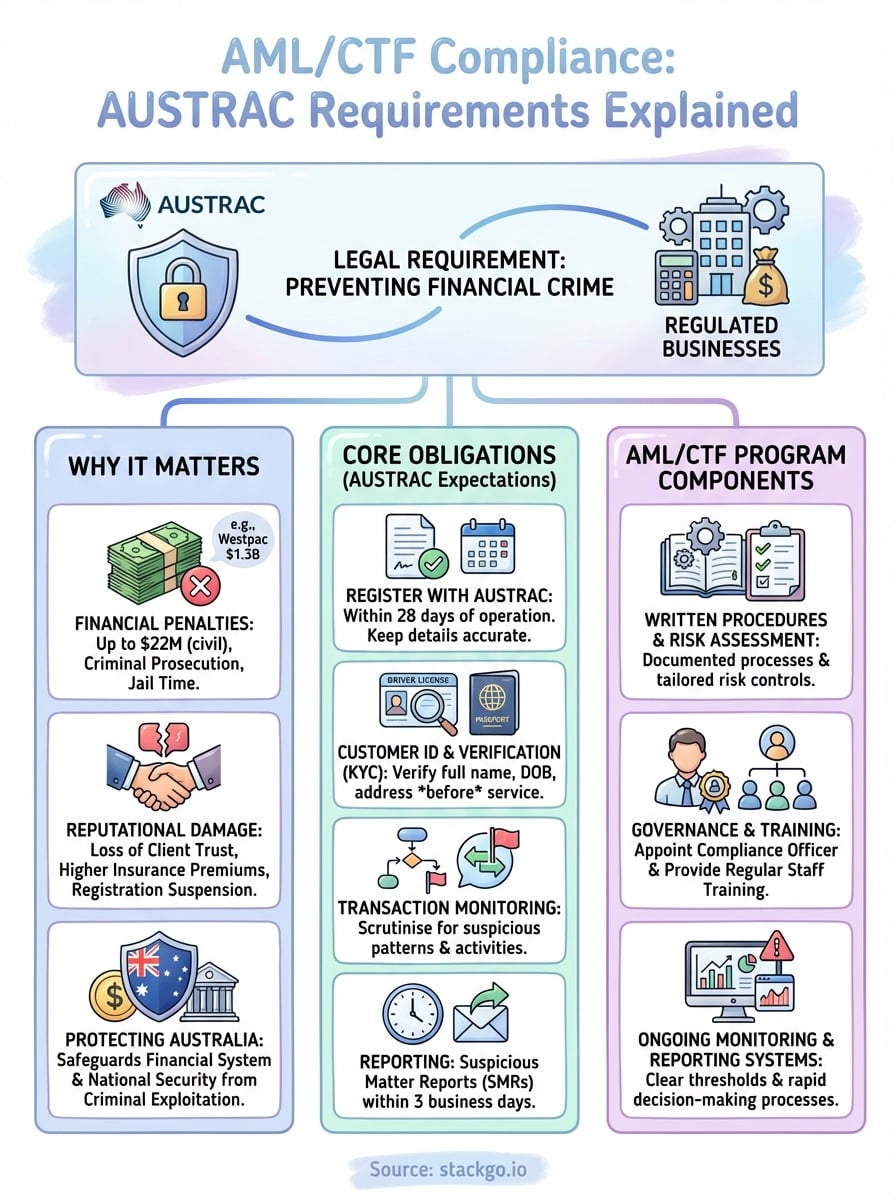

If your business handles financial transactions or provides certain professional services in Australia, AML/CTF compliance isn’t optional, it’s a legal requirement. AUSTRAC, Australia’s financial intelligence agency, enforces strict rules designed to prevent criminals from using legitimate businesses to launder money or fund terrorism. For accounting firms preparing for upcoming regulatory changes, understanding these obligations is now a matter of urgency.

This article breaks down what AML/CTF compliance actually means, who it applies to, and the specific components AUSTRAC requires in a compliant program. You’ll learn about customer due diligence, ongoing transaction monitoring, reporting obligations, and the penalties for getting it wrong. Whether you’re new to these requirements or need a refresher before expanded regulations take effect, this guide covers the essentials you need to know.

At StackGo, we help regulated businesses streamline their identity verification and KYC processes directly within their existing software. Compliance doesn’t have to mean adopting clunky new systems or drowning in manual checks. But before we get to implementation, let’s start with the fundamentals: what AML/CTF compliance requires and why it matters for your business.

Why AML/CTF compliance matters in Australia

The financial and reputational consequences of non-compliance with AML/CTF regulations in Australia are severe enough to put businesses out of operation. AUSTRAC has the authority to impose civil penalties of up to $22 million per breach for corporations, and directors can face criminal prosecution with potential jail time. These aren’t theoretical risks: in 2020, Westpac paid a record $1.3 billion penalty for more than 23 million breaches of AML/CTF laws. Your business might not operate at that scale, but the same legal framework applies regardless of size.

Financial penalties and enforcement actions

AUSTRAC actively pursues non-compliant businesses through a tiered enforcement approach. The regulator can issue infringement notices for less serious violations, commence civil penalty proceedings for systemic failures, or refer cases for criminal prosecution when deliberate breaches occur. Recent years have seen increased enforcement activity, with penalties issued across industries from financial services to remittance providers. Your compliance isn’t just about avoiding fines; AUSTRAC can also suspend or revoke your business registration, effectively shutting down operations until you demonstrate compliance.

Understanding what is aml ctf compliance means recognising that regulatory oversight extends beyond major banks to any business handling financial transactions or providing designated services.

Reputational damage and client trust

Beyond regulatory penalties, non-compliance destroys the client relationships that professional services firms depend on. When AUSTRAC publishes enforcement actions on its website, your business name becomes permanently associated with compliance failures. Prospective clients conduct due diligence before engaging service providers, and a history of AML/CTF breaches signals unreliability and potential risk. For accounting firms entering this regulatory space, your existing clients expect you to handle their financial information with the same rigour you apply to tax compliance.

Professional indemnity insurers also scrutinise your compliance framework. Firms without adequate AML/CTF controls may face higher premiums or coverage exclusions, particularly for claims related to financial crime facilitation. This creates a compounding cost that extends far beyond initial regulatory penalties.

Protecting Australia’s financial system

Your compliance program serves a purpose beyond your business interests. Money laundering and terrorism financing undermine economic stability and national security, with criminals exploiting weaknesses in legitimate businesses to move illicit funds. When you implement effective AML/CTF controls, you create barriers that make Australia a harder target for financial crime. The regulated sectors collectively form a defence network that protects both the financial system and the broader community from exploitation.

Professional service providers occupy a particularly vulnerable position because criminals actively seek gatekeepers who can provide legitimacy to suspicious transactions. Lawyers, accountants, and real estate agents all handle activities that criminals need to integrate illegal funds into the legitimate economy. Your vigilance directly impacts whether your business becomes an unwitting facilitator of crime.

What AUSTRAC expects from reporting entities

AUSTRAC designates specific businesses as reporting entities under the AML/CTF Act, which means you must comply with a structured framework of obligations if your business operates in one of the regulated sectors. The definition captures financial institutions, remittance providers, gambling services, and bullion dealers as core categories. From 2026, accountants providing certain services will also fall under this definition, marking a significant expansion of the regulatory scope. Your obligations begin the moment you start providing designated services, not when you feel ready to comply.

Registration and ongoing obligations

You must register your business with AUSTRAC within 28 days of commencing operations as a reporting entity. This registration isn’t a one-time formality; AUSTRAC requires you to maintain accurate business details and notify them of any changes to your structure, ownership, or services. Your registration creates a permanent record that AUSTRAC uses to track your compliance performance and target its supervisory activities. Failing to register or update your details triggers immediate penalties before you even begin operating.

What is aml ctf compliance if not a commitment to transparent operation within a framework that AUSTRAC actively monitors and enforces?

Customer identification and verification

AUSTRAC expects you to verify every customer’s identity before providing designated services, using reliable and independent documentation. You cannot accept a client relationship based on verbal assurances or partial information. The verification standard requires you to collect full legal names, dates of birth, and residential addresses, supported by original documents or certified copies. For corporate clients, you must identify beneficial owners who ultimately control the entity. Your verification records must demonstrate that you completed these checks before the business relationship commenced, not retrospectively when AUSTRAC asks questions.

Transaction monitoring forms another core expectation. AUSTRAC requires you to scrutinise customer transactions for patterns that indicate potential money laundering or terrorism financing activity.

What an AML/CTF program includes

Your AML/CTF program must exist as a written document that details how your business identifies, manages, and mitigates money laundering and terrorism financing risks. This isn’t a theoretical exercise; AUSTRAC requires you to create specific procedures that your staff can follow when handling customer relationships and transactions. The program forms the operational backbone of your compliance framework, and you must review it regularly to ensure it remains effective as your business evolves and threats change.

Written procedures and risk assessment

You must document clear identification and verification procedures that explain exactly how your staff will check customer identities before establishing business relationships. Your written program needs to specify what documents you accept, how you verify them, and when enhanced due diligence becomes necessary for higher-risk customers. AUSTRAC expects you to conduct a risk assessment that evaluates how criminals might exploit your particular business model, then design controls that address those specific vulnerabilities. Generic templates don’t satisfy this requirement; your program must reflect your actual operations.

Understanding what is aml ctf compliance means recognising that your written program serves as evidence that you’ve systematically considered financial crime risks and implemented proportionate controls.

Ongoing monitoring and reporting systems

Your program must establish transaction monitoring processes that enable you to detect suspicious patterns in customer activity. You need documented thresholds for what triggers a review, who conducts the assessment, and how quickly you escalate concerns. AUSTRAC requires you to submit suspicious matter reports within three business days of forming a suspicion, which means your procedures must facilitate rapid decision-making. Your program should also specify record-keeping standards, including what information you retain and for how long.

Governance and training requirements

You must appoint a compliance officer with authority to manage your AML/CTF program and direct access to senior management. Your written program needs to detail this person’s responsibilities and reporting lines. AUSTRAC expects you to provide regular staff training so employees understand their obligations and can recognise potential financial crime indicators. Your program should specify training frequency, content, and how you assess whether staff have absorbed the material.

How to implement AML/CTF compliance

Implementation begins with understanding your specific obligations under the AML/CTF Act based on the designated services your business provides. You cannot copy another firm’s program and expect it to work; your compliance framework must address the unique risks your business faces and the particular ways criminals might exploit your operations. Start by reviewing AUSTRAC’s guidance materials for your sector, then conduct an internal assessment of your current processes to identify gaps between what you do now and what the regulations require.

Conducting your risk assessment

You must complete a formal risk assessment that examines how money launderers or terrorism financiers could use your services. This assessment drives every other decision in your compliance program. Look at your customer base, the services you offer, your geographic reach, and the transaction types you handle. Document specific vulnerabilities you identify, such as cash-intensive services, clients in high-risk jurisdictions, or complex corporate structures that obscure beneficial ownership. Your risk assessment determines whether standard customer due diligence suffices or whether certain relationships require enhanced scrutiny.

Building operational procedures

Create documented procedures for each compliance obligation, starting with customer identification and verification. Your procedures must specify what documents you accept, how staff verify authenticity, when they need to collect additional information, and where they record the results. Implement transaction monitoring systems that flag suspicious patterns based on your risk assessment findings. These systems can range from simple spreadsheet tracking for small operations to automated software for higher volumes.

What is aml ctf compliance without practical procedures that your team can actually follow when they encounter real customer situations?

Training your team

Your staff cannot comply with obligations they don’t understand. Deliver initial training that covers money laundering and terrorism financing indicators, verification requirements, and reporting procedures. Schedule regular refresher sessions to reinforce expectations and update staff on new threats or regulatory changes.

Common pitfalls and key questions

Businesses regularly stumble over the same compliance mistakes, often because they underestimate the operational changes AML/CTF obligations demand. You might assume that verifying customer identities involves a simple document check, but AUSTRAC expects ongoing vigilance throughout the customer relationship. Many firms rush to tick boxes without understanding why each requirement exists, creating programs that look compliant on paper but fail in practice when tested by suspicious activity or an AUSTRAC audit.

Underestimating resource requirements

You cannot bolt AML/CTF compliance onto existing workloads without dedicating adequate time and budget. Firms commonly assign compliance responsibilities to staff already overwhelmed with client work, then wonder why verification procedures get skipped or reports get filed late. Your compliance officer needs sufficient authority and resources to implement the program effectively. Training alone requires recurring investment, not a one-off session when you launch your program.

Failing to update your program

Your AML/CTF program requires regular reviews to remain effective as threats evolve and your business changes. Businesses often create initial documentation then leave it gathering dust for years. AUSTRAC expects you to reassess risks periodically and adjust procedures when you introduce new services, enter new markets, or observe emerging financial crime patterns.

What is aml ctf compliance if not a dynamic framework that adapts to changing threats rather than a static document you file and forget?

Questions to ask yourself

Before launching your program, consider whether you understand who holds ultimate responsibility for compliance failures in your organisation. Can your staff explain when they need to conduct enhanced due diligence? Do you have systems that actually work for monitoring customer transactions, or are you relying on manual reviews that inevitably miss suspicious patterns? Have you tested your suspicious matter reporting process to confirm staff can escalate concerns quickly enough to meet the three-day deadline?

Next steps

Understanding what is aml ctf compliance represents your first step toward meeting AUSTRAC’s requirements, but knowledge alone won’t protect your business from penalties or reputational damage. You must translate these obligations into operational procedures that work within your existing workflow, ideally before the expanded regulations take effect in 2026.

Your compliance program needs verification systems that integrate seamlessly with the software you already use. StackGo’s IdentityCheck removes the friction from customer due diligence by running AUSTRAC Tranche 2 identity verification directly inside your CRM, eliminating the need to adopt new platforms or manage manual document checks. Your team verifies clients without switching tabs or learning complex new software.

Start by reviewing your current customer onboarding process against AUSTRAC’s requirements. Identify where manual steps create bottlenecks or compliance gaps, then explore how integrated solutions can strengthen your controls while reducing operational burden.