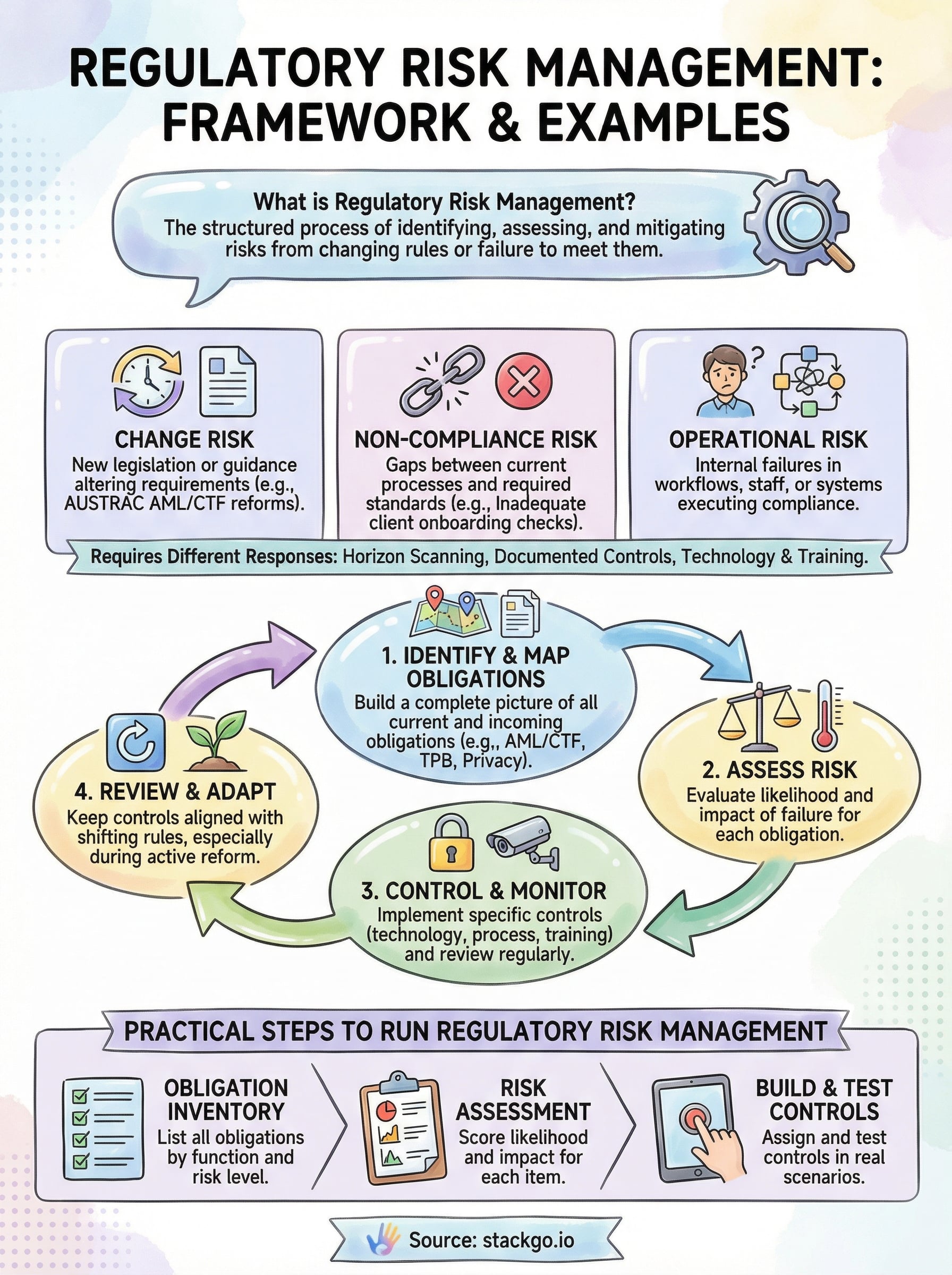

Every regulated business in Australia operates under a web of laws, licensing requirements, and industry standards that can shift with little warning. What is regulatory risk management? It’s the structured process of identifying, assessing, and mitigating the risks that arise when those rules change, or when your business falls short of meeting them. For accounting firms preparing for upcoming AUSTRAC AML/CTF obligations, and for any professional services firm already navigating TPB, ASIC, or APRA requirements, getting this right isn’t optional.

The challenge isn’t just knowing the rules. It’s building systems that keep pace with them, particularly around client onboarding, identity verification, and compliance workflows, without burying your team in manual processes. This is exactly where platforms like StackGo fit in, embedding KYC/AML checks directly into the tools you already use so that compliance becomes part of your operational rhythm, not a bolt-on afterthought.

This article breaks down the core framework behind regulatory risk management, walks through real-world examples relevant to Australian regulated industries, and explains how it differs from standard compliance risk. By the end, you’ll have a practical understanding of how to build a defensible, efficient approach to managing regulatory risk across your business.

What regulatory risk management covers

Regulatory risk management covers far more than tracking a compliance checklist. At its core, it addresses every area of your business that could be exposed to harm when laws change, regulators shift their focus, or your internal processes fail to keep pace. This includes licensing obligations, reporting requirements, data handling rules, and sector-specific conduct standards that apply to how you operate day to day.

The types of risk it addresses

Three distinct risk types sit within the broader regulatory risk landscape. The first is change risk, where new legislation or regulatory guidance alters what you must do, often on a short timeline. The second is non-compliance risk, where a gap between your current processes and the required standard creates exposure to fines, licence suspension, or reputational damage. The third is operational risk, where your internal workflows, staff, or systems fail to execute the compliance activities your obligations demand.

Understanding what is regulatory risk management means recognising that the risk does not only come from breaking the rules; it also comes from being unprepared when the rules move.

Each of these risk types demands a different response. Change risk requires active horizon scanning and engagement with industry bodies. Non-compliance and operational risk require documented controls, staff training, and technology that reduces human error in critical workflows like identity verification and client onboarding.

Where it shows up in practice

For Australian accounting firms, regulatory risk management shows up most visibly in AML/CTF obligations, TPB registration requirements, and privacy law compliance. If your firm onboards clients without a documented verification process, or stores sensitive identity data without proper controls, you carry both a compliance gap and a reputational liability that regulators are increasingly willing to act on.

Beyond accounting, regulated industries such as financial services, legal, and commercial real estate face similar exposure. The specific obligations differ, but the underlying principle stays constant: your business needs a structured, repeatable approach to identifying where regulatory risk sits and reducing it before it becomes a problem.

Regulatory risk vs compliance risk and legal risk

These three terms often get used interchangeably, but they describe different exposures that call for different responses. Treating them as one concept makes it harder to manage any of them well, and understanding what is regulatory risk management requires drawing a clear line between each category before you can build an effective framework.

Mixing up regulatory risk, compliance risk, and legal risk leads to gaps in your risk management strategy that regulators are well-positioned to find.

Compliance risk

Compliance risk is the risk that your internal processes, people, or systems fail to meet obligations that already exist and apply to your business today. If your client onboarding workflow doesn’t collect the required identity documents, that’s a compliance gap, not a regulatory change event. The rule was already in place; your process just didn’t reach it.

Closing this type of risk typically involves process redesign, staff training, and technology that reduces human error in high-stakes tasks like identity verification and AML screening.

Legal risk

Legal risk covers exposure to litigation, contractual disputes, or liability from third parties. Unlike regulatory risk, it doesn’t always involve a regulator or a licensing body. Your business could face legal risk from a contract dispute or a data breach that has no direct connection to industry-specific regulation.

The overlap appears when a regulatory breach triggers legal consequences, such as a fine that escalates into civil action or a licence suspension that causes measurable client losses. All three risk types compound quickly when your compliance systems are weak.

Why regulatory risk management matters in Australia

Australia’s regulatory environment is actively shifting across multiple industries at once. For accounting firms, the AUSTRAC AML/CTF regime expansion will bring tranche-two entities, including accountants, lawyers, and real estate agents, into mandatory anti-money laundering obligations for the first time. The legislative framework is already moving, and businesses that delay preparation will face rushed, error-prone implementation under real deadline pressure.

Understanding what is regulatory risk management becomes urgent when the window to build compliant systems is shorter than most firms expect.

AUSTRAC AML/CTF and tranche-two exposure

Accounting firms currently outside the AML/CTF reporting framework will need to implement structured compliance programs before obligations take effect. Each requirement connects directly to your client onboarding process. The core obligations your firm will need to address include:

- Customer due diligence at the point of onboarding and on an ongoing basis

- Suspicious matter reporting to AUSTRAC when indicators arise

- Record-keeping requirements tied to identity verification outcomes

If your current process relies on manual checks, you carry both a change risk and an operational risk that will be hard to close quickly.

TPB and the broader compliance picture

The Tax Practitioners Board already requires registered agents to meet verification and conduct obligations that touch client identity directly. Treating these as isolated tasks rather than part of a connected risk program misses how obligations compound.

Firms that manage AML/CTF and TPB requirements through a single integrated workflow reduce both cost and the chance of gaps appearing across their overall compliance posture.

A practical regulatory risk management framework

A workable framework for what is regulatory risk management doesn’t need to be complex, but it does need to be structured and repeatable. The goal is to give your business a clear method for spotting where regulatory risk sits, deciding how serious it is, and putting specific controls in place before a gap becomes a breach.

Identify and map your obligations

Your first step is building a complete picture of every regulatory obligation that currently applies to your business, including those that will apply once upcoming reforms like AUSTRAC AML/CTF take effect. This isn’t a one-time exercise. Obligations shift, and your map needs to shift with them.

A regulatory obligation you haven’t mapped is a risk your controls cannot reach.

A useful way to organise this is to group obligations by function and risk level:

- High-risk obligations: AML/CTF customer due diligence, identity verification at onboarding

- Ongoing obligations: TPB conduct requirements, AUSTRAC record-keeping, privacy compliance

- Horizon items: Tranche-two reforms, new ASIC guidance, sector-specific updates

Assess, control, and monitor

Once you have your obligation map, you need to assess the likelihood and impact of a failure in each area. Pair that assessment with a specific control, whether that’s a documented process, a technology integration, or a staff training requirement.

Reviewing your controls on a set cadence keeps them from drifting out of alignment with the rules they’re designed to meet. Annual reviews suit stable obligations, but active reform periods like the current AML/CTF expansion call for more frequent check-ins.

How to run regulatory risk management step by step

Knowing what is regulatory risk management at a conceptual level is only useful if you can translate it into repeatable operational steps. The process below gives you a working sequence to follow, whether you’re building your first risk program or tightening one that already exists.

Start with your obligation inventory

Before you can manage regulatory risk, you need a complete list of every obligation your business currently carries, including any that are incoming. Pull requirements from your licencing conditions, sector-specific legislation, and any guidance issued by relevant regulators such as AUSTRAC or the TPB. Group them by function and risk level so you can allocate your effort where the exposure is greatest.

An obligation inventory that isn’t updated regularly becomes a false sense of security rather than a genuine control.

Run your risk assessment

For each obligation, assess how likely a failure is and what the impact would be if one occurred. Score each item simply: high, medium, or low. This gives you a ranked list of where your controls need to be strongest. Your client onboarding and identity verification processes will almost always sit at the top of that list for regulated professional services firms.

Build and test your controls

Assign a specific control to each obligation, whether that’s a documented procedure, a technology integration, or a staff training requirement. Testing matters as much as building. Run your controls against real onboarding scenarios to confirm they hold under operational conditions, then set a review date before you move on.

Final takeaways

What is regulatory risk management at its core: a structured, repeatable process that keeps your business ahead of obligations, not scrambling to catch up after a breach. The firms that handle it well aren’t necessarily the ones with the largest compliance teams. They’re the ones with clear obligation maps, tested controls, and technology that removes the manual work from high-stakes tasks like identity verification and client onboarding.

Australia’s regulatory environment isn’t slowing down. AUSTRAC’s AML/CTF expansion is the most significant reform to hit professional services in years, and the window to build compliant systems before obligations land is narrowing. If your current onboarding process still relies on manual checks and disconnected tools, that’s the gap to close first.

StackGo’s IdentityCheck embeds KYC and AML verification directly into your existing software. See how IdentityCheck supports AUSTRAC Tranche 2 compliance and find out whether it fits your current stack.