Every regulated business in Australia has a legal obligation to ensure they’re not doing business with sanctioned individuals, entities, or countries. Getting this wrong doesn’t just mean a fine, it can mean criminal prosecution, reputational damage, and the loss of your licence. Yet many firms still aren’t clear on what the process actually involves. A solid sanctions screening definition is the starting point for understanding your compliance obligations and building workflows that hold up under scrutiny.

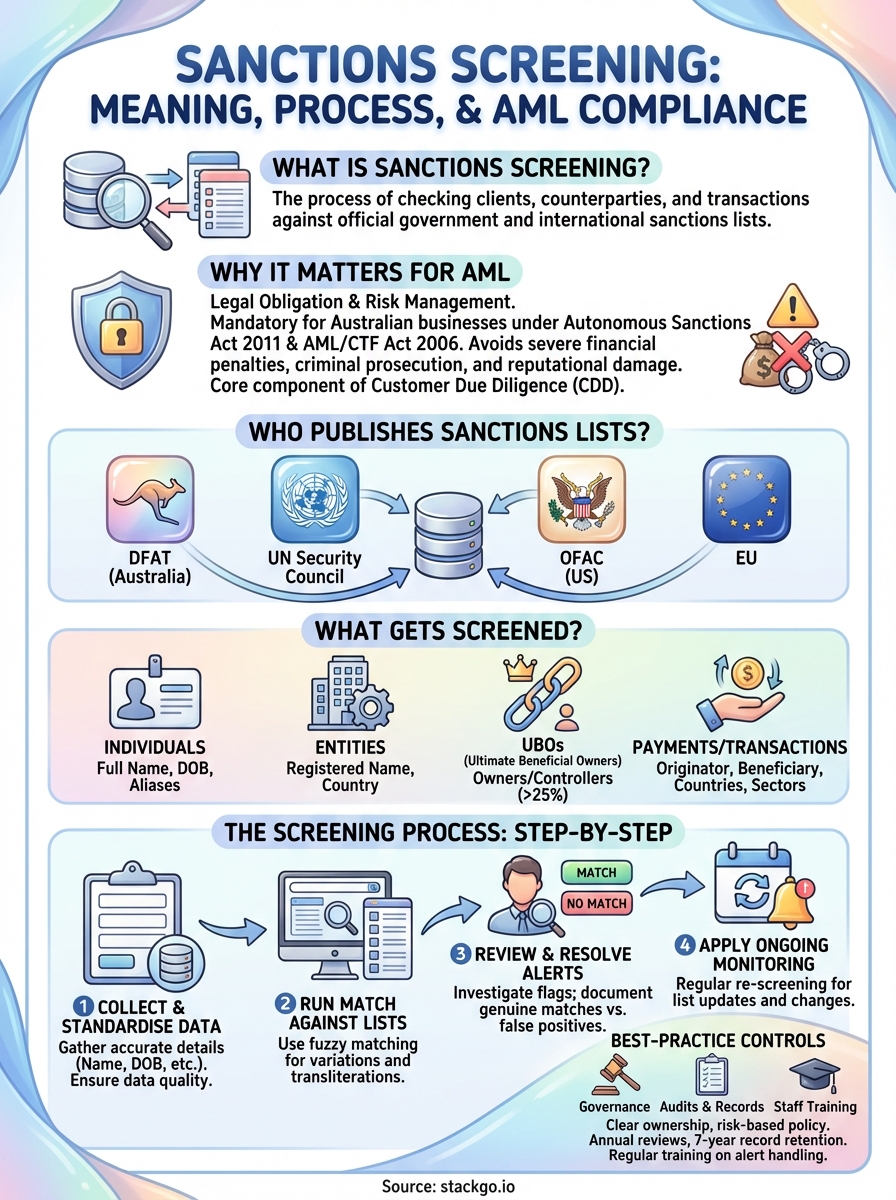

At its core, sanctions screening is the process of checking your clients, counterparties, and transactions against official sanctions lists maintained by bodies like the United Nations, OFAC, the EU, and, critically for Australian businesses, the Department of Foreign Affairs and Trade (DFAT) under the Autonomous Sanctions Act 2011. It sits alongside identity verification and other AML/CTF checks as a non-negotiable part of customer due diligence.

This article breaks down what sanctions screening means, how the process works from start to finish, and why it matters for AML compliance. We’ll also cover the types of sanctions lists you need to know about, common challenges businesses face, and how screening fits into a broader compliance programme. At StackGo, we build integration tools like IdentityCheck that let businesses run KYC and compliance checks directly from their existing CRM, so this is a space we work in every day. Whether you’re an accounting firm preparing for AUSTRAC’s AML/CTF regime or a financial services provider tightening your onboarding process, this guide will give you a clear, practical understanding of sanctions screening and how to approach it.

Why sanctions screening matters for AML and compliance

Sanctions screening sits at the intersection of legal obligation and risk management. For Australian businesses, it is not optional. The Autonomous Sanctions Act 2011 and the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act) together create a compliance landscape where failing to screen clients and transactions can expose your business to serious legal consequences. Understanding the sanctions screening definition is not an academic exercise; it is the foundation of a functioning compliance programme.

The legal obligations driving sanctions compliance

Australian businesses must comply with DFAT’s consolidated sanctions list, which is updated regularly and carries penalties for dealing with listed individuals or entities. Beyond Australian law, many businesses also hold obligations under international frameworks. If you handle cross-border transactions or work with clients who operate internationally, you need to check lists published by bodies such as the UN Security Council, OFAC (the US Office of Foreign Assets Control), and the EU. Ignoring any of these lists is not a valid defence in regulatory proceedings.

The key obligations you are working within include:

- Autonomous Sanctions Act 2011: Prohibits dealings with sanctioned individuals and entities under Australian autonomous sanctions regimes

- AML/CTF Act 2006: Requires designated services to conduct customer due diligence, which includes sanctions checks

- UN Security Council resolutions: Legally binding on Australia, meaning listed entities cannot be dealt with regardless of their location

- AUSTRAC reporting obligations: Suspicious matter reports (SMRs) must be filed where sanctioned parties are identified

How sanctions screening fits into your AML/CTF framework

Sanctions screening is one component of a broader customer due diligence (CDD) process. Alongside identity verification and politically exposed person (PEP) checks, it helps you build a complete picture of who you are dealing with and whether they present a financial crime risk. AML programmes that treat sanctions screening as a separate, standalone task tend to miss connections that only become visible when you examine the full CDD picture together.

Effective AML compliance treats sanctions screening, PEP checks, and identity verification as interconnected controls, not isolated tasks.

Your risk-based approach to AML should also inform how frequently you screen. AUSTRAC guidance makes clear that higher-risk customers require enhanced due diligence, which means more thorough and more frequent screening. A new client in a low-risk sector may require a single check at onboarding. A client with complex ownership structures, international connections, or high transaction volumes needs ongoing, dynamic screening that picks up changes to sanctions lists well after the initial check is complete.

The cost of getting it wrong

The financial penalties for sanctions breaches in Australia are significant. Under the Autonomous Sanctions Regulations, civil penalties can reach hundreds of thousands of dollars per breach, and criminal penalties include imprisonment. The direct financial cost, however, is often less damaging than the reputational fallout. Regulators publish enforcement actions, and being named in one of those notices can undermine client trust and business relationships in ways that take years to recover from.

Non-compliance also carries a significant internal cost. When your team lacks clear, documented screening processes, you end up with inconsistent results, missed matches, and audit findings that require expensive remediation. The firms that attract the least regulatory scrutiny are typically those with systematic, repeatable controls rather than ad hoc checks performed at random points in the client lifecycle. Building that kind of system starts with understanding what sanctions screening is, what it covers, and where it sits within your overall compliance obligations.

What sanctions are and who publishes sanctions lists

Sanctions are legal restrictions imposed by governments or international bodies that prohibit or limit dealings with specific individuals, organisations, countries, or sectors. They are a tool of foreign policy and national security, used to apply pressure without resorting to military action. For your compliance programme, the practical implication is straightforward: if a person, entity, or country appears on a relevant sanctions list, you cannot provide them with services, process their transactions, or facilitate deals on their behalf.

Types of sanctions regimes

Not all sanctions work the same way, and understanding the differences matters when you are designing your screening process. Targeted sanctions (sometimes called smart sanctions) restrict specific named individuals or entities, such as government officials, arms dealers, or terrorist financiers. Sectoral sanctions restrict activities in particular industries, like energy, defence, or finance, within a specific country. Comprehensive country sanctions impose broad restrictions on all dealings with an entire jurisdiction.

Knowing which type of sanctions apply to your client base helps you calibrate the depth of your screening and avoid gaps that a one-size-fits-all approach would miss.

Your exposure to these regimes depends on the nature of your business. An accounting firm handling domestic clients faces a different risk profile than a financial services provider processing cross-border payments, but both carry obligations under Australian law.

Key list publishers you need to know

Several bodies publish the sanctions lists you need to screen against. DFAT maintains Australia’s consolidated sanctions list under the Autonomous Sanctions Act 2011, and it is the primary reference point for Australian businesses. The UN Security Council publishes its own consolidated list covering individuals and entities subject to UN sanctions measures, which are legally binding on all member states including Australia.

For businesses with international exposure, two additional publishers carry significant weight. OFAC (the US Office of Foreign Assets Control) publishes several lists, including the Specially Designated Nationals (SDN) list, which matters if you touch USD transactions or deal with US-connected counterparties. The European Union maintains its own consolidated sanctions list, which is relevant if you operate in or service clients across EU member states.

Each of these bodies updates their lists on different schedules, sometimes multiple times per week, which is why a one-time check at onboarding is rarely sufficient. Applying the full sanctions screening definition in practice means building a process that accounts for all relevant lists and monitors for changes on an ongoing basis.

What gets screened: customers, counterparties, payments, UBOs

The sanctions screening definition only becomes operationally useful when you know exactly what needs to go through the screening process. Most businesses focus on new clients at the point of onboarding, but that narrow view leaves significant gaps. A complete screening programme covers every touchpoint where a sanctioned party could enter your business, whether as a client, a supplier, a payment recipient, or a hidden owner sitting behind a corporate structure.

Individual customers and beneficial owners

When a new individual client engages your services, their details need to run against relevant sanctions lists before you proceed. This includes full legal name, date of birth, and any known aliases. Name matching alone is not enough, because sanctioned individuals often appear under multiple transliterations or variations, particularly when names originate from non-Latin scripts.

Ultimate beneficial owners (UBOs) are where many screening programmes fall short. A UBO is the natural person who ultimately owns or controls a legal entity, typically defined as holding 25% or more of shares or voting rights. If you only screen the entity itself and not the individuals behind it, a sanctioned person can enter your client base through a layered corporate structure. AUSTRAC’s guidance makes clear that your due diligence must look through corporate veils to identify and screen the actual humans in control.

Screening the entity name without identifying and checking the UBOs behind it is one of the most common gaps regulators find during AML audits.

Counterparties and business entities

Beyond your direct clients, third parties involved in transactions or business arrangements also require screening. Suppliers, intermediaries, joint venture partners, and referral sources all represent potential exposure points. When you facilitate a deal or process a payment on behalf of a client, the other side of that transaction carries risk that lands on you if you have not checked them.

Business entities require screening against sanctions lists that target organisations directly, not just the individuals associated with them. Some regimes, such as OFAC’s SDN list, include both individuals and companies, so your process needs to handle both entity types without treating them identically.

Payments and transactions

Individual payment instructions can also carry sanctions risk, particularly in financial services and accounting. The originator, beneficiary, and any intermediary banks involved in a cross-border payment all need checking. Payments referencing sanctioned countries, currencies, or sectors require additional scrutiny even when no named individual appears on a list.

How sanctions screening works step by step

Understanding the sanctions screening definition at a conceptual level is useful, but knowing how the process actually runs helps you identify where your current workflow has gaps. The core process follows a consistent set of steps regardless of whether you screen manually or use an automated tool, and each step needs to be completed reliably every time to satisfy your compliance obligations.

Step 1: Collect and standardise data

Before any screening takes place, you need to gather accurate data about the person or entity you are checking. For individuals, this means full legal name, date of birth, nationality, and any known aliases. For entities, you need the registered legal name, country of incorporation, and the identities of UBOs. Poor data quality at this stage produces unreliable results downstream, so standardising how you collect and store client information before screening begins is not a step you can skip.

Step 2: Run the match against relevant lists

With clean data in hand, you run the details against all sanctions lists relevant to your risk profile, including DFAT’s consolidated list, the UN Security Council list, and any others your obligations require. Screening tools compare your input against list entries using fuzzy matching algorithms that account for spelling variations, transliterations, and partial name matches. This is why manually searching a list document and calling it a check is not sufficient for a regulated business.

The match logic your system uses determines the quality of your results, so understanding how your tool handles name variations is critical to running a defensible screening process.

Step 3: Review and resolve alerts

Every potential match generates an alert that requires human review. Your compliance team assesses whether the flagged result is a genuine match or a false positive by comparing additional identifying details such as date of birth, nationality, and address. You document the outcome either way, because keeping a clear audit trail of every alert and the decision made is what protects you during a regulatory review or external audit.

Step 4: Apply ongoing monitoring

A single check at onboarding does not satisfy your obligations. Sanctions lists update frequently, sometimes multiple times per week, and a client who was clear at onboarding can appear on a list months later. Ongoing monitoring means re-screening your existing client base against updated lists on a scheduled and triggered basis, particularly when your risk assessment identifies a client as higher risk. Running this process systematically keeps your screening programme current without requiring a manual review from scratch each time a list changes.

Common challenges and how teams reduce false positives

Applying the sanctions screening definition in practice is harder than the theory suggests. The gap between running a check and running a reliable, defensible check is where most compliance programmes run into real trouble. Understanding the common failure points helps you design a process that produces results your team can act on without drowning in unworkable noise.

The false positive problem

False positives are the most persistent challenge in any sanctions screening process. They occur when your screening tool flags a name that resembles a listed entry but belongs to a completely different person. A client named "Mohammed Al-Hassan" may trigger matches against several listed individuals with similar names, and each alert requires manual investigation and documented resolution, which adds time and cost to every check.

The volume of false positives your process generates is directly tied to the quality of your matching logic and the completeness of your client data.

Teams reduce false positives by improving data quality at the point of collection. When you capture full legal names, dates of birth, nationalities, and addresses consistently across your client base, your matching logic has more data points to work with and can rule out non-matches faster. Partial data forces the system to cast a wider net, which produces more noise and slows your team down.

Keeping up with list updates

Sanctions lists change constantly. DFAT, the UN Security Council, and OFAC all update their lists on irregular schedules, sometimes multiple times in a single week. Businesses that run screening only at onboarding will miss additions that occur after that initial check. Teams that manage this well schedule automated re-screening at regular intervals and configure alerts when a list update occurs, so no changes slip through unnoticed between review cycles.

Handling name transliteration and aliases

Many sanctioned individuals appear on lists under multiple name variants due to transliteration differences across languages and scripts. A name rendered from Arabic, Russian, or Chinese characters into English can produce several plausible spellings, each of which may or may not match your client’s recorded name. Your screening tool needs fuzzy matching capability that accounts for these variations rather than relying on exact string comparisons.

Building your team’s ability to recognise transliteration patterns and alias structures when reviewing alerts reduces the risk of both missed matches and unnecessary escalations on clear non-matches. Pairing capable tooling with informed human review is what separates a screening process that holds up under scrutiny from one that creates more compliance risk than it removes.

Best-practice controls: governance, audits, training

Running a defensible sanctions screening programme requires more than the right tool. The sanctions screening definition extends into how your organisation governs the process, tests it over time, and equips the people responsible for making decisions on alerts. Weak controls in any of these areas create gaps that regulators identify quickly.

Governance and ownership

Your sanctions compliance programme needs a clearly assigned owner, whether that is a compliance officer, practice manager, or a designated responsible individual at the partner level. Without clear ownership, decisions get deferred, documentation falls behind, and your process drifts from its intended design. Policies and procedures should be written down, approved at a senior level, and reviewed at least annually or whenever a relevant regulatory change occurs.

Good governance also means setting a risk-based screening policy that documents which lists you screen against, how frequently you re-screen existing clients, and what thresholds trigger enhanced due diligence. Regulators do not expect perfection, but they do expect you to show that deliberate, documented decisions drove your approach.

A written policy that your team follows consistently is more valuable to a regulator than a sophisticated tool that no one uses correctly.

Regular audits and record-keeping

Audits give you the evidence that your controls are working. You should review your screening process at least annually, checking whether all new clients were screened at onboarding, whether ongoing monitoring ran on schedule, and whether alerts were resolved and documented within an acceptable timeframe. Any gaps you find are better addressed internally before an external reviewer identifies them.

Record-keeping is non-negotiable. Every check you run, every alert your system generates, and every decision your team makes needs to be stored in a way that you can retrieve and present during an audit or regulatory review. Retaining records for a minimum of seven years aligns with AUSTRAC’s general record-keeping requirements and gives you a defensible paper trail.

Staff training

Your team’s ability to recognise a genuine match and act on it appropriately is what makes the rest of your process work. Annual training should cover how to interpret screening alerts, what a false positive looks like versus a genuine concern, and when to escalate to a senior compliance decision-maker. Training records should be kept alongside your other compliance documentation.

New staff need to complete sanctions training before they handle any client onboarding or transaction processing. A well-trained team reduces both missed matches and unnecessary escalations, which improves the efficiency of your entire compliance workflow.

How to implement sanctions screening in your workflow

Putting the sanctions screening definition into practice means making screening a structured, repeatable part of how your business operates rather than an ad hoc task handled differently each time a new client walks through the door. The implementation steps below apply whether you are an accounting firm preparing for AUSTRAC’s expanded AML/CTF regime or a financial services business tightening an existing programme.

Start with your risk assessment

Your risk assessment determines the scope and depth of your screening programme. Before you choose a tool or write a procedure, map out the types of clients you work with, the jurisdictions they connect to, and the transaction types you process. High-risk client segments and those with international exposure require more thorough and more frequent screening than a purely domestic, lower-risk base. Your risk assessment also tells you which sanctions lists are relevant to your business, so you are not screening against every list in existence but against the ones your regulatory obligations and client profile actually require.

Document your risk assessment formally and review it whenever your client base or service offering changes significantly.

Choose your screening tool and data sources

Manual screening against PDF lists is not a defensible approach for a regulated business. You need a tool that connects to updated list feeds automatically, applies fuzzy matching logic across name variants and aliases, and generates an auditable record of every check and outcome. Evaluating tools against your actual client data before committing gives you a realistic picture of false positive rates and match quality rather than relying on vendor claims alone.

Whichever tool you select, confirm that it covers DFAT’s consolidated list, the UN Security Council list, and any additional lists your risk profile requires. A tool that misses a relevant list source creates a compliance gap that you own, not the vendor.

Embed screening into your onboarding and ongoing review process

Screening needs to happen at two defined points: before you onboard a new client, and on an ongoing basis throughout the relationship. Build the onboarding check into your client intake form so that no new engagement can proceed without a completed, documented screen. For ongoing monitoring, configure your tool to re-screen your client base on a scheduled cycle and to flag alerts whenever the relevant lists update.

Connecting your screening tool directly to your existing CRM or practice management software removes the manual step of moving between systems and reduces the risk of checks being skipped during busy periods. StackGo’s IdentityCheck integration does exactly this, running KYC and compliance checks from within your CRM so the process becomes part of your normal workflow rather than a separate task your team has to remember.

Next steps

The sanctions screening definition covers more ground than most businesses initially expect. It is not a single check at onboarding but a systematic, ongoing process that spans client identity, beneficial ownership, counterparty verification, and transaction monitoring. Getting it right means combining a clear risk assessment, the correct list sources, capable tooling, and trained staff who know what to do when an alert lands in front of them.

Your obligations under AUSTRAC’s AML/CTF framework are not going to get lighter, particularly as Tranche 2 brings accounting and professional services firms into scope. The firms that handle the transition smoothly are already building repeatable processes rather than scrambling when the deadline arrives.

If you want to see how embedded identity verification and sanctions screening can run directly from your existing CRM without adding another standalone tool to your stack, explore how IdentityCheck supports AUSTRAC Tranche 2 compliance.