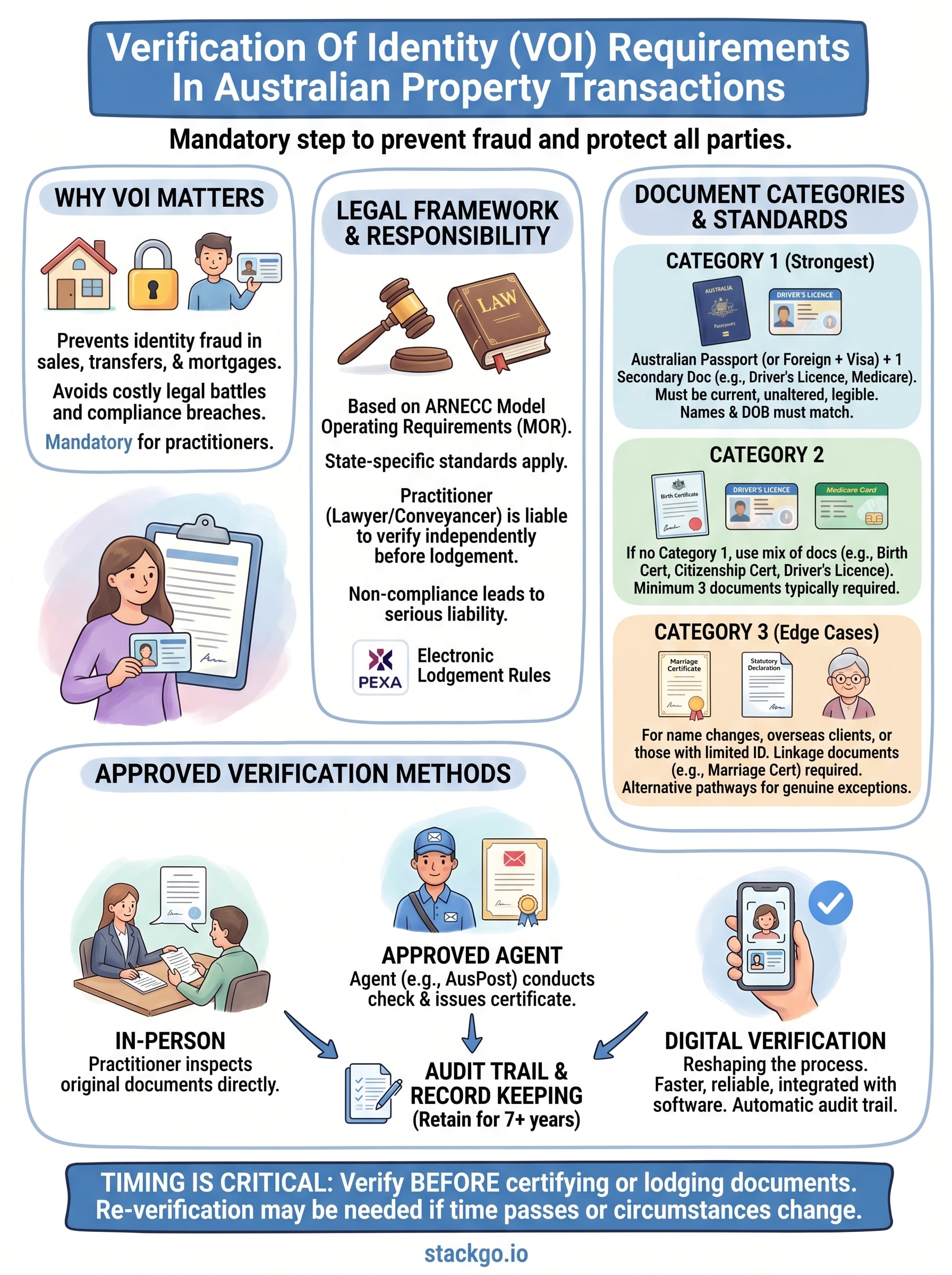

Every property transaction in Australia, whether it’s a sale, transfer, or mortgage, requires the parties involved to prove they are who they claim to be. This is where verification of identity (VOI) requirements come into play. VOI is a mandatory step in conveyancing and property dealings, designed to prevent identity fraud and protect all parties from unauthorised transactions. Get it wrong, and you risk delays, compliance breaches, or worse, facilitating fraud.

The rules around VOI aren’t uniform across the country. Each Australian state and territory sets its own standards for what documents are acceptable, how verification must be conducted, and who is authorised to carry it out. For lawyers, conveyancers, and the regulated professionals supporting them, understanding these requirements isn’t optional, it’s a core part of doing business compliantly.

This article breaks down the VOI requirements across Australia: the documents you need, the methods available, and the standards that apply. We also cover how digital identity verification is reshaping the process, making it faster and more reliable than traditional in-person checks. At StackGo, our IdentityCheck integration helps regulated businesses run identity verification directly from their existing software, no extra platforms, no manual data entry, so compliance workflows like VOI fit seamlessly into how your team already works.

Why VOI matters in Australian property transactions

Property fraud is a serious and growing problem in Australia. Identity-related fraud can result in someone fraudulently transferring or mortgaging your property without your knowledge, leaving you with a costly legal battle to resolve. VOI exists specifically to close this gap, requiring that every person involved in a property transaction proves their identity before a dealing can proceed.

The legal framework behind VOI

Australia’s approach to VOI in property transactions is anchored in the ARNECC (Australian Registrars’ National Electronic Conveyancing Council) Model Operating Requirements (MOR), which set the national baseline for identity verification in electronic conveyancing. Each state and territory has adopted these standards, with some local variations, through their own land title legislation. Practitioners using platforms like PEXA for electronic lodgement must follow subscriber rules that directly incorporate these requirements.

Failing to verify a client’s identity in line with the applicable state requirements exposes you, your firm, and your client to serious legal and financial liability.

Under these rules, the obligation to verify identity sits with the responsible practitioner, typically the lawyer or conveyancer acting in the transaction. You cannot rely on another party’s verification and must conduct your own independent checks.

What’s at risk without proper VOI

Title fraud and mortgage fraud are the two most common risks when identity verification is skipped or done poorly. In a title fraud scenario, a fraudster uses stolen identity documents to impersonate a property owner, then sells or mortgages the property and disappears with the funds. Recovering from this outcome is slow, expensive, and often requires court intervention.

Beyond fraud, non-compliance with verification of identity (VOI) requirements creates direct liability for practitioners. Regulators and professional indemnity insurers take a dim view of practitioners who cannot demonstrate they followed the correct verification process. If you cannot produce a clear audit trail showing how and when you verified a client’s identity, your professional cover and your firm’s reputation are both on the line.

Who must complete VOI and when it happens

The obligation to complete VOI sits with the practitioner acting in the transaction, not the client themselves. If you are a lawyer or conveyancer representing a buyer, seller, mortgagor, or mortgagee in a property dealing, you are responsible for verifying their identity before lodging any documents with the land titles office.

Practitioners who carry the obligation

Conveyancers and lawyers are the primary professionals required to meet verification of identity (VOI) requirements in Australian property transactions. If you are acting for a party in a sale, transfer, lease, mortgage, or discharge of mortgage, the obligation applies to you directly. Financial institutions such as banks and credit unions must also verify the identity of mortgagors before registering a mortgage over a property.

When verification must take place

Timing matters. You must complete VOI before you certify or lodge any documents with the relevant state land titles office. In electronic conveyancing environments like PEXA, this requirement is embedded directly into the subscriber rules, meaning you cannot progress a transaction without evidence of completed verification.

Leaving VOI until the last minute creates real risk: if a client cannot produce the right documents in time, your settlement date is in jeopardy.

Re-verification may be required if a significant period has passed since the original check, or if the client’s personal circumstances have materially changed since the last verification was completed. Always check the applicable state rules to confirm the timeframe that applies to your transaction.

VOI document categories and what counts as acceptable

The ARNECC VOI Standard organises acceptable identity documents into categories, and you must collect documents that together satisfy the required threshold. Most states require verification against Category 1 (an Australian passport or foreign passport with visa evidence, plus one supporting document) unless your client cannot produce those, in which case you move down the category list.

Primary and secondary document categories

Category 1 documents are the strongest: an Australian passport or foreign passport combined with a secondary document such as a driver’s licence or Medicare card. Category 2 accepts a broader mix of Australian-issued documents when a passport is unavailable, including a birth certificate, citizenship certificate, or driver’s licence. You typically need a minimum of three documents from Category 2 to meet the standard.

If your client cannot meet Category 1 requirements, document your reasoning clearly before moving to a lower category.

What the documents must show

Beyond collecting the right categories, each document must be current, unaltered, and legible. You need to confirm that the name and date of birth on the documents match across all items presented. Expired documents generally do not satisfy verification of identity (VOI) requirements, with very limited exceptions depending on your state.

For each check, you must also record and retain a copy of the documents inspected, along with the date, method, and outcome of the verification. Retention periods vary by jurisdiction but typically run for at least seven years after the transaction completes.

How VOI works in practice for buyers and sellers

For most buyers and sellers, the process is more straightforward than it sounds. Your lawyer or conveyancer contacts you early in the transaction, requests your identity documents, and arranges verification through an approved method. Most practitioners complete this step at the outset, before contracts are signed or lodged, so the check does not delay your settlement timeline.

The three approved methods

Verification of identity (VOI) requirements allow practitioners to verify clients through three main methods: in-person at the practitioner’s office, through an approved identity agent such as Australia Post, or via a digital verification solution. Each method must still meet the ARNECC document standard and record-keeping obligations.

Digital verification has become common for many firms because it removes the need for clients to travel and generates an automatic audit trail.

Your practitioner inspects your original documents directly during an in-person check, records the outcome, and retains copies. If you use an identity agent, they conduct the check on your behalf and issue a verification certificate that your practitioner keeps on file.

What you need to bring

Prepare your documents before your appointment. Bring your passport and driver’s licence as a starting point, since together they satisfy the Category 1 threshold in most states. If either is unavailable, gather two or three secondary documents to meet the applicable category requirement.

Common document combinations accepted across Australian jurisdictions include:

- Australian passport + driver’s licence

- Foreign passport + Medicare card + driver’s licence

- Birth certificate + driver’s licence + Medicare card (where no passport is available)

Edge cases: name changes, overseas, and missing ID

Not every client walks into a transaction with a current passport and matching driver’s licence. Real-world circumstances create complications that your verification process must account for, and the ARNECC standard makes some provisions for these situations.

Name changes and document mismatches

If your client has changed their name through marriage, divorce, or deed poll, their documents may show different names across categories. You need to collect a linkage document such as a marriage certificate or change of name certificate to bridge the gap. Keep this linkage document on file alongside the other identity records, and note clearly in your file how the names connect.

If you cannot establish a clear documentary link between a client’s current name and their identity documents, do not proceed until you can.

Overseas clients and remote verification

If your client is outside Australia, they can still satisfy verification of identity (VOI) requirements through an approved overseas identity agent, such as an Australian consulate or embassy officer. The agent conducts the check and issues a certificate confirming the documents inspected. Digital verification platforms that meet the ARNECC standard are also increasingly accepted for overseas clients, provided the solution is approved under your state’s rules.

When a client genuinely cannot produce enough ID

Some clients, particularly elderly individuals or recent migrants, may simply not hold enough documents to satisfy the standard categories. In these situations, your state rules may allow alternative verification pathways, such as a statutory declaration from a qualified witness combined with whatever documents your client can produce. Document your reasoning thoroughly, because any deviation from the standard categories requires a clear, defensible explanation on your file.

Next steps

Verification of identity (VOI) requirements in Australia sit at the intersection of compliance obligation and practical workflow. You now understand the legal framework, the document categories, the approved verification methods, and how to handle edge cases when clients cannot produce standard ID. The rules vary by state, but the core principle does not change: verify before you lodge, and document everything.

For conveyancers, lawyers, and accountants supporting property transactions, the biggest operational challenge is not understanding the rules but executing them consistently across every client, every time. Manual processes create gaps, missed steps, and audit trail problems that expose your firm to liability. A streamlined, integrated approach removes that risk.

If you want to run identity checks directly from your existing software without switching tabs or managing a separate platform, see how IdentityCheck works for compliance-driven businesses. You can also create a free account to test whether it fits your workflow.