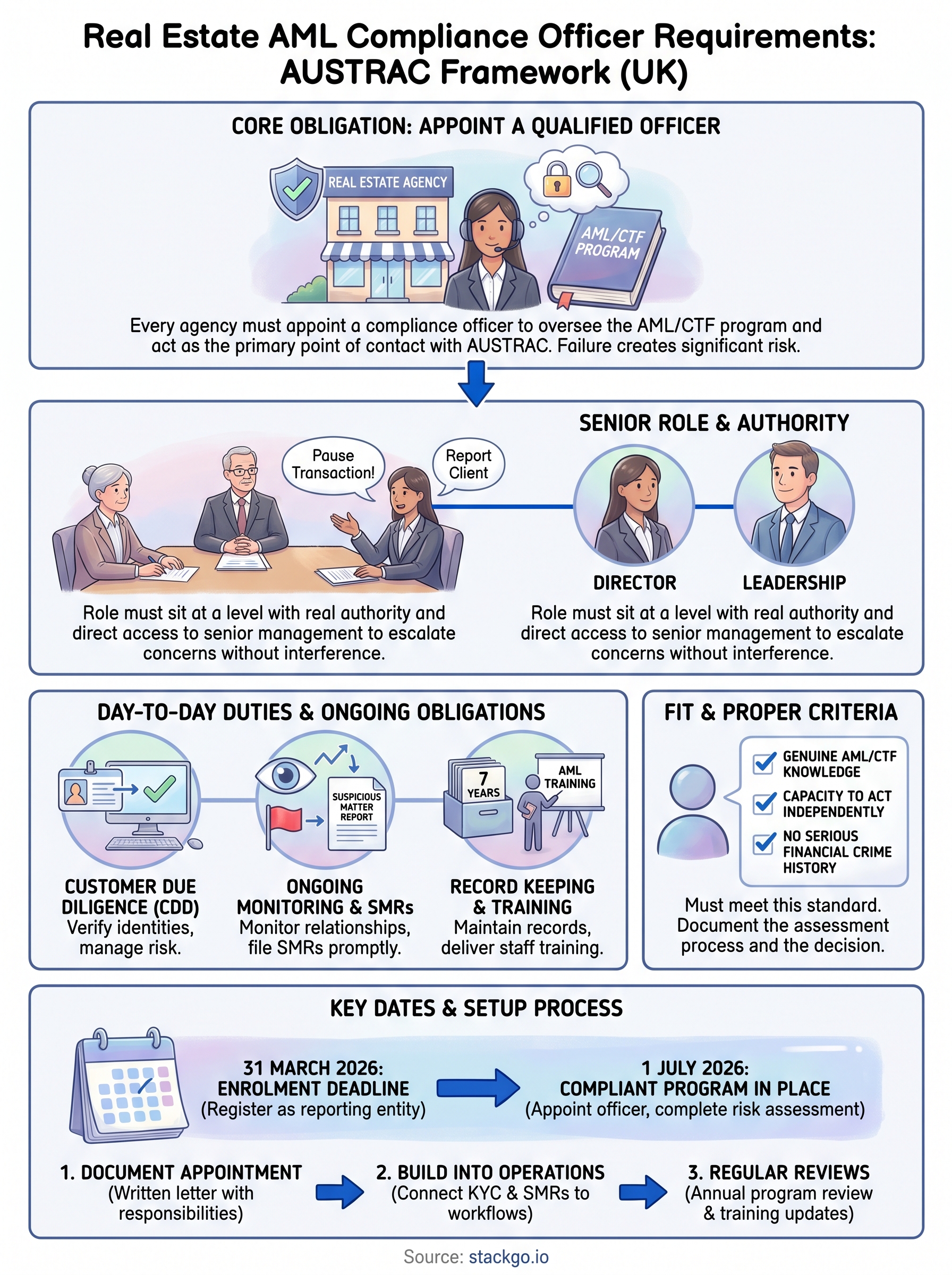

Australia’s AML/CTF regime is expanding to cover real estate, and with that comes a clear regulatory expectation: appoint a qualified compliance officer. Understanding real estate AML compliance officer requirements isn’t optional, it’s a core obligation under AUSTRAC’s framework that every agency needs to get right before enforcement begins.

The compliance officer role carries real weight. This person is responsible for overseeing your agency’s AML/CTF program, managing risk assessments, ensuring staff are trained, and acting as the primary point of contact with AUSTRAC. Getting the appointment wrong, or failing to make one at all, exposes your business to significant regulatory and financial risk.

This article breaks down who qualifies to serve as an AML compliance officer in a real estate agency, what the role actually involves day-to-day, and how to meet AUSTRAC’s expectations from the outset. We also cover how tools like StackGo’s IdentityCheck can support your compliance officer by streamlining identity verification (KYC) directly within your existing CRM, removing manual steps and reducing the kind of human error that triggers compliance failures.

What the AML compliance officer role covers

The AML compliance officer is the person inside your agency who owns your AML/CTF program and keeps it running. This isn’t a title you hand to someone as a formality. The role carries active, ongoing responsibilities that touch everything from customer due diligence to staff training to regulatory reporting. Under AUSTRAC’s framework, the compliance officer is the single accountable individual who ensures your agency meets its obligations under the AML/CTF Act.

Day-to-day responsibilities

When you look at the real estate AML compliance officer requirements in practice, the day-to-day work is more operational than most people expect. Your compliance officer is responsible for conducting and documenting customer due diligence (CDD) on clients, which includes verifying identities before providing designated services. They also manage ongoing monitoring of client relationships, escalate suspicious activity to AUSTRAC through Suspicious Matter Reports (SMRs), and maintain records in line with the seven-year retention requirement.

A compliance officer who only acts reactively, rather than maintaining active oversight, puts the entire agency at risk of regulatory breach.

Beyond reporting, your compliance officer needs to run regular AML/CTF training for all staff who interact with clients. This training must be documented and updated whenever your risk environment changes, for example, when you take on new property types or enter new markets.

Where the role sits in your agency

Your compliance officer must sit at a level where they have real authority and direct access to senior management. AUSTRAC expects this person to have the standing to escalate concerns, pause a transaction, or report a client without interference. Placing the role too low in your business structure creates a gap between compliance responsibility and operational power that regulators will notice.

The compliance officer also acts as the internal point of contact for AUSTRAC, which means they need to understand your reporting obligations, enrolment status, and how your AML/CTF program is structured. This requires genuine familiarity with your business, not just a surface-level knowledge of the regulations.

AUSTRAC requirements and key dates for real estate

Real estate agencies in Australia now fall under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act), following amendments that received Royal Assent in November 2024. These changes extend the regime to cover real estate professionals who facilitate the buying and selling of property. If your agency provides these services, you are a reporting entity and must meet all AUSTRAC obligations, including appointing a qualified compliance officer.

Key compliance deadlines

Meeting the real estate AML compliance officer requirements starts with understanding when obligations actually kick in. AUSTRAC has set 31 March 2026 as the enrolment deadline for real estate agencies, by which point your business must be formally registered as a reporting entity. Following enrolment, you have until 1 July 2026 to have a compliant AML/CTF program in place, which includes the formal appointment of your compliance officer and completion of your first risk assessment.

Missing the enrolment deadline leaves your agency operating as an unregistered reporting entity, which carries serious penalties under the AML/CTF Act.

These dates are firm, and AUSTRAC has made clear that regulated businesses will be expected to demonstrate readiness, not just intent. Starting your compliance officer appointment process now gives you the time to find the right person, document the role properly, and build your program before regulators begin scrutiny.

Who can be appointed and fit and proper criteria

AUSTRAC does not require your compliance officer to hold a specific formal qualification, but the person you appoint must meet a "fit and proper" standard. This means they need to demonstrate genuine knowledge of your AML/CTF obligations, the capacity to carry out the role independently, and no history of serious financial crime or regulatory breaches.

Appointing someone simply because they are available, rather than because they are capable, creates a compliance gap that AUSTRAC can identify quickly.

Who is eligible

Your compliance officer can be drawn from several roles within your agency, provided they hold enough authority to act without being overruled on compliance matters. Eligible appointments typically include:

- A director or principal of the agency

- A senior manager with direct access to leadership

- An employee with delegated compliance authority and documented decision-making power

What fit and proper means in practice

When assessing the real estate AML compliance officer requirements, fit and proper is not a checkbox. The individual must have no disqualifying criminal convictions, particularly for dishonesty or financial offences, and must be capable of understanding and applying your AML/CTF program in full.

You should document your assessment process and keep a clear record of why the appointed person meets this standard. AUSTRAC may ask you to demonstrate this during a review or audit, so written evidence of your decision carries real weight.

Core duties and ongoing AML and CTF obligations

Once appointed, your compliance officer carries a defined set of ongoing obligations that run continuously, not just at setup. Meeting the real estate AML compliance officer requirements means understanding that this role is active year-round, not something you revisit only when AUSTRAC makes contact.

Reporting and record-keeping

Your compliance officer must file Suspicious Matter Reports (SMRs) with AUSTRAC whenever a transaction or client behaviour raises a red flag. These reports must be submitted promptly, and the obligation to file exists even if a transaction does not proceed. All records related to customer due diligence, identity verification, and SMRs must be retained for a minimum of seven years under the AML/CTF Act.

Delayed or incomplete SMR filing is one of the most common compliance failures AUSTRAC identifies during audits.

Training and program reviews

Your compliance officer is responsible for delivering documented AML/CTF training to every staff member who interacts with clients or handles property transactions. This training must be reviewed and updated whenever your business changes, including new service lines, new staff, or shifts in your client risk profile. Your compliance officer must also conduct a formal review of your AML/CTF program at least annually to confirm it reflects your current risk environment and meets AUSTRAC’s standards.

How to set up the role in your agency

Setting up the compliance officer role correctly from the start saves you significant remediation work later. Before you make any appointment, you need to document the role formally and confirm that your chosen person meets the fit and proper standard outlined in your AML/CTF program.

Document the appointment

Your first step is to produce a written appointment letter that sets out the compliance officer’s responsibilities, authority level, and reporting lines within your agency. This document gives AUSTRAC clear evidence that your business has taken the real estate AML compliance officer requirements seriously and assigned genuine accountability to a named individual, rather than leaving the role undefined.

Keep your appointment documentation alongside your AML/CTF program so both are available immediately if AUSTRAC requests a review.

Build the role into your operations

Once you have documented the appointment, integrate the compliance officer’s responsibilities into your day-to-day operational workflows. This means connecting your identity verification process, your CDD records, and your SMR filing procedures directly to the role so nothing falls through the gaps. Practical tools like StackGo’s IdentityCheck let your compliance officer run KYC checks from within your existing CRM, keeping verification records accurate and audit-ready without adding manual steps or requiring staff to switch between multiple platforms.

Next steps for your agency

Your agency has already passed the 31 March 2026 enrolment deadline, which means your immediate focus should be on having a compliant AML/CTF program in place before AUSTRAC begins active scrutiny of the real estate sector. If you have not yet formally appointed a compliance officer, that appointment needs to happen now, with written documentation and a completed fit and proper assessment on file.

Meeting the full scope of real estate AML compliance officer requirements is easier when your verification process runs directly inside the tools your team already uses. StackGo’s IdentityCheck connects KYC checks to your existing CRM, so your compliance officer has accurate, audit-ready records without managing separate platforms or chasing manual paperwork.

Start by reviewing your current onboarding workflow and identifying where identity verification gaps exist. Then explore how IdentityCheck supports AUSTRAC Tranche 2 compliance to see how it fits your agency’s setup.