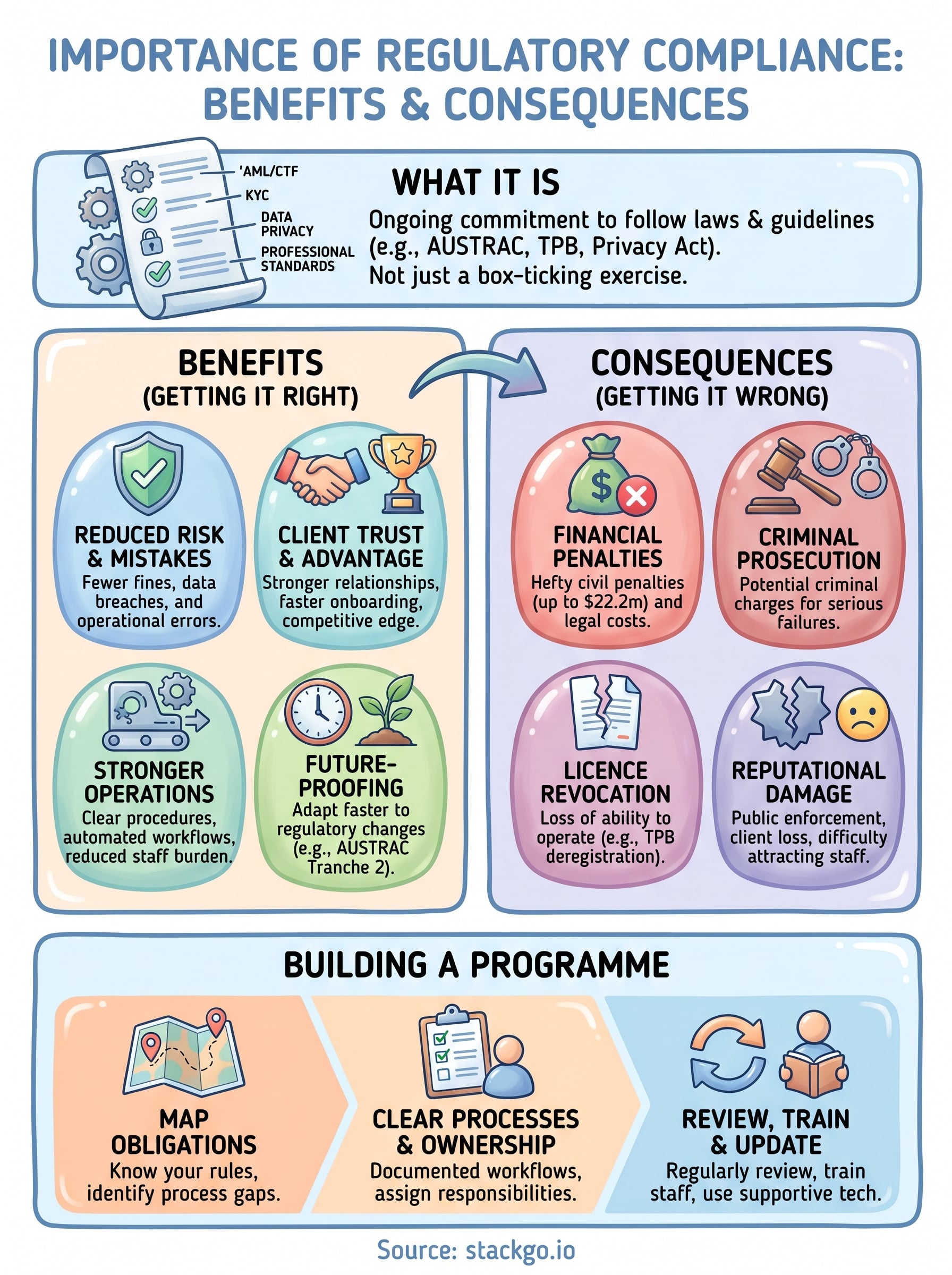

Every regulated business in Australia operates under a web of legal obligations, from AML/CTF requirements to TPB regulations for accountants, and sector-specific rules that seem to multiply each year. Understanding the importance of regulatory compliance isn’t optional; it’s the foundation that determines whether a business can continue operating, maintain client trust, and avoid penalties that range from hefty fines to criminal prosecution and licence revocation.

Yet compliance isn’t just about dodging consequences. Businesses that treat it as a genuine priority, rather than a box-ticking exercise, often find themselves with stronger client relationships, cleaner operations, and a competitive edge over firms that cut corners. The benefits are real and measurable, from reduced operational risk to faster, more confident client onboarding.

The challenge most firms face isn’t a lack of awareness. It’s execution. Manual compliance processes, disconnected software tools, and human error turn what should be a straightforward workflow into a time-consuming liability. That’s exactly why we built StackGo, to let businesses run identity verification, KYC, and AML checks directly from the software they already use, without juggling separate platforms or stitching together unreliable automations. Compliance becomes part of the workflow, not a disruption to it.

This article breaks down why regulatory compliance matters, what businesses stand to gain by getting it right, and what’s at stake when they don’t. Whether you’re an accounting practice preparing for AUSTRAC’s upcoming AML/CTF obligations or a professional services firm tightening your onboarding process, you’ll walk away with a clear picture of the risks, rewards, and practical realities of staying compliant.

What regulatory compliance covers in practice

Regulatory compliance refers to the process of following the laws, regulations, guidelines, and specifications relevant to your business operations. In Australia, these obligations come from multiple directions: federal legislation, industry regulators, professional bodies, and in some cases international standards. The importance of regulatory compliance sits in understanding that this isn’t a single checkbox; it’s an ongoing commitment that touches almost every part of how your business operates day to day.

Legal and industry-specific obligations

Every industry carries its own regulatory burden, and knowing which rules apply to your business is the essential starting point. For accounting firms, the Tax Practitioners Board (TPB) sets standards around client verification and professional conduct. Businesses captured under AUSTRAC’s AML/CTF Act must implement a compliance programme, conduct customer due diligence, and report suspicious matters. Financial services firms face obligations under the Corporations Act and ASIC, while businesses handling personal information must comply with the Privacy Act 1988 and the Australian Privacy Principles.

Regulatory obligations don’t exist in isolation. Each one connects to a broader framework designed to protect consumers, financial systems, and public trust.

The types of compliance your business must manage typically fall into several key categories:

- AML/CTF compliance: Anti-money laundering and counter-terrorism financing rules, enforced by AUSTRAC

- KYC obligations: Know Your Customer checks to verify client identity before providing services

- Data privacy: Requirements under the Privacy Act to handle personal information securely and transparently

- Professional conduct standards: Rules set by bodies like the TPB or state-based legal services commissions

- Workplace law: Fair Work Act obligations and work health and safety requirements

Internal policies and controls

External legal obligations give you the framework, but compliance in practice means translating those requirements into internal policies, workflows, and controls that your team actually follows. This includes documented procedures for client onboarding, staff training on how to handle sensitive information, and maintaining records that demonstrate you’ve met your obligations when a regulator asks.

Your internal controls also need to keep pace with regulatory change. When AUSTRAC extends its AML/CTF regime to accounting and legal firms, businesses that already have structured onboarding processes will adapt far more easily than those running manual, ad hoc workflows. Compliance isn’t a one-time setup; it requires regular reviews, staff updates, and technology that fits your existing operations without creating new friction or requiring your team to learn entirely new platforms.

Why regulatory compliance matters to Australian businesses

Australia’s regulatory environment has grown significantly more demanding over the past decade, and that trend is continuing. Businesses in professional services, financial services, and education now face stricter obligations than ever before, with regulators actively increasing enforcement activity and expanding the scope of who those rules apply to. Understanding the importance of regulatory compliance in this context isn’t abstract; it directly affects your licence to operate and your ability to retain clients who expect professional standards.

A shifting landscape for professional services

The most significant change on the horizon is AUSTRAC’s extension of AML/CTF obligations to accounting firms, lawyers, and other designated non-financial businesses and professions. From 2026, firms that were previously outside the AML/CTF regime will need to implement compliance programmes, conduct customer due diligence, and meet ongoing reporting requirements. This isn’t a distant policy discussion; it’s a firm deadline that your practice needs to prepare for now.

Tax Practitioners Board regulations already require accountants to verify client identities as part of their professional obligations. Firms that haven’t built reliable, repeatable onboarding processes for meeting these requirements are already operating at risk, regardless of whether an AUSTRAC obligation has kicked in yet.

Regulators are watching more closely

Enforcement activity across Australian regulators has increased markedly. AUSTRAC, ASIC, and the TPB have all signalled that they are prioritising compliance oversight, and penalties for failures have grown accordingly. Regulators are also sharing information more readily, which means a gap in one area can trigger scrutiny in another.

The businesses that respond to this environment proactively, rather than reactively, consistently find themselves in a stronger position when regulators come knocking.

Your clients notice too. A firm that handles identity verification and onboarding smoothly signals competence and trustworthiness from the very first interaction.

Benefits of strong compliance

Strong compliance does more than keep regulators satisfied. When you treat the importance of regulatory compliance as a genuine business priority, you unlock practical advantages that directly affect your firm’s stability, reputation, and growth. The firms that build structured compliance programmes consistently outperform those that treat it as an afterthought when questions arise.

Reduced risk and stronger operations

A well-run compliance programme reduces the likelihood of costly mistakes, whether that’s a missed KYC check, a data breach caused by poor information handling, or an onboarding process that lets a high-risk client through without proper due diligence. These aren’t edge cases; they’re the everyday failures that expose firms to fines, investigations, and remediation costs far exceeding what solid compliance infrastructure would have cost to establish in the first place.

Businesses with documented, repeatable compliance processes recover faster when regulations change, because they have a foundation to update rather than a gap to fill from scratch.

Your team benefits too. Clear procedures and automated workflows reduce the cognitive load on staff who would otherwise manage compliance manually, cutting errors and wasted time and freeing capacity for higher-value work.

Client trust and competitive advantage

Clients notice how you handle their information and onboarding experience from the very first interaction. A firm that verifies identities quickly, handles sensitive data securely, and demonstrates clear professional standards signals that it takes its obligations seriously. That builds genuine trust, which is harder to earn and easier to lose than most firms realise.

Compliance also differentiates you from competitors who cut corners. When a prospective client compares two firms, the one with a transparent, professional onboarding process wins that first impression and often the engagement. Over time, that reputation for diligence and reliability becomes a genuine business asset.

Consequences of non-compliance

The importance of regulatory compliance becomes clearest when you look at what happens to businesses that fail to meet their obligations. Australian regulators have become significantly more active in pursuing enforcement, and the consequences they impose range from financial penalties to the permanent loss of your licence to operate.

Financial penalties and enforcement action

AUSTRAC can impose civil penalties of up to $22.2 million for serious AML/CTF breaches, with higher figures applying to corporations under certain provisions. The TPB can suspend or deregister practitioners who fail to meet professional standards, which for an accounting firm means losing the ability to provide tax agent services entirely. Beyond the headline fines, enforcement investigations consume significant management time and legal costs that frequently exceed the penalty itself.

Regulators do not treat first-time failures as automatically minor. If your compliance programme is undocumented or absent, the penalty reflects that.

Criminal prosecution is also on the table for serious AML/CTF failures, not just civil sanctions. That exposure alone is reason enough to treat your compliance obligations as non-negotiable.

Reputational damage and client loss

Regulatory sanctions become public record. AUSTRAC, ASIC, and the TPB all publish enforcement outcomes, which means a penalty does not stay between you and the regulator. Clients searching your firm’s name will find it, and prospective clients conducting due diligence will walk away. In professional services, where referrals and reputation drive growth, that kind of public exposure can shrink your client base faster than any fine.

Your team notices too. Talented people choose firms they trust to operate professionally and ethically. A compliance failure signals poor governance, and that directly affects your ability to retain and attract the staff your firm depends on to deliver quality work.

How to build and run a compliance programme

Understanding the importance of regulatory compliance is one thing; putting a programme in place that actually holds up under scrutiny is another. A compliance programme doesn’t need to be complex, but it does need to be documented, consistent, and regularly reviewed. Start by mapping which regulations apply to your business, then build workflows that make meeting those obligations the default behaviour for your team.

A written record of your obligations and how your firm meets them is your first line of defence if a regulator investigates.

Map your obligations and assign ownership

Your first step is knowing exactly which rules apply to your firm and where your current processes fall short. Compare each regulatory framework that covers your business against what you actually do today, and treat the gaps you find as your priority list for action.

Once you know what needs to change, design clear, repeatable processes for each compliance task and document who is responsible for running each check, how results are recorded, and what happens when something flags a concern. Assigning clear ownership at the individual level prevents tasks from being dropped during busy periods when everyone assumes someone else has covered it.

Review, train, and update regularly

Regulations change, and your programme needs to change with them. Schedule regular reviews of your compliance procedures, at minimum annually, and whenever a significant update occurs. When AUSTRAC extends its AML/CTF regime to accounting and legal firms, businesses with structured programmes will adapt quickly, while those without one will scramble to catch up.

Make sure your team receives practical, role-specific training that covers both why each requirement exists and exactly how to carry it out. A policy document nobody reads does not constitute a compliance programme, and regulators are well aware of the difference between documented intent and genuine practice.

Final takeaways

The importance of regulatory compliance goes well beyond avoiding fines. When you build a programme that’s documented, consistently followed, and supported by the right technology, you protect your firm from enforcement action, strengthen client trust, and create operations that hold up when regulations shift. Businesses that treat compliance as a genuine priority consistently outperform those that wait for a regulator to prompt action.

Your biggest challenge is execution, not awareness. Manual processes and disconnected tools introduce the errors and delays that compliance failures are made of. Getting the foundations right now, before AUSTRAC’s extended AML/CTF obligations fully bite, puts your firm in a far stronger position than scrambling to catch up later.

If you want to see how StackGo makes identity verification and AML/CTF checks work directly inside your existing software, explore how IdentityCheck handles AUSTRAC Tranche 2 compliance or create a free account to test it for yourself.