Australia’s AML/CTF reforms are bringing accountants under AUSTRAC’s regulatory umbrella, and the first question most practitioners ask is straightforward: which of my services are actually caught? The answer sits in the concept of AML/CTF designated services for accountants, a defined list of professional activities that trigger compliance obligations under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 and its upcoming amendments.

Getting this list wrong, or ignoring it, isn’t a minor oversight. If a service you provide qualifies as a designated service, you’ll need a compliant AML/CTF program, customer identification procedures, ongoing monitoring, and suspicious matter reporting. Misclassifying your services means either unnecessary compliance spend or, worse, regulatory exposure you didn’t see coming.

This article sets out the full list of designated services relevant to accounting professionals, explains what each one means in practice, and helps you assess where your firm sits. At StackGo, we build identity verification tools that integrate directly into your existing software, so once you’ve identified your obligations, you can meet them without bolting on yet another disconnected platform. But first, let’s get clear on exactly which services are covered.

Why designated services matter for accountants

Accounting has historically sat outside Australia’s formal AML/CTF framework. The reforms bringing tranche 2 entities, including accountants, into the regulated population mean the question of whether your services qualify as designated services is no longer academic. It determines whether AUSTRAC holds direct regulatory authority over your firm and whether you face obligations that carry genuine legal weight, not just professional guidance.

The shift from voluntary to mandatory

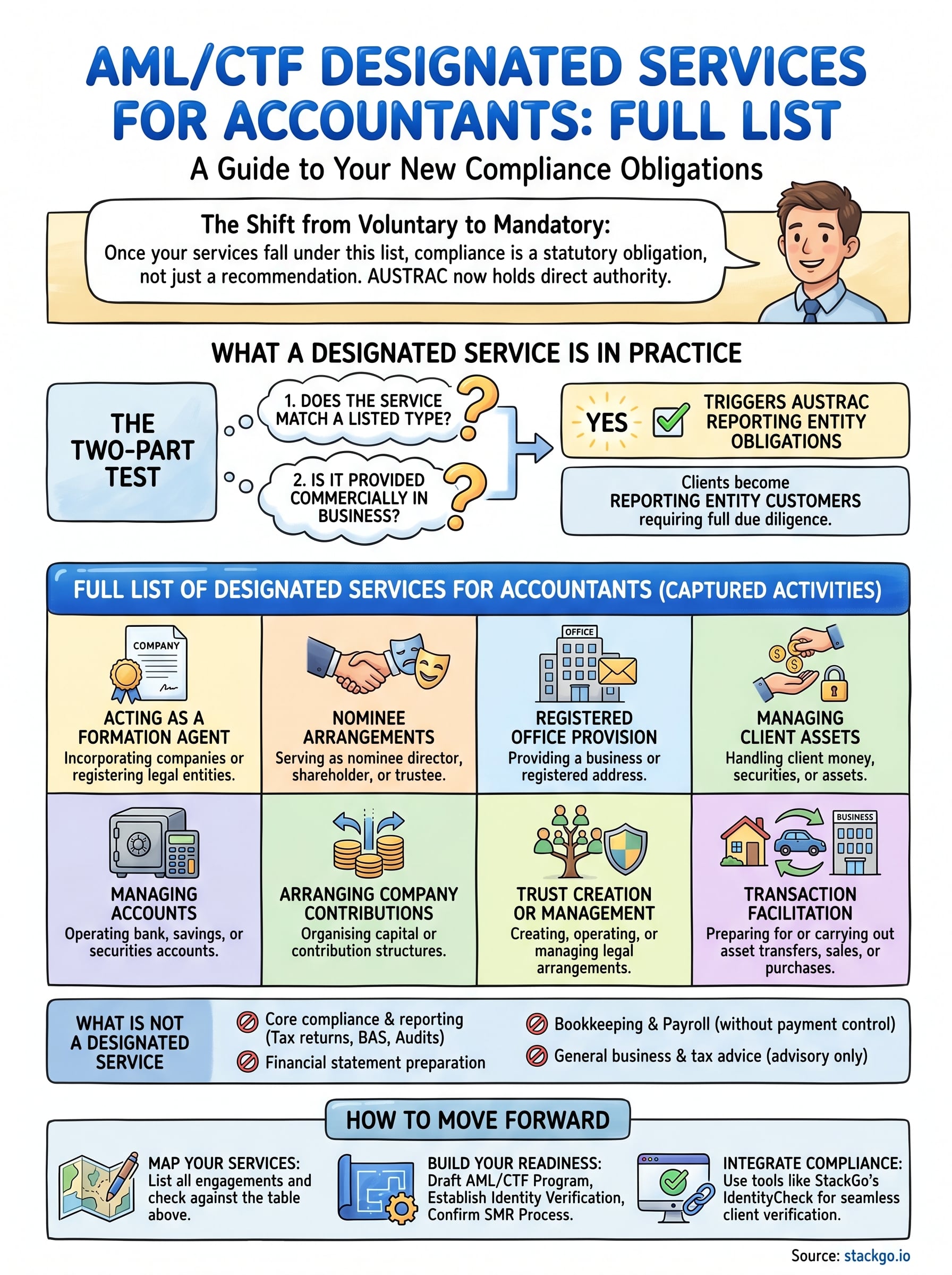

Until the legislative reforms take full effect, most Australian accountants have engaged with AML/CTF only in a general professional sense, drawing on guidance from bodies like CPA Australia or Chartered Accountants ANZ. The upcoming changes shift that entirely. Once your services fall within the AML/CTF designated services for accountants category, compliance becomes a statutory obligation rather than a recommended practice.

If any of your services qualify as a designated service, you must have a written AML/CTF program in place before you provide that service to a customer.

This is a significant operational change for most accounting firms. You’ll need customer due diligence (CDD) procedures, records of identity verification, and a functioning process for filing suspicious matter reports (SMRs) with AUSTRAC when required. Firms that have never encountered these requirements before will need to build these systems from the ground up, or find a way to embed them into existing client workflows without creating a parallel compliance burden.

What’s at stake if you get it wrong

Misidentifying your obligations cuts two ways. If you incorrectly assume a service you provide is not a designated service, you risk operating without a required AML/CTF program, which AUSTRAC can investigate and penalise. Civil penalties under the AML/CTF Act are substantial, and AUSTRAC has shown it will act against non-compliant entities in regulated sectors.

The second risk is less visible but equally expensive. If you over-scope your compliance program and treat every service as captured when most are not, you’ll spend time and money building obligations you don’t actually have. Getting the list right matters because it defines the entire scope of what you need to build: which clients require identity verification, what records you must keep, what staff need training on, and what your onboarding process looks like. Knowing exactly where your obligations start and stop is the only way to build a compliance program that is both legally sound and operationally proportionate.

What a designated service means in practice

Under the AML/CTF Act, a designated service is a specific type of service that, when provided to a customer in the course of carrying on a business, triggers the full suite of AUSTRAC reporting entity obligations. The definition is not about your job title or your professional licence. It focuses on the activity itself: what you are actually doing for the client, not how you describe it.

The two-part test

To determine whether you’re providing a designated service, apply a straightforward two-part test. First, ask whether the service matches a type listed in the relevant schedule of the AML/CTF Act. Second, ask whether you provide that service in the course of carrying on a business in Australia. Both conditions must be satisfied. A one-off favour to a family member is not the same as the same activity delivered commercially and repeatedly to paying clients.

The threshold is the commercial delivery of a listed service, not the professional intent behind it.

How the service definition affects your clients

Once a service qualifies, every client who receives that service from you becomes a reporting entity customer for the purposes of the Act. That means you must apply customer due diligence before or during the provision of the service, collect and verify identifying information, and keep records for at least seven years. The definition does not scale based on how much you charge, how complex the transaction is, or how long you have known the client. If the service type is captured and you provide it commercially, the obligations apply in full from the first time you deliver it.

Full list of designated services for accountants

Australia’s AML/CTF reforms identify specific professional activities that constitute AML/CTF designated services for accountants. The list focuses on services where an accountant controls or directs money, assets, or legal structures on behalf of a client, because these activities create genuine exposure to money laundering and terrorism financing risk.

The services listed below are drawn from the proposed reforms to the AML/CTF Act covering tranche 2 entities, including accounting professionals operating in Australia.

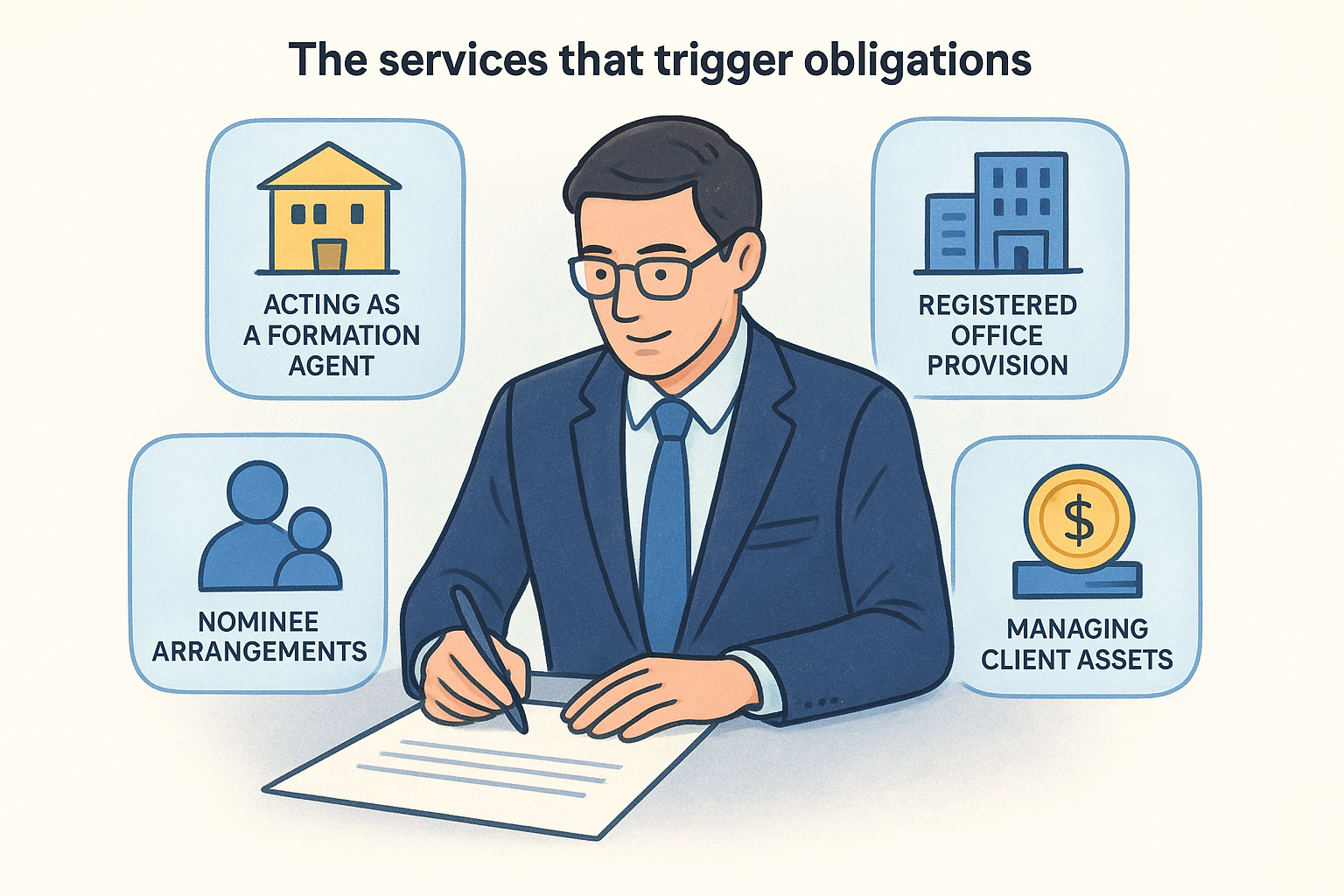

The services that trigger obligations

The following activities, when provided commercially to clients, bring your firm within AUSTRAC’s regulatory scope:

| Designated Service | What It Covers |

|---|---|

| Acting as a formation agent | Incorporating a company or registering another legal entity on behalf of a client |

| Nominee arrangements | Serving as a nominee director, nominee shareholder, or trustee for a client |

| Registered office provision | Providing a business or registered address for a company or legal entity |

| Managing client assets | Handling client money, securities, or other assets on their behalf |

| Managing accounts | Operating or controlling bank, savings, or securities accounts for a client |

| Arranging company contributions | Organising capital or contribution structures for company creation |

| Trust creation or management | Creating, operating, or managing a legal arrangement such as a trust |

| Transaction facilitation | Preparing for or carrying out transactions involving real property sales, business purchases, or asset transfers |

What connects these services

Each service listed above gives you direct control or significant influence over a client’s financial or legal structure. That common thread, rather than your accounting licence itself, is what places these activities inside the regulated perimeter. If you carry out any of these tasks commercially and repeatedly, AUSTRAC treats you as a reporting entity for those activities.

What is not a designated service for accountants

Understanding the boundaries of AML/CTF designated services for accountants is just as important as knowing what is captured. The regulated perimeter draws around activities where you take control of a client’s money, assets, or legal structures. If your work stays on the advisory or reporting side of that line, your core accounting services do not trigger AUSTRAC obligations on their own.

The regulated perimeter captures control and facilitation of financial structures, not the professional advice or reporting work that surrounds them.

Core compliance and reporting work

Preparing tax returns, lodging BAS statements, conducting audits, and producing financial statements are not designated services. These activities involve analysing and reporting on a client’s financial position, but you are not directing or controlling their money or legal arrangements. The same applies to management accounting, budgeting, and performance reporting. You’re advising on the numbers, not moving them.

Bookkeeping services fall into the same category. Recording transactions, reconciling accounts, and maintaining ledgers do not give you the kind of direct control over client assets that the AML/CTF framework is designed to address. Even payroll processing, where you calculate amounts owed, sits outside the captured list provided you are not operating the actual payment mechanism.

General business and tax advice

Providing tax planning advice, structuring recommendations, and general business consulting are also outside the designated services list. You might advise a client on the most effective way to structure an acquisition, but if you are not the one executing the transaction or managing the assets, the advisory work alone does not bring you under AUSTRAC’s scope. The trigger is always the hands-on delivery of a listed activity, not the conversation around it.

How to check if you are captured and get ready

The fastest way to assess your position is to list every service your firm currently offers and match each one against the designated services table above. You don’t need a lawyer to start this process. Pull your standard engagement types and ask, for each one, whether you are controlling or directing client money, assets, or legal structures. If the answer is yes, cross-reference with the table before you go any further.

Map your services against the list

Go through each client engagement type your firm runs regularly and write down what you actually do, not what you call it. An engagement described as "business advisory" might include acting as a nominee director or managing a trust, both of which are AML/CTF designated services for accountants.

If even one service you provide matches the list, you are a reporting entity for that service and the full set of obligations applies.

The label on an engagement matters far less than the underlying activity you are performing. A single captured service, even a minor part of your overall work, makes you a reporting entity for that activity and brings with it every compliance requirement attached to that status.

Build your readiness steps

Once you know which services are captured, move on three fronts before you provide those services to any new client. First, draft a written AML/CTF program that covers risk assessment, customer due diligence procedures, and staff training. Second, establish a customer identification and verification process that runs at the start of each captured engagement. Third, confirm how your firm will file suspicious matter reports with AUSTRAC when a client’s behaviour or transaction raises concern.

A simple way to move forward

Once you know which of your services qualify as AML/CTF designated services for accountants, the practical challenge shifts to execution. Building a compliant customer identification process doesn’t have to mean learning new software or managing a separate compliance platform. StackGo’s IdentityCheck integrates directly into the tools you already use, so you can verify client identities and write outcomes back to your CRM without switching tabs or duplicating data.

Your compliance program needs to work at the point of onboarding, not as a separate step that staff skip under pressure. IdentityCheck runs the verification check inside your existing workflow, keeps personally identifiable information out of your CRM, and gives you a clear audit trail for AUSTRAC purposes.

Take the next step and explore how IdentityCheck supports AUSTRAC Tranche 2 compliance, or create a free account to run a live identity check against your actual onboarding workflow before committing to anything.