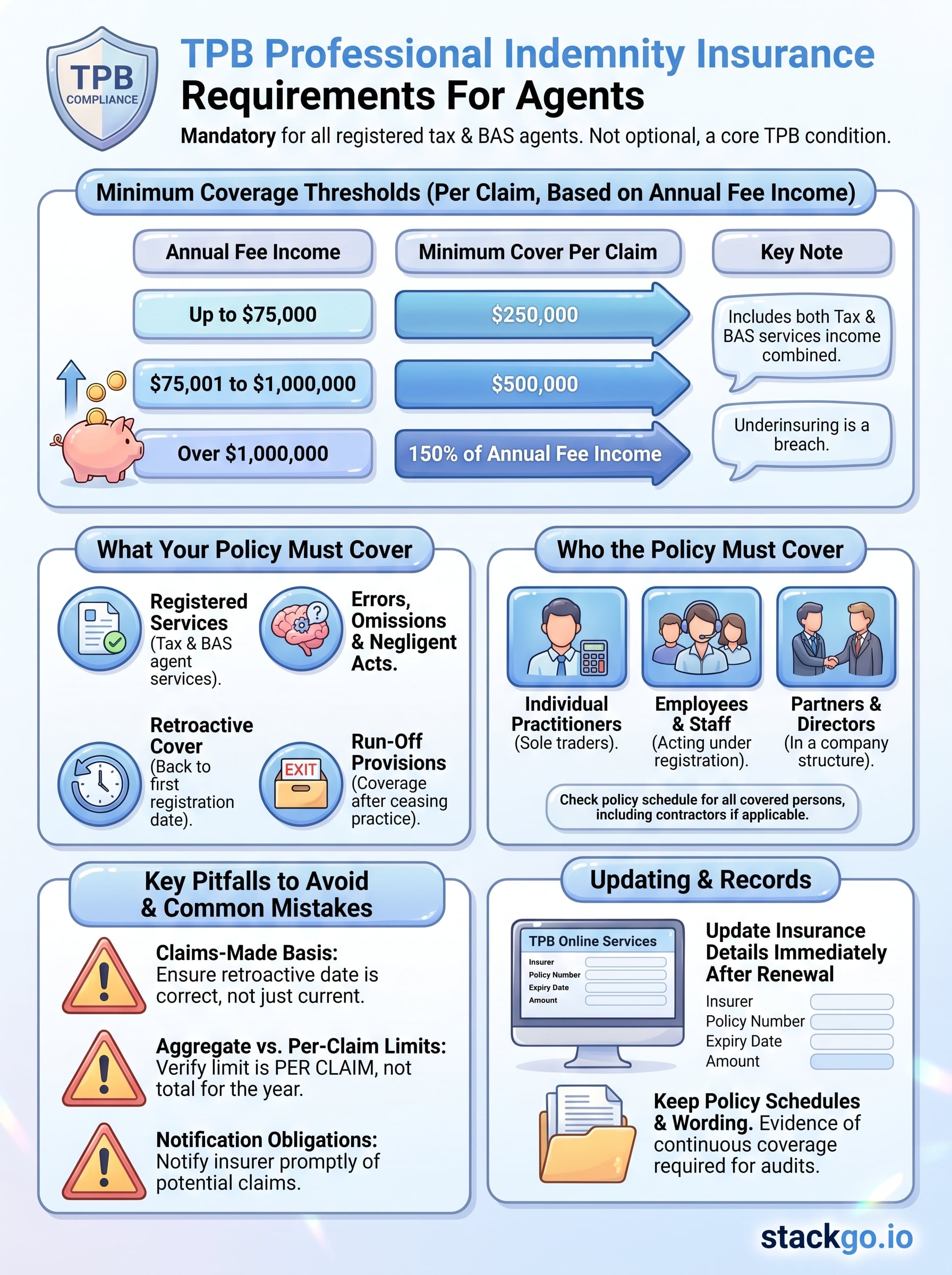

Every registered tax agent and BAS agent in Australia must hold adequate TPB professional indemnity insurance to maintain their registration. It’s not optional, it’s a core condition set by the Tax Practitioners Board, and failing to meet it can result in sanctions, suspension, or termination of your registration. Yet despite these stakes, the specific requirements around coverage levels, policy types, and reporting obligations remain a common source of confusion for practitioners.

This article breaks down exactly what the TPB requires from your professional indemnity insurance policy, including minimum coverage thresholds, what your policy must actually cover, how to assess whether your current insurer meets the TPB’s standards, and the process for updating your insurance details with the Board. Whether you’re applying for registration for the first time or renewing an existing one, you’ll find the practical detail you need here.

At StackGo, we build integration tools, like IdentityCheck, that help accounting and professional services firms run compliance workflows directly from their existing software. While PII is something you’ll arrange with an insurer, identity verification and client onboarding are areas where we see firms lose significant time to manual processes. Understanding your full compliance picture, from insurance through to KYC obligations, is what keeps a practice running cleanly, and that’s the space we operate in.

Why TPB PI insurance matters

PI insurance sits at the heart of how the TPB ensures the public is protected when they rely on a registered practitioner. When a tax or BAS agent makes an error, whether it’s a miscalculation, missed deadline, or incorrect advice, the financial consequences can fall heavily on the client. The Tax Practitioners Board requires PI insurance precisely so that compensation is available when something goes wrong, not just for your clients’ protection, but for yours as well.

The regulatory basis for the requirement

The requirement for TPB professional indemnity insurance flows directly from the Tax Agent Services Act 2009 (TASA) and the Tax Agent Services Regulations 2022. Under these instruments, adequate PI insurance is a condition of registration that all registered tax agents and BAS agents must satisfy on an ongoing basis, not just at the point of initial application. The TPB’s practice note TPB(PN) 5/2022 sets out the Board’s expectations in detail, including what "adequate" actually means in practice.

Importantly, the Regulations give the TPB the authority to assess whether a policy meets the required standard, and the Board has been clear that it will act where practitioners fall short. Failing to hold compliant insurance at any point during your registration is treated as a breach of a registration condition, which triggers the TPB’s compliance and investigation processes.

If your PI policy lapses even briefly between renewals, you are technically in breach of your registration conditions for that period.

What you and your clients are protected against

PI insurance covers claims arising from professional negligence, errors, and omissions that occur in the course of your work as a registered practitioner. For a tax agent, that might mean a client suffers a financial loss because of incorrect advice on a capital gains event, or because a return was filed late and penalties accrued. For a BAS agent, it could mean an activity statement was prepared using figures that did not match the client’s records, resulting in an underpayment or overpayment obligation.

Your clients gain a financial remedy when something goes wrong, and you get a funded defence if a claim is made against you. Without an adequate policy, you would bear the full cost of legal defence and any compensation awarded, which in a complex tax dispute can be substantial and business-ending. This is why the TPB treats coverage as non-negotiable rather than an optional best-practice measure.

What TPB PI insurance does not cover

Worth being clear about what PI insurance is not. It does not cover criminal conduct, deliberate dishonesty, or fraud. It is not the same as general business liability insurance, and it does not automatically extend to every person working within your practice unless your policy is explicitly structured to include them. Many agents run into problems because they assume their existing business insurance policy already satisfies the TPB requirement, only to find at renewal or during a TPB review that the policy terms do not align with what the Board requires.

Understanding the actual limits of your coverage is just as important as holding a policy in the first place. A policy that exists on paper but excludes key activities, specific service types, or certain staff members may leave you exposed in exactly the scenario you assumed you were protected against. The TPB assesses whether your policy genuinely satisfies its conditions, not simply whether you hold some form of insurance.

Who must hold PI insurance and who may not

The obligation to hold TPB professional indemnity insurance applies broadly, but it is not identical for every registration type. Understanding exactly where you sit in the framework saves you from either leaving yourself exposed or over-engineering your coverage for a situation that does not require it.

Practitioners who must hold PI cover

All registered tax agents and BAS agents are required to hold adequate PI insurance as an ongoing condition of their registration. This applies whether you operate as a sole trader, a partnership, or a company. If your registration is active, your insurance obligation is active. There is no threshold of client numbers or revenue below which the requirement disappears.

If you operate through a company or trust structure, the registered entity itself must hold the policy, not just the individual practitioners working within it. Individual tax agents employed by a registered company are generally covered under that company’s policy, but only if the policy is structured to include them. You should not assume that your employer’s policy covers you personally in all circumstances. Checking the policy schedule and confirming coverage with your insurer directly is the cleaner approach.

Sole traders in particular often underestimate their exposure, because they carry the entire professional and financial risk personally without a corporate structure to separate it.

When the requirement may not apply

The Tax Agent Services Regulations 2022 do make provision for certain limited exemptions, primarily where a registered agent is employed and covered under the employer’s policy, or where the TPB has granted a specific waiver. However, these are narrow carve-outs and should not be treated as a default assumption. The TPB’s guidance is clear that the burden sits with the individual registrant to confirm their coverage status, not with the Board to confirm an exemption.

New applicants applying for registration must have PI insurance in place before registration is granted. The policy needs to be current at the date of application, and you will need to provide policy details as part of the application process. Waiting until after registration is approved is not a viable approach. Similarly, if your registration lapses and you later seek to renew it, you will need to demonstrate that you have current, compliant coverage in place before the TPB will reinstate your registration.

Some practitioners operating purely in an employed capacity and providing services only through their employer’s registered practice may have a different position, but this depends entirely on the specific policy terms your employer holds. Verify before you assume.

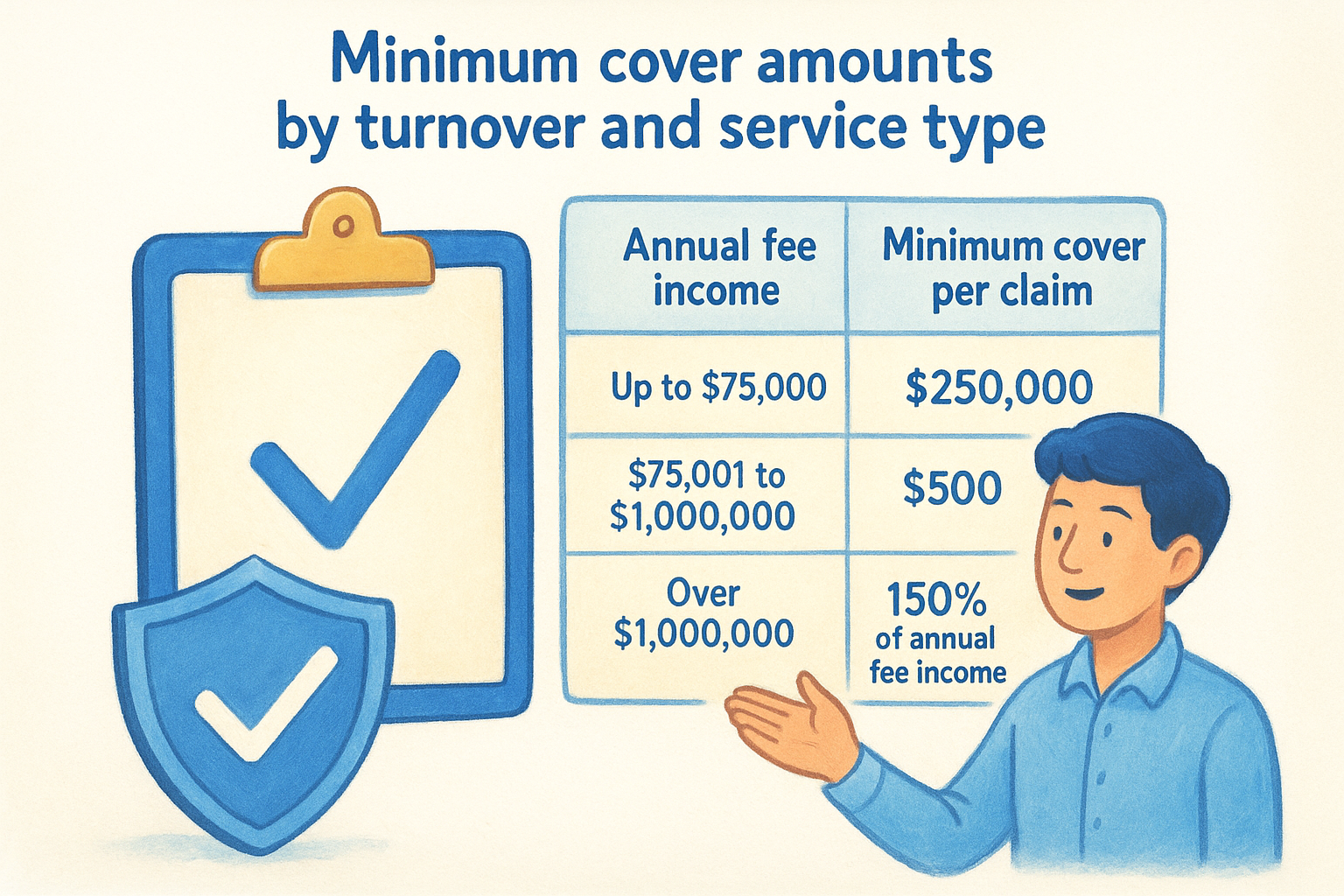

Minimum cover amounts by turnover and service type

The TPB does not leave the question of coverage level open to interpretation. The Tax Agent Services Regulations 2022 specify minimum amounts of cover that registered practitioners must hold, and those minimums are tied directly to your annual fee income from tax agent or BAS agent services. Getting the figure right matters because underinsuring is treated as non-compliance, even if you hold a policy that is otherwise structured correctly.

How turnover determines your minimum cover

Your annual fee income from providing registered tax agent or BAS agent services determines which minimum coverage tier applies to you. The Regulations set out a sliding scale, so as your practice grows, your minimum required cover increases alongside it.

The table below summarises the thresholds as set out in the Regulations:

| Annual fee income | Minimum cover per claim |

|---|---|

| Up to $75,000 | $250,000 |

| $75,001 to $1,000,000 | $500,000 |

| Over $1,000,000 | 150% of annual fee income |

For most sole traders and small practices, the $250,000 or $500,000 tiers will apply. However, if your practice has grown significantly, you may now fall into the third tier without having reviewed your policy limits in recent years. Many insurers renew policies on standard settings unless you actively update them, so it is worth confirming your current fee income and checking whether your existing policy still meets the applicable minimum.

Review your annual fee income figure at every renewal, not just when you expect it to have changed significantly.

Service type and how it affects your calculation

When you hold both a tax agent and a BAS agent registration, the fee income from both streams counts toward your total for the purposes of calculating which coverage tier applies. You cannot separate the two to stay within a lower threshold. The TPB assesses your total registered services income as a combined figure.

Where your practice provides additional professional services, such as financial advice, bookkeeping outside the BAS agent scope, or accounting work that does not fall under the Tax Agent Services Act 2009, those earnings may not count toward your TPB-regulated fee income. However, those same activities may still generate professional liability claims, which is why many practitioners elect to hold a policy that extends beyond the tpb professional indemnity insurance minimum to cover their full range of services. Confirm the scope with your insurer so there are no gaps between what the TPB requires and what your practice actually does.

What your policy must cover

Holding a policy that meets the minimum coverage amount is only part of the TPB’s requirement. The Board also has specific expectations about what your policy must actually cover in terms of activities, circumstances, and claim types. A policy that covers the right dollar amount but excludes key services you provide is not compliant, even if it looks adequate on the surface.

Activities and services your policy must include

Your policy must cover all registered tax agent or BAS agent services that you provide. That means the policy scope needs to align with the actual work you do for clients, including any services that sit at the edge of those categories. If you prepare income tax returns, provide tax advice, lodge BAS statements, or advise clients on their obligations to the ATO, all of those activities need to sit within your policy’s covered scope.

The TPB expects your policy to cover:

- Tax agent services as defined under the Tax Agent Services Act 2009

- BAS services if you hold a BAS agent registration

- Claims arising from errors, omissions, and negligent acts in the course of providing those services

- Legal defence costs associated with a covered claim

If you have expanded the range of services your practice offers since you last reviewed your policy, check that the new services fall within your current policy’s scope before your next renewal.

Retroactive cover and run-off provisions

Retroactive cover is a requirement that many practitioners overlook. Because PI insurance typically operates on a claims-made basis rather than an occurrence basis, your policy needs to include cover for claims arising from work performed before the current policy period, as long as the claim is made during the current period. The TPB requires that your policy provides retroactive cover back to the date you were first registered, or to the date you first provided the relevant services, whichever is earlier.

Run-off cover becomes relevant when you retire, close your practice, or otherwise stop providing registered services. Even after you cease active practice, claims can still arise from work you completed previously. The TPB’s guidance on tpb professional indemnity insurance makes clear that you need to hold adequate run-off cover for a period after ceasing to practise, to ensure that any claims that emerge in the tail period are still covered. Confirm the specific run-off period your insurer provides and compare it against the TPB’s requirements before you let a policy lapse or cancel it upon retirement.

Who the policy must cover

The coverage scope of your policy is not just about what activities it includes, it also matters who is covered when a claim arises. The TPB requires that your tpb professional indemnity insurance policy extends to all individuals who provide registered services under your registration, not just the principal or the entity holding the registration. If your policy only names one person but several practitioners work under your registration, you likely have a coverage gap that puts both your clients and your registration at risk.

Individual practitioners and employees

Your policy must cover all registered individuals who provide tax agent or BAS agent services on behalf of your practice. That includes employees who prepare returns, lodge statements, or provide tax advice to clients in your practice’s name. It is not sufficient for those employees to hold separate personal policies if your practice is the registered entity providing the service. The registered practice’s policy is the one the TPB assesses for compliance, and it must extend to every person acting within the scope of your registration.

Where you employ junior practitioners or support staff who operate under direct supervision, you should still confirm with your insurer that those individuals fall within the policy’s definition of covered persons. Insurers word these definitions differently, and a policy that covers "the insured" without clearly extending to employees may leave gaps you have not anticipated.

Confirm the definition of covered persons in your policy schedule with your insurer, not just the certificate of currency, before you assume all staff are included.

Partners and directors in a registered entity

If your practice operates as a partnership or company, the policy must cover each partner or director who provides registered services. A policy issued in the company name does not automatically extend to individual directors or partners acting in a personal capacity, so the policy wording needs to address this directly. Your insurer should be able to confirm whether each person in a principal role falls within the scope of the policy.

Contractors and consultants

Practitioners who engage contractors to deliver registered services face an additional question: does your policy cover them, or do they need their own? The answer depends on how the services are structured and whether your practice holds out those contractors as providing services under your registration. Some policies explicitly exclude contractors, which means either your contractors need separate cover, or you need to negotiate an endorsement that brings them within your policy’s scope. Resolve this before a claim arises, not after.

Policy settings that often trip agents up

Most PI policy failures do not come from an agent holding no insurance at all. They come from agents holding policies with specific settings that, on closer inspection, do not satisfy TPB requirements. These are the configurations that tend to catch practitioners off guard, often because they were not explained clearly at the time of purchase or have drifted out of alignment as the practice has changed.

Claims-made basis and your retroactive date

PI insurance for registered practitioners operates on a claims-made basis, meaning the claim must be made and reported during the active policy period, not necessarily when the underlying work was performed. This sounds straightforward until you factor in the retroactive date, which is the point from which your policy agrees to cover past work. If your retroactive date is set to today or to a recent date, you have no cover for work you completed in prior years, which is exactly when many claims arise.

Your retroactive date should align with the date you first provided registered services, and you should verify it on your policy schedule every time you renew.

Switching insurers without confirming that the new policy carries the same or earlier retroactive date can create a gap in historical coverage even though your policy looks current on paper. This is one of the most common unintentional gaps practitioners create for themselves.

Aggregate versus per-claim limits

Some policies quote a figure that looks like it satisfies the TPB minimum, but that figure is an aggregate limit covering all claims across the entire policy year, not a per-claim limit. The TPB’s minimum coverage amounts refer to cover per claim, not in total. A $500,000 aggregate policy that caps any single claim at $250,000 does not satisfy the per-claim minimum for a practitioner in the $75,001 to $1,000,000 fee income tier.

When you review your policy, confirm specifically whether the limit stated is applied per claim or in aggregate, and whether legal defence costs are included within that limit or sit outside it. Defence costs that erode your indemnity limit reduce what is actually available to settle a claim against you.

Notification obligations

Your policy will include a requirement to notify your insurer promptly when you become aware of a circumstance that could give rise to a claim, even if no formal claim has been lodged yet. Missing this notification window can result in your insurer declining cover for a claim that would otherwise have been paid under your tpb professional indemnity insurance policy.

Set a reminder to review open client matters before your renewal date each year and flag anything that carries residual risk or unresolved disputes. Treating notification as a routine annual task, rather than waiting until a formal complaint arrives, keeps you on the right side of both your insurer and the TPB.

How to choose compliant PI insurance in practice

Knowing what the TPB requires is one thing. Finding a policy that actually satisfies every requirement is where practitioners often spend unnecessary time or settle for coverage that misses the mark. Choosing the right tpb professional indemnity insurance policy comes down to asking the right questions before you sign, not after a claim is made.

Work with a broker who knows the professional services sector

Not every insurance broker understands the specific TPB requirements that apply to registered tax agents and BAS agents. A general business insurance broker may issue you a policy that looks adequate but uses definitions, exclusions, or aggregate limits that do not align with what the Regulations require. Seek out a broker or insurer with demonstrated experience placing PI cover for accounting and tax practices, ideally one who can confirm in writing that the policy meets the TPB’s conditions.

Ask your broker to confirm in writing that the policy satisfies the Tax Agent Services Regulations 2022 before you accept the quote.

Your broker should be able to walk you through the retroactive date, the per-claim limit structure, the definition of covered persons, and the run-off provisions without you needing to prompt them on each point. If they cannot, that is a signal to keep looking.

Check the policy wording, not just the certificate of currency

A certificate of currency tells you that a policy exists and provides a coverage amount. It does not tell you whether the policy wording satisfies every TPB condition. Before you renew or switch insurers, request the actual policy document and check the covered activities, the definition of insured persons, the retroactive date, and the notification obligations.

Confirm that the limit stated is a per-claim amount, that defence costs sit outside that limit rather than eroding it, and that the policy covers all services your practice provides under your registration. If you have added services, employed new practitioners, or changed your business structure since you last reviewed your policy, those changes need to be reflected in the current policy terms.

Match the coverage level to your current fee income

Your fee income changes year to year, and your minimum required coverage changes with it. Before you renew, calculate your total annual fee income from registered services for the past financial year and confirm which tier applies. Do not rely on the figure you used at your last renewal without checking it.

Insurers will not automatically increase your cover to match TPB thresholds unless you provide updated income figures. You carry the responsibility for ensuring the coverage level meets the regulatory minimum, so build a review step into your annual renewal process.

How to notify TPB and keep details current

Holding a compliant tpb professional indemnity insurance policy is not enough on its own. You also need to keep your insurance details current in the TPB’s register, because the Board uses the information you submit to assess whether your registration conditions are being met. Letting your recorded details fall out of date, even when your actual policy is still active and compliant, creates an administrative gap that can trigger compliance queries you do not need.

Updating your insurance details in the TPB portal

You manage your insurance details through the TPB’s Online Services portal, where your registration information is held. When your policy renews, changes insurer, or is updated with new coverage limits, you need to log in and update the relevant fields to reflect the current policy. The TPB does not receive policy updates directly from insurers, so the responsibility for keeping your registered insurance information accurate sits entirely with you.

The details you will typically need to update include your insurer’s name, your policy number, the coverage amount, and the policy expiry date. Make a point of updating these immediately after each renewal rather than leaving it until your next registration renewal period. Delays between your policy renewing and your TPB record being updated leave a window where your registered details do not match your actual coverage.

Update your TPB portal record on the same day your renewed policy documents arrive, not at the end of the quarter.

When you must notify the TPB

Certain changes to your insurance arrangements require prompt notification rather than waiting for your next scheduled registration renewal. If your policy is cancelled mid-term, if your insurer becomes insolvent, or if your coverage falls below the minimum required threshold for any reason, you need to notify the TPB as soon as possible. Operating with a coverage gap, even temporarily, is a breach of your registration conditions.

You should also notify the TPB when your practice structure changes in a way that affects who holds the policy. If you move from operating as a sole trader to a company structure, or if you add a new partner who needs to be covered, the policy details on record need to reflect those changes. Keep a short checklist that ties your insurance review directly to any structural changes in your business, so nothing slips through between your annual renewal cycle and an unexpected change in circumstances.

Ongoing compliance, renewals and record keeping

Maintaining compliant tpb professional indemnity insurance is not a once-a-year task that ends the moment you receive your renewal certificate. The TPB can review your registration conditions at any point, and your ability to demonstrate continuous, adequate coverage depends on how well you manage your records and renewal process throughout the year, not just during registration renewal periods.

Build a renewal checklist that covers every TPB requirement

Your renewal process needs to be systematic and repeatable, because the same details need to be verified each year regardless of whether your circumstances appear to have changed. A short checklist tied to your policy expiry date ensures nothing is missed and gives you a clear record of the steps you completed.

Run your renewal checklist at least four weeks before your policy expiry date so you have time to address any gaps before your cover lapses.

Work through these steps every renewal cycle:

- Confirm your total annual fee income from registered services and verify which coverage tier applies

- Check that your per-claim limit meets or exceeds the regulatory minimum for your tier

- Verify your retroactive date has not shifted, particularly if you have switched insurers

- Confirm that all current staff and contractors who provide registered services fall within the policy’s definition of covered persons

- Review run-off provisions and confirm they still meet TPB standards

- Update your TPB Online Services portal record with the new policy details immediately after renewal

- File your renewal documentation in your compliance records folder with the date of update noted

Keep your records ready for a TPB audit

The TPB can request evidence of your insurance coverage as part of a compliance review, and your records need to support a clear, uninterrupted coverage history. Keeping only the most recent certificate of currency is not sufficient. You should retain each year’s policy schedule, the full policy wording, and your renewal correspondence so you can demonstrate continuous coverage back to your registration date if required.

Store your records in a location that is accessible to your practice manager or a trusted colleague, not only to you personally. If you are unavailable during a compliance review, someone else needs to be able to locate and provide the relevant documents without delay. A shared, structured folder with clearly labelled files by policy year is straightforward to maintain and avoids the scramble of reconstructing a coverage history under pressure.

Treat your insurance records as part of your broader compliance file, alongside your registration certificate, CPE records, and any TPB correspondence. Keeping them together makes any future review faster and less disruptive to your practice.

Wrap-up and next steps

TPB professional indemnity insurance is a non-negotiable condition of your registration, and managing it well means more than holding a policy. You need the right coverage level for your fee income, a policy that covers all staff and services, a retroactive date that goes back far enough, and records that are kept current in the TPB portal. A gap in any one of those areas puts your registration at risk, regardless of how well you manage everything else.

Your compliance obligations do not stop at insurance. AUSTRAC Tranche 2 is extending AML/CTF requirements to accountants and tax practitioners, which means identity verification and client onboarding processes are now moving into the same compliance space as your PI obligations. If you want to understand how those requirements will affect your practice and how to handle them without adopting new software, explore how IdentityCheck handles Tranche 2 AML/CTF obligations.