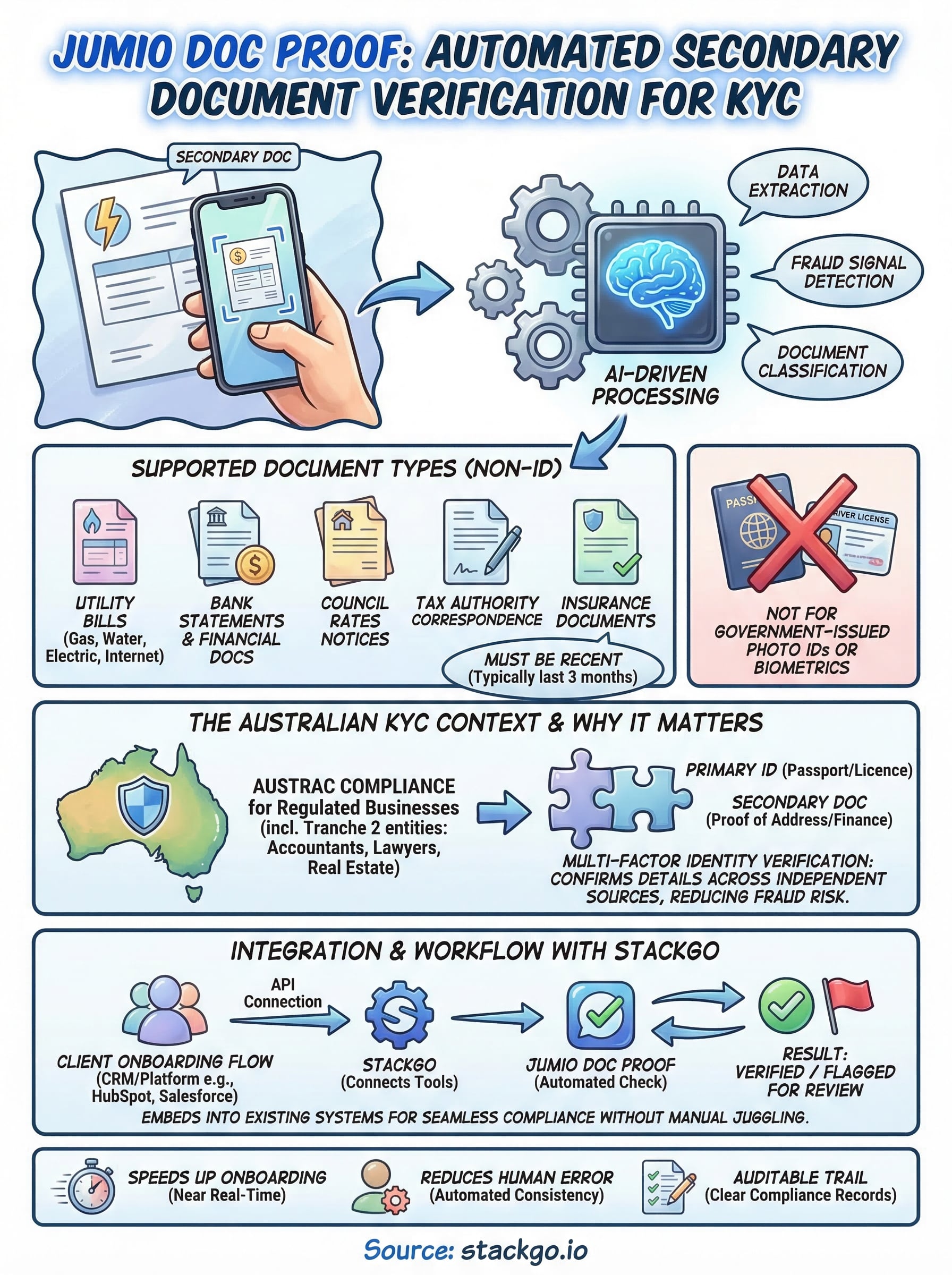

When verifying a client’s identity, checking their passport or driver’s licence is only half the picture. Regulated businesses often need to verify secondary documents, utility bills, bank statements, proof of address, to meet KYC and AML obligations. That’s where Jumio document verification comes in. Jumio’s Doc Proof product is built to handle exactly this: automated verification of supporting documents that sit outside standard government-issued IDs, giving compliance teams a reliable way to confirm client details without manual review.

Doc Proof uses a combination of AI-driven data extraction, fraud detection, and document classification to assess whether a submitted document is genuine. It covers a range of document types across multiple countries, which matters if your firm deals with international clients or cross-border transactions. For Australian accounting firms preparing for upcoming AUSTRAC AML/CTF requirements, or any regulated business already bound by KYC obligations, understanding how this technology works is a practical step toward tightening your compliance workflows.

At StackGo, we build integrations that connect verification tools like Jumio directly into your existing software, your CRM, your onboarding flows, so you’re not juggling separate platforms. This article breaks down how Jumio’s Doc Proof actually works, what document types it supports, and how it fits into a broader KYC process. Whether you’re evaluating Jumio as a standalone option or looking at how to embed document verification into your current tech stack, you’ll walk away with a clear picture of what’s on offer.

Why secondary document checks matter for KYC in Australia

Australia’s AML/CTF framework requires regulated businesses to verify the identity of their clients before providing services. The Anti-Money Laundering and Counter-Terrorism Financing Act 2006 sets the baseline, but the upcoming reforms expanding AUSTRAC’s reach to tranche-two entities (accountants, lawyers, and real estate agents) will push thousands more firms into mandatory KYC territory. A passport or driver’s licence tells you who someone claims to be. A secondary document, a utility bill, a bank statement, a rates notice, adds a layer of confirmation that a person’s details are consistent across multiple independent sources.

The role of secondary documents in a compliant identity check

Most KYC frameworks distinguish between primary identity documents (government-issued photo ID) and secondary documents (proof of address or financial standing). A robust identity verification process typically requires at least one of each. AUSTRAC’s guidance on customer identification procedures treats secondary documents as a key component of multi-factor identity verification, particularly when biometric checks alone are insufficient for higher-risk clients.

Relying solely on a single government-issued ID leaves a gap that fraudsters can exploit, especially when synthetic identities combine real ID data with fabricated address records.

Common secondary documents accepted in Australian KYC processes include:

- Utility bills (electricity, gas, water) issued within the last three months

- Bank or financial institution statements

- Local council rates notices

- ATO-issued correspondence

Why manual document review creates compliance risk

Reviewing secondary documents manually is slow and prone to human error. Staff may miss signs of tampering, accept expired documents, or fail to record outcomes consistently. When your firm processes dozens of onboarding checks each week, these small gaps accumulate quickly.

Tools like Jumio document verification automate classification, data extraction, and fraud signal detection, removing the inconsistency that manual review introduces. For firms preparing for AUSTRAC compliance, building that reliability into your process from the start is far easier than retrofitting it later.

What Jumio Doc Proof verifies and what it does not

Jumio document verification via Doc Proof focuses on non-ID supporting documents. It reads, classifies, and validates documents that confirm a person’s address, financial activity, or account details, rather than their government-issued identity. Understanding what falls inside and outside its scope helps you structure your onboarding process correctly from the start.

Document types Doc Proof supports

Doc Proof handles a defined set of secondary documents. The most common types include:

- Bank statements and financial institution documents

- Utility bills (electricity, gas, water, internet)

- Council rates notices

- Tax authority correspondence

- Insurance documents

Each submitted document goes through automated classification and data extraction, so the system identifies the document type before pulling key fields like name, address, and issue date.

What Doc Proof does not cover

Doc Proof is not designed to verify government-issued photo ID such as passports or driver’s licences. That function sits with Jumio’s separate ID verification product. The tool also does not perform biometric or liveness checks; it focuses entirely on document authenticity and data extraction for supporting materials.

Combining Doc Proof with a primary ID verification step gives you a more complete KYC picture than either product delivers on its own.

How Jumio document verification works step by step

When you submit a document, Jumio document verification runs it through a multi-stage automated process to confirm authenticity and extract key client data without manual review.

Document capture and classification

Your client uploads a photo or file directly. Doc Proof classifies the document type automatically, identifying whether it is a bank statement, utility bill, or rates notice before any extraction begins. This classification step matters because different document types carry different expected data fields.

Once classified, the system knows which fields to extract, keeping the process accurate rather than applying a generic template to every submission.

Data extraction and fraud signal detection

The system extracts key data points, including name, address, and issue date, then immediately runs fraud signal checks to scan for digital manipulation, inconsistent formatting, or data that conflicts with known templates for that issuer.

A document that fails fraud checks gets flagged for review rather than automatically accepted, giving your compliance team a clear audit trail.

Results return in near real time, so your onboarding flow does not stall. That speed makes Doc Proof practical for high-volume client onboarding.

How to integrate Doc Proof into your onboarding flow

Doc Proof connects to your existing onboarding stack via Jumio’s API, giving you flexibility to trigger document checks where they make the most sense. For most regulated businesses, that means placing a secondary document check immediately after primary ID verification, so both steps run as part of the same client journey rather than separate manual tasks.

Embedding verification at the right stage means clients complete compliance checks before they access your services, not after.

Connecting Doc Proof to your CRM or platform

Your integration approach depends on how your current onboarding flow is structured. If you use a CRM like HubSpot or Salesforce, a platform like StackGo handles the jumio document verification API connection without requiring custom development on your end.

Common integration trigger points include:

- After a prospect submits an onboarding form

- When a contact reaches a specific pipeline stage

- At the point of engagement letter sign-off

What to set up before you go live

Before activating Doc Proof, confirm your accepted document types match what your clients are likely to submit. Defining this clearly upfront reduces failed submissions and keeps your onboarding experience consistent.

You should also map out what happens when a check fails, whether your team receives an automatic alert or the client is prompted to resubmit a clearer document image.

Common failure reasons and how to fix them

Even well-structured onboarding flows hit verification failures. Most jumio document verification rejections trace back to a small set of recurring issues, and fixing them is straightforward once you know what triggers them. Addressing these proactively saves your compliance team from manual follow-up and delayed onboarding.

Poor image quality or incorrect file format

Blurry photos, cropped edges, and low-resolution scans are the most common reasons Doc Proof rejects a submission. Your clients often capture documents on mobile devices in poor lighting, which produces images the system cannot reliably extract data from.

Setting clear upload instructions at the start of your onboarding form reduces image quality failures significantly.

To reduce this failure type, communicate the following before clients upload:

- Capture the document flat on a plain, light-coloured surface

- Use natural or overhead lighting, not flash

- Ensure all four corners are visible in the frame

- Submit a JPEG or PDF at the resolution your platform specifies

Document is outside the accepted date range

Expired or outdated documents are another frequent failure point. Most KYC frameworks require supporting documents issued within the last three months, so a bank statement from six months ago will not pass. Prompt your clients to check the issue date before uploading, and build a clear rejection message that tells them exactly why the submission failed and what to resubmit instead.

Next steps

Jumio document verification gives regulated businesses a reliable way to confirm secondary documents without building manual review into every onboarding step. By combining Doc Proof with a primary ID check, you get a multi-factor verification process that meets KYC and AML expectations, reduces human error, and keeps your onboarding consistent across every client.

For Australian accounting firms and other tranche-two entities, the time to build this into your process is now, before AUSTRAC obligations land and force a rushed implementation. Getting your document verification workflow right early means you go live with confidence rather than retrofitting compliance into a system that was never built for it.

StackGo connects tools like Jumio directly into your existing CRM or onboarding platform, so your team runs checks without switching software or managing separate logins. If you want to see how it works in practice, explore how IdentityCheck handles AUSTRAC Tranche 2 AML/CTF compliance inside your current stack.