Getting customer due diligence right isn’t just about ticking compliance boxes, it’s about protecting your business from financial crime while building trust with legitimate clients. For accounting firms and regulated businesses across Australia, a clear customer due diligence process flow serves as the backbone of effective KYC/AML compliance.

Yet many firms still rely on fragmented manual processes that create gaps, slow down client onboarding, and increase the risk of costly errors. Whether you’re preparing for AUSTRAC’s upcoming AML/CTF requirements or strengthening existing TPB compliance, understanding each stage of the CDD workflow is essential.

This guide breaks down the step-by-step stages of customer due diligence, from initial identification through to ongoing monitoring. We’ll also explore how integration platforms like StackGo help streamline identity verification directly within your existing CRM, eliminating disconnected systems and tedious manual data entry.

What customer due diligence covers

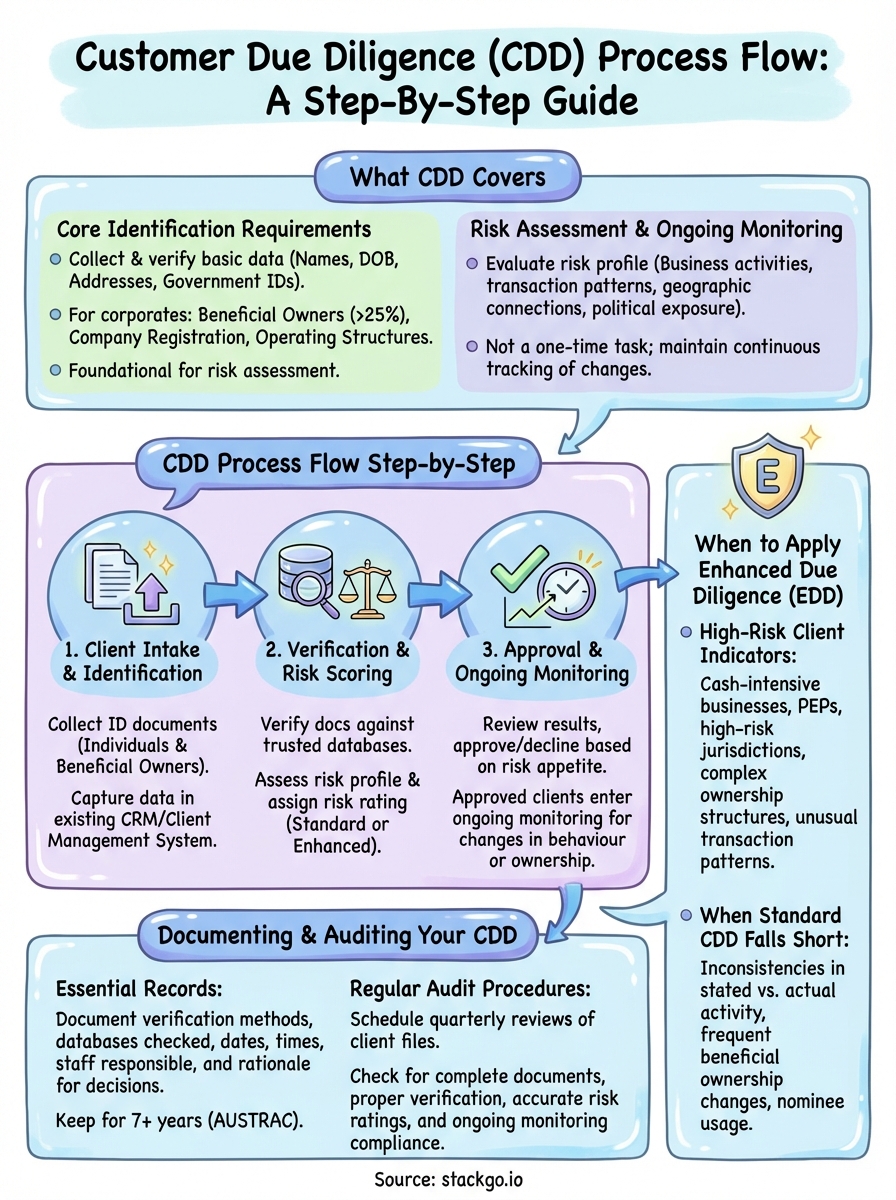

Customer due diligence covers three fundamental areas that work together to verify who your clients are and assess the risks they present. You need to collect identity information, verify that information against trusted sources, and then evaluate the potential for money laundering or terrorist financing based on what you’ve discovered. This process applies to every new client relationship and triggers again when circumstances change significantly.

Core identification requirements

At the foundation level, you must collect and verify basic identity data for all clients. This includes full legal names, dates of birth, residential addresses, and government-issued identification documents. For corporate clients, you also need to identify beneficial owners who hold 25% or more of ownership or control, along with company registration details and operating structures.

Your customer due diligence process flow starts with gathering this baseline information before you can assess risk or make decisions about the relationship. Without proper identification, you can’t move forward with onboarding.

You cannot conduct meaningful risk assessment until you’ve established and verified your client’s true identity.

Risk assessment and ongoing monitoring

Beyond identification, CDD requires you to evaluate each client’s risk profile based on factors like their business activities, transaction patterns, geographic connections, and political exposure. High-risk indicators might include cash-intensive businesses, operations in sanctioned jurisdictions, or connections to politically exposed persons.

This assessment isn’t a one-time task. You need to maintain ongoing monitoring that tracks changes in client behaviour, updates to beneficial ownership, and shifts in risk factors throughout the relationship. Regular reviews help you spot suspicious activity early and ensure your initial risk assessment remains accurate as circumstances evolve.

Why CDD needs a clear process flow

Without a documented customer due diligence process flow, your team makes inconsistent decisions that create regulatory gaps and expose your firm to unnecessary risk. Each staff member might apply different standards for identity verification, skip crucial risk assessment steps, or fail to escalate high-risk clients appropriately. This inconsistency becomes particularly dangerous during AUSTRAC audits, where regulators expect to see standardised procedures applied uniformly across all client relationships.

Preventing costly errors and delays

Manual CDD processes introduce human error at every stage, from mistyped client names to missed beneficial ownership checks or forgotten risk assessments. Staff might verify documents using different standards, lose track of which clients need enhanced due diligence, or fail to update records when circumstances change. These mistakes compound over time, creating a compliance backlog that becomes increasingly difficult to resolve.

A clear process flow eliminates guesswork and ensures every client moves through the same verification stages regardless of who handles their onboarding.

Building defensible compliance records

Regulators demand documented evidence that you’ve applied appropriate due diligence to each client relationship. A structured process flow creates an audit trail showing exactly what checks you performed, when you performed them, and who approved each stage. This documentation protects your firm during regulatory reviews and demonstrates you take AML/CTF obligations seriously rather than treating compliance as an afterthought.

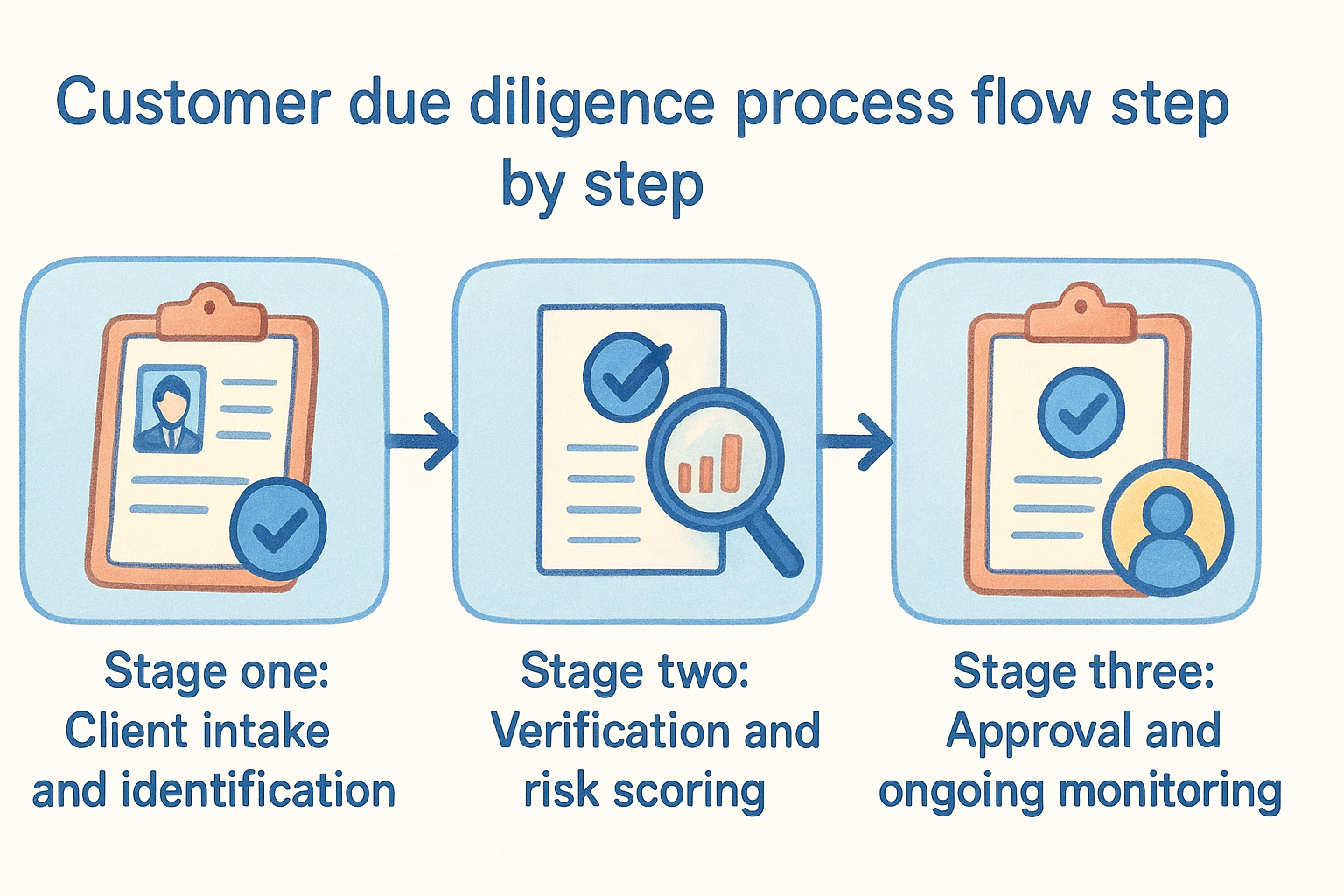

Customer due diligence process flow step by step

Your customer due diligence process flow breaks down into three distinct stages that move clients from initial contact through to active monitoring. Each stage builds on the previous one, creating a systematic approach that reduces errors and ensures consistent compliance across your entire client base.

Stage one: Client intake and identification

You begin by collecting identity documentation from the client and any beneficial owners. This includes government-issued IDs, proof of address, and corporate registration documents for business entities. Your team captures this information within your existing CRM or client management system, creating a single source of truth for all verification data.

Stage two: Verification and risk scoring

Next, you verify the collected documents against trusted databases and identity verification services. This step confirms the client exists, the documents are legitimate, and the information matches official records. You then assess the risk profile based on factors like business type, transaction patterns, and geographic connections to assign an appropriate risk rating.

Your risk assessment determines which clients require enhanced due diligence and how frequently you need to review their information.

Stage three: Approval and ongoing monitoring

Finally, you review the verification results and approve or decline the relationship based on your firm’s risk appetite. Approved clients enter ongoing monitoring, where you track changes in ownership, business activities, or transaction patterns that might elevate their risk profile or trigger additional verification requirements.

When to apply enhanced due diligence

Enhanced due diligence kicks in when your standard verification process doesn’t adequately address elevated money laundering or terrorism financing risks. You need to apply EDD when specific risk triggers appear during your customer due diligence process flow, requiring deeper investigation into the client’s background, funding sources, and intended business activities.

High-risk client indicators

You must implement enhanced due diligence for clients who operate cash-intensive businesses like money services, casinos, or precious metals dealers. Politically exposed persons (PEPs) and their family members also trigger EDD requirements, as do clients with business connections to high-risk jurisdictions identified by FATF or AUSTRAC.

Complex ownership structures that obscure beneficial owners, clients who refuse to provide complete documentation, or those with unusual transaction patterns that don’t match their stated business purpose all warrant enhanced scrutiny.

Enhanced due diligence isn’t optional when risk indicators appear; it’s a regulatory requirement that protects both your firm and the financial system.

When standard CDD falls short

Your risk assessment during initial onboarding might reveal inconsistencies in the client’s stated activities versus their actual behaviour. Clients requesting services that seem disproportionate to their business size, those with frequent changes in beneficial ownership, or entities operating through nominees all require the additional verification steps that enhanced due diligence provides.

How to document and audit your CDD

Your customer due diligence process flow only protects your firm when you maintain complete records of every verification step and decision made. AUSTRAC requires you to keep detailed documentation for at least seven years, including copies of identification documents, verification results, risk assessments, and any decisions to apply enhanced due diligence. Missing or incomplete records leave you exposed during regulatory reviews and make it impossible to defend your compliance decisions.

Essential records to maintain

You need to document the specific verification methods used for each client, including which databases you checked, what documents you reviewed, and who approved the onboarding. Your records must show the date and time of each verification step, the staff member responsible, and the rationale behind risk ratings or enhanced due diligence decisions.

Complete documentation proves you followed your procedures consistently rather than making arbitrary decisions about client relationships.

Regular audit procedures

Schedule quarterly reviews of a sample of client files to verify your team applies the customer due diligence process flow correctly. Check that staff collected all required documents, performed proper verification, assigned accurate risk ratings, and completed ongoing monitoring on schedule. Flag any gaps or inconsistencies immediately and retrain staff where procedures weren’t followed correctly.

Where to go from here

You’ve now mapped out a complete customer due diligence process flow that covers identification, verification, risk assessment, and ongoing monitoring. The real challenge shifts from understanding regulatory requirements to implementing these procedures efficiently within your existing business systems. Manual processes scatter client data across spreadsheets, email chains, and disconnected verification platforms, creating the exact gaps and inconsistencies that AUSTRAC auditors target during regulatory reviews.

StackGo’s IdentityCheck eliminates this fragmentation by running identity verification and risk assessment directly within your CRM. Your team completes full verification checks, document validation, and AML screening without switching between multiple platforms or manually re-entering client information. The system writes results back to your contact records, maintaining a complete audit trail within your existing workflow. Explore how IdentityCheck handles AUSTRAC Tranche 2 requirements inside the software you already use, or create a free account to test the platform.